CORSIA Carbon Credit Prices, Demand, and Supply: What the Future Holds

The Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), launched by the International Civil Aviation Organization (ICAO), plays a major role in helping airlines offset their emissions and meet climate goals.

International air travel is bouncing back after the pandemic. This drives a surge in demand for carbon credits under CORSIA. A new report by Allied Offsets forecasts strong growth in both demand and prices of eligible carbon credits from 2025 through 2035.

This article explores the latest trends, price scenarios, and what this means for airlines, project developers, and the broader voluntary carbon market.

Rising Demand: Airlines Set to Purchase More Credits

Industry estimates say that demand for CORSIA-eligible carbon credits will hit 101 to 148 million tonnes (MtCO₂e) during Phase I (2024–2026). Demand will rise quickly in Phase II (2027–2035).

Cumulative needs are expected to be between 502 and 1,299 MtCO₂e. This will depend on how much international air traffic grows and how CORSIA expands its coverage.

This big increase comes from the rebound in international air travel and the start of Phase II in 2027. During this phase, most ICAO member countries must take part.

By 2035, demand might exceed 1 billion tonnes in high-growth scenarios. That’s about the same as the yearly emissions of a major industrialized country.

To summarize projected cumulative demand:

-

Phase I (2024–2026): 101–148 MtCO₂e

-

Phase II (2027–2035): 502–1,299 MtCO₂e

This growth presents both challenges and opportunities. Airlines need enough credits to comply with regulations. At the same time, project developers and suppliers face pressure to increase the verified supply of eligible credits.

Price Outlook: A Wide Range with Upward Pressure

The report outlines three price scenarios for carbon credits based on different market dynamics:

-

Low Scenario: Prices start at $14/tonne in a tight supply scenario and grow slowly to $25/tonne in under supply scenario.

-

Medium Scenario: Prices rise from $15/tonne to $29/tonne.

-

High Scenario: Prices climb sharply from $16/tonne to $34/tonne.

Even in the conservative case, prices show modest growth. But in the high-demand scenario, prices could grow over the next decade.

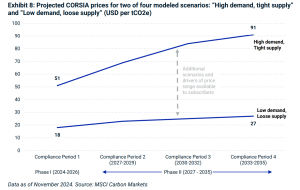

On the other hand, MSCI outlines a range of price scenarios for CORSIA-eligible carbon credits as follows:

-

Phase I (2024–2026): $18–$51 per tonne

-

Phase II (2027–2035): $27–$91 per tonne (by 2033–2035)

This price rise shows that airlines face more pressure to secure high-quality credits. This is especially true as more projects focus on long-term removal instead of just temporary avoidance.

High prices might lead some airlines to invest in sustainable aviation fuel (SAF) or insets. These options help reduce emissions in their operations.

Supply Gaps and Quality Filters

CORSIA doesn’t allow just any carbon credit. ICAO has strict rules for what qualifies — including restrictions on project start dates, crediting periods, and approved methodologies. Only credits from approved programs (like Verra, Gold Standard, and ART TREES) that meet these standards are eligible.

The report estimates that:

-

Only about 543 MtCO₂e of eligible credits will be issued by 2027.

Supply is projected to lag behind demand. Reports suggest possible deficits of 12–43 MtCO₂e in Phase I. Phase II may face even larger shortfalls. This is likely if stricter quality filters are used. These filters include co-benefits, permanence, and additionality. The exact numbers for filtered supply aren’t given, but these criteria would greatly lower the usable pool.

Currently, most eligible supply comes from avoided deforestation (REDD+) and renewable energy projects. As demand increases and quality standards get stricter, the market will likely move toward lasting carbon removal solutions. This includes methods like reforestation, biochar, and direct air capture (DAC).

Regional Insights: Where Supply Comes From

The current credit supply under CORSIA is heavily concentrated in a few countries:

-

India, China, and Brazil together account for over 50% of the available supply.

Africa has fewer CORSIA-eligible credits now. However, it is expected to grow. This growth will focus on nature-based solutions, such as afforestation and cookstove projects.

This geographic concentration means that any changes in policy, political stability, or project approvals in key countries could disrupt supply. For example, if India were to change its rules on carbon credit exports — as some officials have suggested — global supply could shrink quickly.

Interest is growing in boosting credit generation in Southeast Asia and Latin America. Many areas there have good land for reforestation and carbon farming.

Market Trends and Implications for Airlines

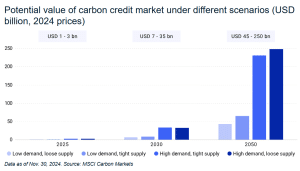

CORSIA credits are part of the larger voluntary carbon market. This market has attracted a lot of interest from companies and governments. According to MSCI report, voluntary carbon markets could reach $250 billion annually by 2050.

But today’s CORSIA credits are selling for far less than the cost of removing CO₂ using high-tech methods like DAC, which can exceed $300 per tonne. This price gap has raised questions about credit quality and how buyers can demonstrate real climate impact.

SEE MORE: CORSIA Credits Soaring Costs: How They Are Reshaping Aviation’s Future

Some key trends include:

-

Airlines such as Delta, United, and Lufthansa are now mixing credit purchases with investments in SAF. They also support offsets from reforestation or engineered removals.

-

Programs like SBTi (Science-Based Targets initiative) encourage firms to reduce emissions. They also promote high-quality removals instead of bulk offsetting.

For airlines, this means they may need to:

-

Budget more for compliance over time

-

Diversify carbon offset portfolios

-

Communicate clearly about the credibility of their offsets

The Bigger Picture: What Comes Next

The Allied Offsets report shows that corporate buyers, like airlines, play a key role in global carbon markets. Their large, long-term offtake agreements — such as Microsoft’s 18 MtCO₂e deal with Rubicon Carbon — are shaping demand signals for the next decade.

ICAO plans to tighten CORSIA rules in future reviews. This may mean more removals and limits on older avoidance projects. This could further reduce supply and raise prices.

Policymakers can boost support for in-sector measures. This includes increasing SAF production and encouraging new removal technologies.

Airlines face challenges now. They must deal with rising prices, new rules, and increased scrutiny on carbon offsetting. In the long run, using durable carbon removals could change aviation and the climate finance system.

CORSIA is entering a critical phase. Demand is set to rise sharply. Meanwhile, supply is tightening due to stricter quality controls. As the report shows, the window to build a balanced, credible carbon market is narrowing. The next few years will shape the cost and credibility of airline decarbonization for decades to come.

The post CORSIA Carbon Credit Prices, Demand, and Supply: What the Future Holds appeared first on Carbon Credits.