One Carbon Rulebook? GHG Protocol and ISO Join Forces to Rewrite Global Emissions Reporting

Companies around the world have spent years measuring their greenhouse gas emissions, but many still face the same problem. Different reporting standards can produce different results.

A company may calculate its emissions one way under the Greenhouse Gas (GHG) Protocol and another under ISO standards. That makes it harder for investors, regulators, and customers to compare companies fairly. This could soon change.

The GHG Protocol and the International Organization for Standardization (ISO) have announced plans to develop one interoperable global greenhouse gas accounting framework. The new effort will combine the strengths of both systems to create a more consistent way of measuring and reporting emissions worldwide.

The partnership is part of a broader update at the GHG Protocol. The organization is modernizing its corporate standards. It is also strengthening governance and adding a new independent process for setting standards. This change aims to meet the rising demand for reliable carbon accounting.

One Global Standard Could Cut Complexity

Carbon reporting has become much more complicated in recent years. The GHG Protocol is the world’s most widely used greenhouse gas accounting system.

According to the organization, 97% of Fortune Global 500 companies that report emissions use its standards. At the same time, ISO develops international standards that governments, businesses, and certification bodies use across many industries.

Both systems are widely trusted, but they were created separately.

As climate reporting has expanded, many companies now have to follow several reporting frameworks at once. A big multinational company can report under the GHG Protocol. It can also meet ISO standards, national rules, investor needs, and voluntary reporting programs.

That takes more time, increases costs, and often creates confusion. The new joint standard aims to simplify the process. Instead of following different accounting methods, companies could use one common approach to calculate and report emissions.

This consolidation merges ISO 14064-1 with GHG Protocol’s Scope 1, 2, 3, and Actions and Market Instruments (AMI) standards. By unifying these frameworks, businesses can track emissions more efficiently. Additionally, a single, coordinated public consultation process ensures more meaningful feedback from stakeholders.

Tim Mohin, CEO of GHG Protocol, noted:

“A consolidated corporate standard represents a significant step toward integrating and harmonizing greenhouse gas accounting across the world. For the organizations applying these standards to measure their greenhouse gas emissions, a single corporate standard will simplify reporting, reduce duplication, and provide greater consistency across markets and jurisdictions. This will in turn allow companies to spend more time reducing emissions.”

Carbon Reporting Is Becoming a Business Requirement

This change comes as carbon reporting becomes a normal part of doing business. More companies are setting net-zero targets, measuring emissions, and reporting climate risks than ever before. They need data that is accurate, consistent, and easy to compare.

The pressure to report emissions continues to grow.

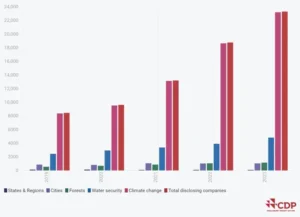

According to CDP, a record 24,800 companies disclosed environmental data through its platform in 2024. Businesses are getting ready for new disclosure rules in key markets. This includes the EU’s Corporate Sustainability Reporting Directive (CSRD) and California’s climate laws. These laws require many large companies to report on their greenhouse gas emissions, including parts of their value chains.

Global reporting standards are also becoming more aligned.

The International Sustainability Standards Board (ISSB) launched the IFRS S2 Climate-related Disclosures standard. This standard is based on greenhouse gas accounting for climate reporting. Many jurisdictions are now adopting or considering ISSB standards, increasing the need for consistent emissions data worldwide.

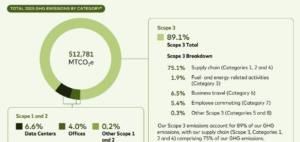

The biggest challenge, however, remains Scope 3 emissions.

These emissions come from suppliers, customers, transportation, purchased goods, and product use rather than a company’s own operations. For many businesses, Scope 3 represents the largest share of their climate footprint.

- In some industries, it accounts for more than 90% of total emissions, according to the GHG Protocol.

Measuring those emissions accurately has proven difficult because companies depend on data from hundreds or even thousands of suppliers.

That is one reason why the GHG Protocol and ISO believe a common, unified global framework has become increasingly important. Improving consistency can boost reporting quality. It can also cut confusion and make emissions data more useful for investors, regulators, and businesses.

Better Carbon Data Could Strengthen Carbon Markets

A single global accounting standard could also strengthen carbon markets.

Carbon credits depend on accurate emissions data. When companies calculate emissions in different ways, it gets harder to measure reductions. This makes it tough to set climate targets and figure out how many carbon credits are needed.

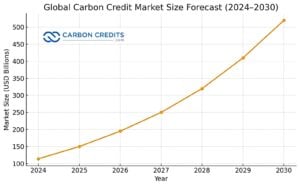

That is becoming more important as carbon markets continue to grow. Compliance carbon markets could hit up to $500 billion by 2030, while voluntary markets could reach $40 billion by the same period.

Meanwhile, Article 6 of the Paris Agreement is creating new international carbon markets. More countries are developing rules to trade carbon credits across borders. Accurate emissions accounting is key. It helps measure credits consistently and prevents double counting.

A common global reporting standard could help provide that foundation. Over time, the standard could improve consistency across carbon credit projects and support higher-quality carbon markets.

A New Foundation for Net Zero Reporting

The new standards will take time to develop. The GHG Protocol and ISO said they will follow an open standards development process with public consultations and technical reviews. Businesses, governments, investors, scientists, and other stakeholders will all have opportunities to provide feedback before the standards are finalized.

If completed, these changes would mark one of the biggest updates to corporate carbon accounting in more than 20 years. The goal is simple: make emissions reporting easier, more consistent, and more useful around the world.

That would reduce reporting costs, improve the quality of emissions data, and make climate disclosures easier to compare across companies and countries.

It could also strengthen other climate initiatives. Organizations such as the Science Based Targets initiative (SBTi), the Integrity Council for the Voluntary Carbon Market (ICVCM), and the Voluntary Carbon Markets Integrity Initiative (VCMI) all rely on credible emissions data to support corporate net-zero claims and high-integrity carbon markets.

For businesses, the benefits are clear: less time dealing with different reporting rules and more time reducing emissions. For investors, it means more reliable climate data.

And for carbon markets, it could provide a stronger foundation for measuring emissions, tracking progress, and building trust as the world moves toward a low-carbon economy.

The post One Carbon Rulebook? GHG Protocol and ISO Join Forces to Rewrite Global Emissions Reporting appeared first on Carbon Credits.