Mark Carney Admits Canada Will Miss 2030 and 2035 Climate Targets as Policy Rollbacks Slow Progress

Canada’s climate strategy reached a turning point this week. Prime Minister Mark Carney openly acknowledged that the country will not meet its greenhouse gas emissions targets for 2030 and 2035 under current policies. The admission marked a rare moment of candor from a government that has already rolled back several flagship climate measures since taking office in March.

Speaking to Radio-Canada, Carney said it was “clear” Canada would fall short of its goals unless policies change. The statement landed heavily because Canada’s climate targets are not aspirational. They are written into law and closely watched by investors, provinces, and international partners.

At the same time, the government continues to defend its long-term strategy. Officials argue that energy investments, industrial decarbonization, and revised methane rules will eventually bend the emissions curve downward. However, recent data, audits, and projections suggest the gap between ambition and reality remains wide.

Canada’s 1% Emission Cuts Fall Short of Net-Zero Goals

Canada committed in 2021 to cut emissions 40% to 45% below 2005 levels by 2030. It also pledged to reach a net-zero electricity grid by 2035. Later, the country strengthened its longer-term ambition, submitting a nationally determined contribution (NDC) in February 2025 that raised the 2035 reduction goal to 45%–50%.

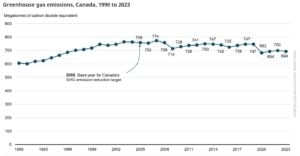

Yet progress has been slow. Between 2005 and 2023, Canada reduced emissions by only about 8.5%. That translates to about a 1% annual reduction. While progress is real, it falls far short of what climate science demands.

- A global net-zero-by-2050 pathway requires annual emissions cuts closer to 4%. At the current pace, Canada simply cannot close the gap by 2030 or 2035.

High Emissions, Heavy Footprint

Globally, Canada ranked 11th worldwide in total emissions in 2022, contributing about 1.4% of the global total.

- According to Climate Change Tracker data, Canada’s emissions stand at roughly 816 megatonnes of CO₂-equivalent in 2024.

- Based on the 2025 Progress Report on the 2030 Emissions Reduction Plan, Canada’s emissions were 694 Mt in 2023.

Yet per capita emissions tell a different story. Canadians emit between 14 and 20.5 tonnes of CO₂-equivalent per person each year, depending on the metric used. That places Canada among the highest per capita emitters in the OECD.

This imbalance matters. While Canada’s global share may seem modest, its emissions intensity remains extremely high. When combined with other mid-sized emitters, Canada’s footprint contributes meaningfully to global warming.

Additionally, under the policies currently in place, emissions are expected to fall only about 21% below 2005 levels by 2030. In short, Canada is moving in the right direction, but far too slowly.

Policy Reversals Shake Climate Confidence

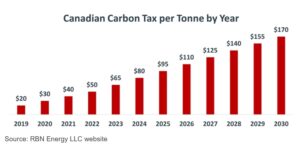

Since taking office, Carney’s minority government has shifted course on several climate policies. Most notably, it eliminated the consumer-facing carbon tax on fuels in April 2025. Canadians no longer pay a carbon charge at the pump or on home heating fuels.

The government also scrapped a proposed emissions cap for the oil and gas sector. These moves were framed as part of a broader effort to turn Canada into an “energy superpower,” especially as trade tensions with the United States intensified under President Donald Trump.

However, the policy pivot triggered political fallout. Steven Guilbeault, who served as environment minister under former Prime Minister Justin Trudeau, resigned after Ottawa reached a deal with Alberta that relaxed certain climate rules to support pipeline development. In his resignation statement, Guilbeault warned that environmental priorities were being sidelined.

Meanwhile, current Environment Minister Julie Dabrusin struck a more optimistic tone. She said Canada’s 2030 and 2035 targets remain achievable, directly contradicting Carney’s public assessment. The mixed messaging has added uncertainty to Canada’s climate outlook.

Fresh Methane Rules: Strong Signal, Longer Timeline

One area where the government doubled down is methane regulation. Recently, Ottawa announced new rules aimed at cutting oil and gas methane emissions by 75% by 2035. Carney’s government extended the deadline by five years, offering companies more time to comply. It also fulfills a promise Carney made during the election campaign to strengthen existing methane standards.

The press release from the Government of Canada projects that from 2028, when the new regulations take effect, through 2040, the measures will cut a total of 304 million tonnes of CO₂-equivalent and 1,593 kilotonnes of volatile organic compounds (VOCs).

- These reductions are expected to prevent around $36.3 billion in climate-related damages and deliver $257 million in health benefits to Canadians.

Methane may not stay in the atmosphere as long as carbon dioxide, but it packs a powerful punch. Over 20 years, methane can trap roughly 80 times more heat than CO₂. Oil and gas facilities account for about half of Canada’s methane emissions, largely due to venting, flaring, and leaks across production infrastructure.

Thus, stronger methane controls could deliver fast climate benefits.

Canada’s Carbon Pricing at Crossroads?

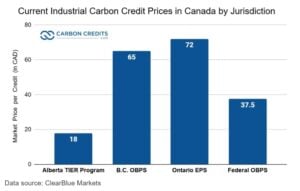

Carbon pricing remains a central pillar of Canada’s climate framework, even after recent changes. For large industrial emitters, the Output-Based Pricing System (OBPS) remains operational. Under this system, facilities receive emissions limits based on output. Companies that exceed their limits must pay, while those that perform better earn tradable credits.

The OBPS aims to cut emissions without driving industries offshore. It tries to balance climate ambition with global competitiveness.

However, the removal of the consumer carbon tax shifted the burden almost entirely onto industry. The federal government plans to review the carbon pricing benchmark in 2026. That review could reshape how the OBPS functions and how stringent it becomes.

This moment is critical. Without clear rules and long-term certainty, carbon pricing risks becoming too weak to drive meaningful change. On the other hand, a strong and predictable system could help Canada decarbonize while protecting jobs and investment.

- CHECK DETAILS HERE: Canada’s Carbon Pricing Reset in 2026: Will Industry Step Up or Stall Climate Progress?

Is the Window Narrowing for Action?

Carney’s admission removes any illusion that Canada is on track. The challenge now is whether the government uses this moment to reset policy or continues to rely on long-term promises.

New methane rules, industrial carbon pricing, and clean energy investments offer pathways forward. Yet auditors, analysts, and climate institutes agree that current measures lack the scale and speed required.

Canada stands at an economic and environmental crossroads. Stronger climate policy could position the country as a credible player in the global energy transition. Weak or uncertain action, by contrast, risks higher emissions, lost competitiveness, and missed opportunities.

The targets are still on the books. The question is whether Canada is willing to match them with the policies needed to make them real.

- ALSO READ: From Now to 2060: How Canada’s SMRs and Maritime Nuclear Power Will Drive a Net-Zero Future

The post Mark Carney Admits Canada Will Miss 2030 and 2035 Climate Targets as Policy Rollbacks Slow Progress appeared first on Carbon Credits.