CORSIA Credits Soaring Costs: How They Are Reshaping Aviation’s Future

A report analyzing carbon credit demand for over 400 airlines under the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) projects significant fluctuations in credit prices and airline costs.

According to modeling by MSCI Carbon Markets, CORSIA-eligible carbon credits could cost between $18-51 per tonne of carbon dioxide equivalent (CO2e) during Phase I, rising to $27-91 in Phase II. If airlines pass these costs on to consumers, international ticket prices could increase by 0.5-1.0% in Phase I.

Alternatively, if airlines absorb the costs, their operating profits could decrease by up to 4%. The impact will vary depending on different demand and supply scenarios.

We crunch the report and here are our key takeaways.

What Are CORSIA Credits? A Flight Plan for Emission Reductions

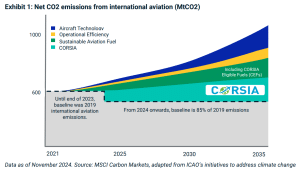

The aviation sector is one of the fastest-growing contributors to global greenhouse gas (GHG) emissions. As international air travel expands, airlines face increasing pressure to mitigate their environmental impact.

The CORSIA, developed by the International Civil Aviation Organization (ICAO), is designed to limit emissions growth in international aviation. By purchasing carbon offsets known as CORSIA credits, airlines can balance emissions exceeding 2020 levels and invest in sustainability.

CORSIA credits allow airlines to compensate for their emissions by funding projects that reduce or remove CO2. These projects include renewable energy initiatives, reforestation, and carbon capture technologies. Verified under internationally recognized standards such as the Verified Carbon Standard (VCS) and the Gold Standard, these credits ensure that emission reductions are real, additional, and permanent.

CORSIA aims to cap international aviation emissions at 2020 levels. Through its two implementation phases—voluntary (2021–2023) and mandatory (from 2024)—the program encourages investment in global sustainability while aligning the aviation industry with broader climate goals.

Carbon Credit Demand: Will Airlines Keep Up with Rising Costs?

CORSIA’s demand for carbon credits hinges on international aviation growth and decarbonization efforts. Using a bottom-up modeling approach, MSCI Carbon Markets analysts assess individual airline emissions, growth rates, and adoption of sustainable practices to project credit needs.

Demand Scenarios

Three scenarios highlight the variability in credit demand:

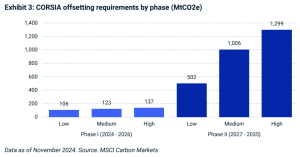

- High-Demand Scenario: Strong aviation growth (+4% annually) and slow adoption of sustainable aviation fuels (SAFs) result in higher offsetting needs. Estimated demand reaches 137 million metric tons of CO2 equivalent (MtCO2e) in Phase I (2024–2026) and 1,299 MtCO2e in Phase II (2027–2035).

- Medium-Demand Scenario: Moderate aviation growth and increased decarbonization lower credit demand to 123 MtCO2e in Phase I and 1,006 MtCO2e in Phase II.

- Low-Demand Scenario: Limited growth and poor adoption of SAFs reduce requirements to 106 MtCO2e in Phase I and 502 MtCO2e in Phase II.

Regional and Airline-Level Insights

Demand will be concentrated among major airlines and regions. For instance, the top 10 airlines are expected to account for 40% of cumulative demand by 2035.

European carriers are likely to lead credit purchases despite regional compliance mechanisms such as the EU Emissions Trading System (ETS). If the ETS is expanded to cover more flights, global demand for CORSIA credits could decrease by 25–50% by 2050.

Supply Struggles: Why CORSIA Credit Availability Could Impact Aviation

The supply of CORSIA-eligible credits faces significant challenges. Credits must meet ICAO criteria, including corresponding adjustments that prevent double counting of emissions reductions under a country’s Nationally Determined Contributions (NDCs). This process requires host countries to authorize projects and align carbon accounting frameworks—a complex and underdeveloped requirement.

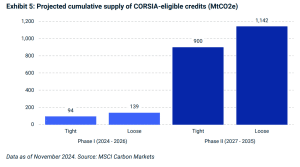

As of late 2024, ICAO-approved registries like Verra, Gold Standard, and Climate Action Reserve have expanded the potential credit pool to 230 MtCO2e. However, only 7 MtCO2e of these credits meet Phase I criteria due to limited corresponding adjustments.

Most eligible credits have been issued by a single REDD+ project in Guyana under ART TREES.

A lack of Letters of Authorization (LoAs) from host countries further constrains supply. Of 40 major credit-producing countries assessed, only two are highly prepared to issue LoAs. Without accelerated regulatory progress, substantial credit supply growth is unlikely until the late 2020s.

Projections and Flexibility

Supply projections factor in registry eligibility, crediting timelines, and the readiness of host countries to provide corresponding adjustments. A 30% reduction is applied to projects not yet in the registry pipeline. Despite these hurdles, expanded registry approvals and government action could gradually increase the availability of CORSIA-compliant credits.

Scenarios for Carbon Prices: How High Will CORSIA Credits Soar?

The prices of CORSIA credits will depend on supply-demand dynamics, influenced by credit availability, international aviation growth, and compliance requirements.

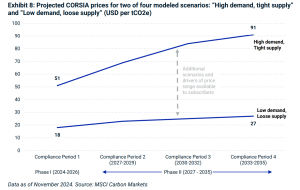

Under high-demand and tight-supply scenarios, Phase I credit prices are expected to range between $18 and $51 per ton of CO2. Prices could climb to $27–$91 per ton during the fourth compliance period (2033–2035) as demand peaks.

Supply-Demand Scenarios

- Tight Supply: A potential deficit of 12–43 million tons of CO2 in Phase I could drive prices higher.

- Loose Supply: A surplus of 2–33 million tons of CO2 may stabilize prices during Phase I. Airlines also have a grace period until January 2028 to offset emissions, easing initial supply constraints.

In Phase II, higher demand from aviation and other sectors, such as corporate voluntary commitments and sovereign programs, could lead to significant price increases.

Market Value Estimates

The market for CORSIA-eligible credits could reach $2–$8 billion by Phase I and grow to $5–$66 billion by the fourth compliance period. This growth reflects both rising demand and the financial implications of carbon market integration.

Implications for Airlines and Carbon Markets

CORSIA credits are an essential tool for airlines to manage emissions and comply with climate regulations. However, reliance on credits is only a short-term solution.

Long-term strategies include investment in SAFs or Sustainable Aviation Fuel, fleet upgrades, and operational efficiencies. Airlines with slower decarbonization may face higher offsetting costs, incentivizing innovation and sustainable practices.

Geopolitical factors and regulatory developments will heavily influence the carbon market. Expanding participation and ensuring the environmental integrity of credits are critical to maintaining trust and achieving emissions reductions.

CORSIA credits are pivotal to the aviation industry’s efforts to cap emissions and contribute to global climate goals. Although challenges remain in scaling credit supply and ensuring regulatory compliance, CORSIA serves as a transitional mechanism while the sector invests in greener technologies. As demand for high-quality offsets grows, the aviation industry’s collaboration with carbon markets will shape the roadmap of global emissions reductions.

The post CORSIA Credits Soaring Costs: How They Are Reshaping Aviation’s Future appeared first on Carbon Credits.