Nickel Prices Fall to a 4-Year Low: What Causes The Plunge?

Demand for battery-grade nickel is projected to grow significantly by the end of the decade due to rising electric vehicle (EV) adoption. However, the nickel market faced more volatility and uncertainty in November 2024, according to S&P Commodity Insights data. It is largely due to macroeconomic and political developments following Donald Trump’s U.S. presidential election victory.

Trump’s Victory Fuels Nickel Market Volatility

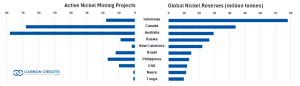

Nickel is vital for producing stainless steel and alloys used in equipment, transport, buildings, and power generation. Major nickel producers include Indonesia, the Philippines, Russia, and Australia, with Indonesia having the highest nickel reserves while Australia has the most active mining projects.

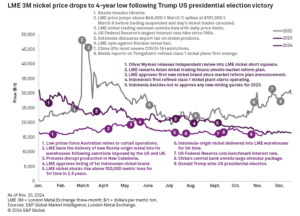

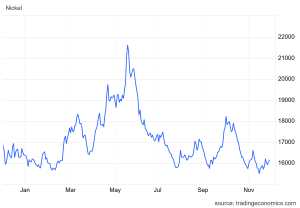

Nickel futures are traded on the London Metal Exchange (LME), reflecting its global industrial importance. The LME three-month nickel price dropped to a four-year low of $15,540 per metric ton on November 15.

Concerns over Trump’s potential economic policies, particularly their implications for China, the industrial metals’ top consumer, have fueled investor caution. A stronger U.S. dollar and increased LME nickel inventories further worsen the downward pressure on prices as shown above. This highlights a risk-off sentiment across metals markets.

-

Nickel prices initially saw an uptick after Trump’s election win, rising from $16,007 per metric ton on November 4 to $16,587 per metric ton on November 7.

This temporary boost mirrored gains in U.S. equity markets. However, optimism quickly faded as the trade-weighted U.S. dollar index climbed to a one-year high, fueled by market expectations that Trump’s policies—such as higher tariffs on Chinese imports—could revive U.S. inflation.

The prospect of prolonged high interest rates from the Federal Reserve further strengthened the dollar. This makes nickel and other commodities more expensive for non-dollar investors.

Investor sentiment in the nickel market took another hit following China’s unveiling of a 10 trillion yuan fiscal stimulus package on November 8. The measures failed to meet market expectations for more aggressive economic support. This disappointment, coupled with rising nickel inventories and a nearly 4x increase in net short positions on LME nickel, accelerated the price decline.

By mid-November, the LME three-month nickel price had plunged to levels not seen since November 2020, underscoring the market’s vulnerability to both economic and geopolitical developments.

In late November, nickel rebounded to $16,040 per tonne amid Indonesia’s tighter mining policies. Approved quotas could drop 27% by 2026, while license fees for low-grade ore may be reduced.

According to the Indonesian mining minister, nickel ore imports surged 50-fold, as officials prioritized domestic reserves and warned of dwindling stocks to stabilize prices.

IRA Under Threat: What Trump’s Plans Mean for Nickel and EVs

The implications of Trump’s election for the U.S. Inflation Reduction Act (IRA) add another layer of uncertainty to the global nickel market.

Signed into law by President Joe Biden in 2022, the IRA has been a key driver of clean energy initiatives. This includes a $7,500 consumer tax credit for electric vehicles.

However, Trump’s transition team is reportedly considering repealing this tax credit as part of broader tax reform efforts. Such a move could slow the adoption of EVs in the U.S. This could undermine a major driver of global primary nickel demand over the next five years.

Additionally, Trump’s administration may tighten the IRA’s foreign entity of concern (FEOC) guidelines, which currently disqualify companies with significant Chinese ownership from benefiting from the EV tax credit. For instance, Indonesia—a leading producer of nickel—has been working to reduce China’s influence to qualify for IRA incentives.

In a recent deal between PT Vale Indonesia and China’s GEM Co., GEM’s stake in a $1.42 billion nickel plant was capped at 25% to comply with the guidelines. However, stricter FEOC rules could make it even harder for such projects to qualify for U.S. tax incentives. This can potentially limit Indonesia’s ability to expand its nickel exports to the U.S.

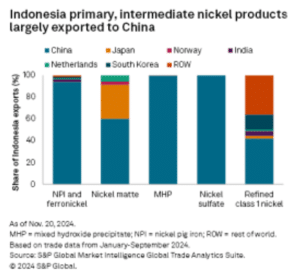

China remains a dominant player in Indonesia’s nickel sector. Between January and September 2024, Indonesia exported 129,860 metric tons of nickel sulfate exclusively to China.

If Indonesia faces challenges in accessing U.S. markets due to stricter IRA policies, its reliance on China is likely to deepen. This dynamic could reshape global nickel supply chains, with potential long-term implications for battery manufacturing and EV production.

Short-Term Pain, Long-Term Gain? Nickel’s Future Outlook

Beyond U.S. policy developments, other global factors are contributing to nickel market uncertainty. Escalations in the Russia-Ukraine war have dampened investor confidence, while concerns about slowing economic growth in China continue to weigh on demand projections.

The interplay of these factors has led to reduced risk appetite among investors, as evidenced by the sharp rise in short positions on LME nickel.

Despite these challenges, S&P Global’s fundamental outlook for primary nickel supply and demand remains broadly unchanged from previous forecasts. However, the near-term trading environment is expected to remain difficult.

Amid all these challenging market conditions, an emerging player is targeting U.S. nickel independence. Alaska Energy Metals Corporation (AEMC) is leading efforts to support the U.S. energy transition through its flagship Nikolai project in Alaska. The site holds a significant resource of nickel, copper, cobalt, and platinum group metals essential for renewable energy and electric vehicles.

The Canadian nickel junior’s dual focus on sustainability and critical mineral supply underscores its commitment to reducing U.S. reliance on imports.

With the nickel prices already at a multi-year low, the market’s recovery will depend on clearer policy signals and stronger demand drivers, particularly from the EV and clean energy sectors.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: AEMC.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Please read our Full RISKS and DISCLOSURE here.

The post Nickel Prices Fall to a 4-Year Low: What Causes The Plunge? appeared first on Carbon Credits.