Canada’s $16.5 Billion Bet on Carbon Capture: Could It Cut Oil Sands Emissions?

A group of Canada’s largest oil sands companies, the Pathways Alliance, is in active discussions with Canada Growth Fund (CGF), the federal government’s $15-billion green investment arm, to secure backing for a substantial carbon capture and storage (CCS) project in northern Alberta.

CCS technology is seen as one of the most effective solutions to reduce emissions in high-polluting sectors like oil, gas, and cement. Canada views this carbon management approach as essential for achieving its net-zero emissions goals.

Carbon Capture Enters the Big Leagues But Price Uncertainty Raises Concerns

The country currently operates several CCS projects that have stored around 44 million tonnes of CO₂ since 2000.

The federal plan calls for tripling national CCS capacity by 2030 to meet its carbon emission reduction targets. This ambitious goal would require adding new facilities capable of capturing 15 million tonnes of CO₂ annually.

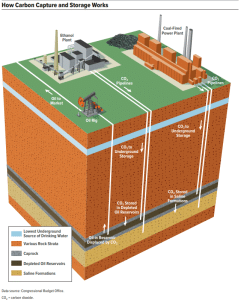

The Pathways Alliance project would include a $16.5-billion network for capturing and storing CO₂ emissions from over a dozen oil sands facilities. The captured CO₂ will be transported to a central hub in Cold Lake, Alberta. Once operational, this network would permanently store the captured CO₂ deep underground, supporting efforts to reduce emissions across Alberta’s oil sands industry.

This is a major step in decarbonization efforts for Canada’s oil and gas sector. However, oil sands executives remain wary of the potential financial risks tied to the future price of carbon.

Adam Waterous, executive chairman of Strathcona Resources, emphasized the “stroke-of-the-pen” risk, a term used to describe the industry’s fear that regulatory changes or policy reversals, such as a shift in the carbon tax, could drastically impact the value of carbon credits.

Waterous, whose company is the first in the sector to strike a CCS deal with CGF, suggested that industry leaders are cautious about committing capital to projects that could ultimately result in stranded assets if carbon prices don’t stabilize.

Moreover, Waterous foresees a significant need for sequestered carbon from technology firms looking to offset emissions. In particular, a recent carbon capture deal between Microsoft and Occidental Petroleum, aimed at reducing data center emissions.

The Role of Carbon Contracts for Difference (CCfD)

To address industry apprehensions, experts recommend using Carbon Contracts for Difference (CCfD). It offers a guaranteed floor price for sequestered carbon. CCfDs help “de-risk” investments in emissions reduction technology by providing more stable pricing.

They argue it could be a decisive factor in encouraging the Pathways Alliance and other companies to pursue costly CCS projects.

Canada Growth Fund was partially designed to deploy tools like CCfDs to jumpstart green investments. However, it has not yet offered these to oil and gas producers, who are also seeking loan support for carbon capture technology.

The only oil and gas-related agreement involving CCfDs that CGF has reached thus far is with Entropy, a clean-tech company owned by Advantage Energy. The deal allows Entropy to sell carbon credits with an initial value of up to 185,000 tonnes at $86.50 per tonne.

In contrast, oil producers seeking to meet compliance obligations through carbon credits have been unable to secure similar agreements with CGF, leaving a gap in support for some of the industry’s largest players.

World’s Largest CCS Project by Pathways Alliance

The Pathways Alliance comprises six major oil sands companies:

- Canadian Natural Resources,

- Suncor Energy,

- Cenovus Energy,

- Imperial Oil,

- MEG Energy, and

- ConocoPhillips Canada.

If successful, their carbon capture and storage network would be the world’s largest and a landmark in global CCS projects. The alliance is eager to collaborate with Ottawa, recognizing the role government backing plays in ensuring the viability of large-scale CCS ventures.

Kendall Dilling, president of the Pathways Alliance, expressed optimism over Ottawa’s commitment to de-risking industry investments, stating that they “look forward to continued engagement with the government.”

Other policy experts echoed the sentiment that any successful deal would depend on assurance that the operating costs for carbon capture and storage infrastructure will be viable in the long term. This happens if carbon pricing remains stable.

Carbon Pricing: A Make-or-Break Factor

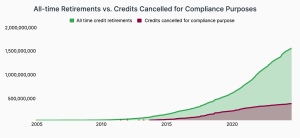

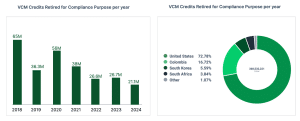

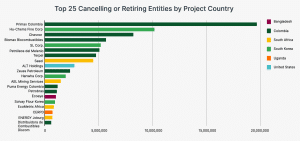

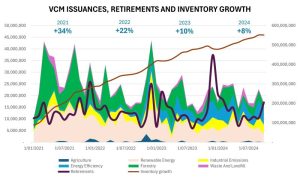

The fate of the Pathways Alliance’s CCS project will hinge on the development of carbon pricing policies and market demand. The recent surge in carbon credit retirements, representing demand, highlights a potential future trend that could significantly impact carbon prices.

Remarkably, Rich Gilmore, CEO of Carbon Growth Partners, stated that although retirements have fluctuated in the past, 2024 looks set to hit a record high. He shared on LinkedIn some of his interesting insights regarding voluntary carbon market (VCM) growth.

As seen in the chart below, demand surged from November 2023 to January 2024, causing a sharp drop in inventory. This spike was largely due to Shell retiring around 17 million credits to hit its internal net emissions efficiency target. That’s one company offsetting about 28% of its Scope 1 and 2 emissions—without even touching Scope 3.

This shift, spurred by one major player, demonstrates the scale of impact that corporations can have on the VCM.

Now, imagine the impact when more companies commit to scaling their carbon reduction strategies taking Shell as an example. The demand could quickly outpace supply, driving up carbon credit prices and creating a more competitive market for offsets.

Shell’s industry has a strong reliance on carbon capture technology to help meet decarbonization targets. Canada, as part of its Emissions Reduction Plan, focuses on achieving substantial emission cuts in the oil and gas sector.

As the country navigates its decarbonization goals, the Pathways Alliance’s CCS negotiations with CGF show the complexities of advancing green initiatives within a competitive, carbon-intensive sector.

With potential government support on the horizon, Canada’s oil sands companies could help make significant progress toward lowering emissions. Once it happens, it will set a precedent for industry-government collaboration on climate action in the years to come.

The post Canada’s $16.5 Billion Bet on Carbon Capture: Could It Cut Oil Sands Emissions? appeared first on Carbon Credits.