What’s Shaping North America’s Natural Gas in 2024? Insights from Wood Mackenzie

The natural gas market has immensely benefitted this year from robust storage levels and stabilized prices after the sharp spikes of 2022. However, challenges such as volatile pricing, seasonal demand fluctuations, and supply-demand imbalances persist. The emergence of renewable natural gas (RNG) and LNG export projects reflects ongoing structural shifts in this dynamic energy landscape of North America.

Industry experts predict that the North American natural gas market is projected to grow at a 5% CAGR between 2022 and 2027. This will be driven primarily by increasing industrial demand from the refining, petrochemical, and fertilizer sectors.

Winter 2024: What Will Drive North America’s Natural Gas Markets?

Apart from production levels and storage capacity, the North American natural gas market is also shaped by power market trends, LNG exports, imports, and changing weather patterns. But which of these will play the most critical role in the upcoming season? Let’s study the Wood Mackenzie findings…

Cold Snaps Impact Demand and Supply

Changing weather conditions significantly impact the natural gas market. And this is the direct effect of climate change. Cold snaps not only just spike demand, they also disrupt supply. Freeze-offs, where water or liquids in gas wells solidify and block production, are a recurring issue in North America.

Wood Mac reports that historically, these events have reduced about 0.7% of Lower 48 output during winter. However, losses vary and depend on the location and intensity of the cold. These disruptions are most critical because they hit supply when demand peaks.

LNG Exports Fluctuate Gas Price

LNG exports are driving growth in the U.S. gas market, with new projects like Venture Global’s Plaquemines in Louisiana and Cheniere Energy’s Corpus Christi expansion boosting capacity. However, this surge constricts domestic gas supplies, especially when demand is at its highest level.

For instance, natural gas inflows for LNG exports dropped from 15 billion cubic feet per day (bcfd) to 7 bcfd to meet local needs due to severe cold this January. This shortage drove Henry Hub prices to $13, with some regions experiencing even higher spikes. This showed that LNG exports are increasingly acting as “synthetic storage,” thereby balancing supply when stored gas falls short.

Production Choices May Strain the Supply

North American natural gas producers are increasingly managing supply through proactive decisions. Companies like EQT and Expand Energy (formerly Chesapeake Energy) have found strategic ways to adjust the supply based on market price.

Some techniques like delaying the activation of new wells or turning existing wells on and off can transform gas production into “synthetic storage“. However, this widely adopted approach is expected to still keep markets unpredictable this winter.

Renewables Fuel Demand Volatility

Natural gas demand for electricity generation has also become more unpredictable. Several factors influence this surge, including the retirement of coal plants, low gas prices fueling coal-to-gas switching, and an overall increase in power load.

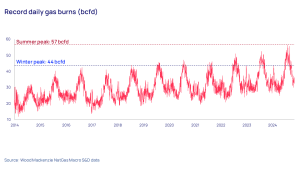

Power generation during summer hit a record high of 58 bcfd of gas, surpassing 50% of the total U.S. production of just over 100 bcfd. Last winter, demand also peaked at a record 44 bcfd, reflecting a year-round trend.

However, renewable energy plays a key role in the power sector. Simply put, during summer solar availability is high, while wind power is low and it’s just the opposite during winter. These fluctuations increase reliance on natural gas during extreme weather.

Storage Shortfalls and Supply Concerns

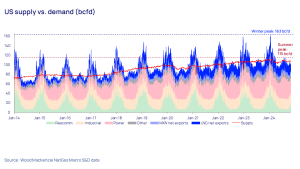

Storage capacity acts as a buffer during high demand or low supply. The report revealed that in recent years, storage capacity was limited. This was mainly due to narrow summer-winter price spreads which offered very minimal commissioning to set up new storage facilities. The planned 50 billion cubic feet of capacity falls short of market needs.

The demand for stored gas remains substantially high during peak winters like in January 2024 which led to 64 bcfd withdrawals. Conversely, the “days of cover” metric, measuring storage relative to demand, remains low in the cold. Thus, raising supply concerns.

Price Volatility

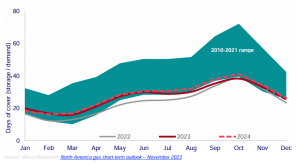

We can comprehend now that North America’s natural gas market faces significant instability due to storage-related struggles. However, this year storage inventories showed a 10% surplus compared to the five-year average which caused a sharp price drop in Henry Hub gas prices.

Despite this surplus, long-term storage capacity lags behind market expansion. Currently, U.S. storage covers only 25 days of full demand—a historic low. Without significant expansion, volatile prices could dominate the years ahead.

US L48 storage represented as days of demand cover

North America’s Natural Gas Market: Opportunities Amid Challenges

We have studied the challenges that North America’s gas market faces but at the same time, it has transformed significantly tapping the opportunities that lie ahead. Quite evidently, natural gas will play a vital role while replacing coal and renewables, bolstering the energy mix.

Several ongoing and upcoming projects will expand capacity and address the challenges related to price, demand, and supply of natural gas.

Renewable Natural Gas Gains Momentum

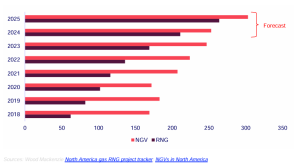

Renewable Natural Gas (RNG) has emerged as a promising tool for decarbonization. Supported by policies like California’s Renewable Gas Standard, RNG production is growing, with 324 projects in operation across the U.S. and Canada.

In 2024, demand-side contracting is expected to gain traction, particularly in hard-to-decarbonize sectors and heavy-duty transportation. Companies like Walmart and UPS are already testing RNG-powered fleets which signals a transition toward sustainable fuel solutions.

North American gas RNG production and NGV demand

LNG Export Boom: North America’s Next Wave

With rising U.S. and Canadian gas production and storage levels hitting highs in 2023, the North American gas market eagerly waits for the upcoming LNG export projects. While the timelines for large-scale terminals like Plaquemines and Golden Pass are well-known, the impact of this new demand surge remains uncertain.

Low gas prices have recently discouraged production growth. However, forward price projections showing premiums of up to $4/mmbtu for late 2024 and 2025 signal more lucrative returns when this demand kicks in.

Some promising LNG projects in North America include Plaquemines LNG Phase 1 in Louisiana, Golden Pass LNG, The Corpus Christi, Fast Altamira FLNG project in Mexico, LNG Canada, etc.

These developments highlight the growing structural demand for LNG across North America and beyond. While challenges persist, the region’s LNG export potential is poised to reshape global energy markets.

All in all, natural gas continues to be pivotal for North America’s energy system. However, it’s crucial to tackle challenges like weather, limited storage, redundant infrastructure, and the need to integrate renewables smoothly. So, overcoming these hurdles will be key to ensuring the sector’s growth and stability in the future.

Sources:

- Woodmac: North America Gas: 5 things to look for in 2024

- 5 factors affecting North American natural gas markets this winter | Wood Mackenzie

- FURTHER READING: US Power Demand Surge Spurs 133 New Gas Plants Amid Climate Targets

The post What’s Shaping North America’s Natural Gas in 2024? Insights from Wood Mackenzie appeared first on Carbon Credits.

Source: EU

Source: EU Source:

Source: