Indonesia’s Bold Push to Net Zero: Shutting Down All Coal Plants in 15 Years

Indonesia has unveiled an ambitious plan to transition away from fossil fuels and achieve net-zero emissions by 2050, a decade earlier than its previous target. Speaking at the G20 Summit in Brazil, President Prabowo Subianto announced a timeline to retire all coal-fired and fossil-fueled power plants within 15 years.

From Coal to Clean: Indonesia’s 15-Year Plan for Energy Revolution

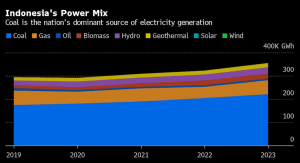

The Southeast Asian nation aims to replace its fossil fuel capacity with over 75 GW of renewable energy, utilizing its rich geothermal resources and expanding its solar and wind infrastructure. This commitment marks a significant shift for a country heavily reliant on coal and natural gas. These energy sources account for almost 80% of Indonesia’s electricity production.

Indonesia’s coal-fired power emissions surpassed 185 million metric tons of CO₂ equivalent (MtCO₂e) in 2023. This makes the country a significant contributor to global power sector emissions. With coal dominating its electricity mix, Indonesia remains heavily reliant on this fossil fuel for energy production.

As of the end of 2023, Indonesia’s combined wind and solar capacity was less than 1 GW, per BloombergNEF data above. This underscores the vast scale of transformation required to meet its targets.

Despite these challenges, the country is determined to pivot towards renewable energy and be a regional leader in the green energy transition.

Building on Global Partnerships

Indonesia’s ambitious agenda builds on the $20 billion Just Energy Transition Partnership (JETP) deal signed in 2022. This initiative, co-led by nations like the U.S., Japan, and European countries, aims to fund early coal plant retirements and accelerate renewable energy adoption.

However, progress has been slow. Much of the pledged funding remains undelivered, with officials expressing the urgency of receiving the support to achieve its goals.

President Prabowo’s announcement underscores Indonesia’s intent to lead by example, revealing a more aggressive approach toward reducing carbon emissions. His predecessor initiated the JETP deal, but Prabowo’s leadership seeks to overcome the challenges that have stalled its progress.

Earlier this month, Indonesia inked a $10 billion agreement with China at the Indonesia-China Business Forum. The event focuses on economic growth in clean tech, biotechnology, water conservation, and mining.

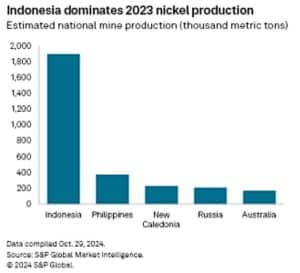

Indonesia’s nickel industry remained a focal point, with Chinese firms like GEM Co. partnering with PT Vale on a $1.42 billion HPAL plant. Investments by Tsingshan and Huayou Cobalt further affirm Indonesia’s vital role in supplying nickel for EVs, batteries, and green technologies.

Nickel and Nature: Leveraging Resources for Climate Goals

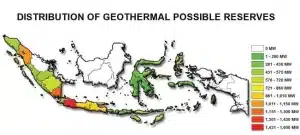

Indonesia plans to tap into its vast natural resources to drive its energy transition and reach net zero. The country is rich in geothermal energy, making it an ideal candidate for large-scale renewable energy projects.

Alongside geothermal, the government plans to expand solar and wind capacity to bridge the gap left by retiring fossil fuel plants.

Additionally, biodiesel production will play a significant role in the transition. Indonesia has been using palm oil to produce biofuels, and President Prabowo emphasized its importance in reducing dependence on coal and gas.

Beyond energy generation, Indonesia’s expansive rainforests offer a unique opportunity to generate carbon credits. The country aims to produce over 550 million tons of carbon credits, helping offset emissions and contributing to the global fight against climate change.

In September, President Prabowo unveiled plans for a $65 billion green economy fund by 2028. This innovative fund will leverage carbon credit sales from large-scale environmental projects, including forest preservation and reforestation. Managed by a “special mission vehicle,” the initiative will centralize sustainable activities nationwide.

- READ MORE: $65 Billion Green Fund from Carbon Credits Sale? Says Indonesia’s President-elect Prabowo Subianto

Bold Targets, Big Challenges: Will Indonesia’s Green Vision Succeed?

Hashim Djojohadikusumo, Indonesia’s climate envoy to COP29, outlined the nation’s target to install 100 GW of new energy capacity over the next 15 years. Of this, 75%—or 75 GW—will come from renewable energy sources. These projects will add to the country’s existing installed capacity of over 90 GW, of which coal currently dominates.

The plan involves a massive budget of $235 billion, technology, and scientific expertise.

However, the scale of these ambitions raises questions about feasibility. With renewables currently accounting for less than 15% of Indonesia’s energy mix, the road to 75 GW of renewable capacity will require significant investments in infrastructure, technology, and workforce training.

Moreover, the nation’s reliance on coal exports as a major revenue source adds economic complexity to the transition. Retiring coal plants will not only require financial support from international partners but also a clear strategy to manage the social and economic impacts on coal-dependent communities. Amid all these challenges, President Prabowo’s leadership signals a new chapter in Indonesia’s energy policy.

With global eyes on its progress, Indonesia’s journey to net zero will be a litmus test for the feasibility of large-scale energy transitions in emerging markets. If successful, it will show that even coal-reliant economies can shift toward sustainable energy with the right policies and support.

The post Indonesia’s Bold Push to Net Zero: Shutting Down All Coal Plants in 15 Years appeared first on Carbon Credits.