Colombia’s Largest Carbon Project Secures $100M Backing from Temasek-Owned GenZero and Trafigura

GenZero, a decarbonization-focused investment platform owned by Temasek, and global commodities trader Trafigura have committed over $100 million to Brújula Verde, Colombia’s largest nature-based carbon removal project. Located in the Orinoco River Basin, this project aims to restore land degraded by agriculture and wildfires while generating high-integrity carbon removal credits.

Bringing Degraded Lands Back to Life

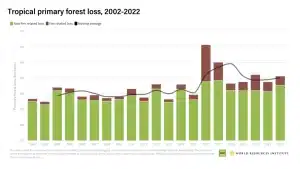

The planet is losing about 10 million hectares of forest worldwide every single year. The primary reason is to clear land for agriculture and materials like paper. This deforestation, largely concentrated in tropical forests (96%), contributes to 16% of total tree cover loss.

Notably, deforestation releases nearly 5 billion tons of carbon dioxide annually, accounting for about 10% of global human-made emissions. This is why most nature-based projects are focusing on restoring degraded forests.

In Colombia, 79,256 hectares were deforested in 2023. The South American nation is covered by over 60 million hectares of forests, with 405,000 hectares of planted forests.

The Brújula Verde project focuses on afforestation and reforestation across 30,000 hectares of degraded land, particularly areas previously used for cattle grazing. The initiative will plant 24 million mixed-species trees, with no plans for commercial harvesting.

- By restoring the land, the project could sequester over 20 million tonnes of carbon throughout its lifetime.

The project uses advanced technologies such as high-resolution sensors for accurate carbon monitoring and eDNA sampling to track biodiversity. It also assesses the health of local ecosystems, including their biodiversity, water systems, and social impacts.

Expanding the Project’s Scope

Trafigura initially invested in Brújula Verde in 2023, funding the first phase, which reforested 10,000 hectares. This latest investment, supported by GenZero, will double the project’s size and help it issue its first carbon credits by 2025.

Matthew Nelson, Head of Carbon Investments at Trafigura, highlighted the project’s potential to attract institutional investors and deliver environmental and social benefits. He stated that:

“GenZero’s partnership will enhance the scope and impact of Brújula Verde, bringing local employment alongside environmental and biodiversity benefits to the region, whilst producing high integrity nature-based carbon removal credits.”

Trafigura Sustainability and Climate Initiatives

Trafigura is a leading global commodity trading firm, specializing in the trading of oil, refined products, metals, and minerals. The company plays a vital role in connecting producers with consumers through efficient supply chains. In 2023, Trafigura reported revenues exceeding $315 billion, underscoring its significance in global markets.

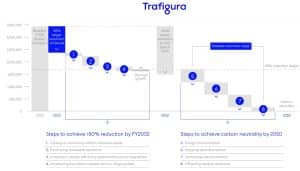

The global commodity trading giant is actively pursuing ambitious carbon reduction initiatives, aiming to align with global net-zero targets. It targets a 50% reduction in Scope 1 and 2 emissions by 2032 and operational carbon neutrality by 2050.

The company’s emissions reduction strategy also includes reducing its Scope 3 emissions intensity. These targets are complemented by investments in renewable energy projects, such as solar and wind. The company also invests in the development of low-carbon fuels, including green hydrogen and ammonia.

In 2023, Trafigura launched a $2 billion fund to support its energy transition projects. The company is also advancing its emissions trading activities, helping clients offset their carbon footprints by sourcing high-quality carbon credits. Trafigura’s climate action plan underscores its commitment to decarbonizing its supply chain and supporting global sustainability goals.

The $100 million investment in Colombia’s Brújula Verde project for nature-based carbon removals is the company’s most recent initiative.

Building High-Quality Carbon Markets

The project aims to contribute to the development of robust carbon markets by delivering high-quality, verifiable carbon removal credits. According to Hoon Ling Min, Director of Investments at GenZero, the project’s focus on soil restoration and native species reintegration ensures the production of top-tier carbon credits. He further noted that:

“The Brújula Verde project marks an important effort in restoring one of Colombia’s most biologically diverse areas. It is a unique project which adopts a restoration bridge concept by reconditioning soil health through reforestation, which enables the reintegration of native species gradually.”

GenZero, a wholly-owned subsidiary of Temasek, is committed to accelerating global decarbonization. The platform invests across three key areas:

- technology-based solutions,

- nature-based projects, and

- carbon ecosystem enablers.

GenZero has already deployed capital in impactful initiatives, including investments in Carbon Capture, Utilization, and Storage (CCUS) and nature-based solutions like sustainable forestry.

The company’s key achievements include reducing carbon emissions through clean cookstove projects in Southeast Asia and supporting the New Forests Tropical Asia Forest Fund 2. Together, these efforts contribute to advancing decarbonization by 2030, aligning with global net-zero goals.

The Brújula Verde project represents a significant step toward addressing climate change by restoring ecosystems and generating carbon credits. With GenZero and Trafigura’s combined investment, the project will deliver environmental, social, and economic benefits to the Orinoco River Basin while advancing the global carbon market.

The post Colombia’s Largest Carbon Project Secures $100M Backing from Temasek-Owned GenZero and Trafigura appeared first on Carbon Credits.

Image Source: Oklo Inc

Image Source: Oklo Inc