Saudi Arabia’s Carbon Ambition: NEOM’s Enowa and VCM Ink 30M Tonnes Carbon Credit Deal

The Voluntary Carbon Market Company (VCM) and Enowa, NEOM’s energy and water arm, have struck a landmark deal to deliver at least 30 million tonnes of high-integrity carbon credits by 2030. This long-term agreement shows Enowa’s promise to offset its unavoidable emissions. It also supports global climate action. This is especially true for projects in the Global South, which gain stable, long-term funding. The first delivery occurred in December 2024.

VCM launched Saudi Arabia’s first carbon credit exchange in November 2024. It was founded by the Public Investment Fund (PIF) with 80% ownership and the Saudi Tadawul Group with 20%.

The platform offers top-level carbon trading, clear price discovery, global registry access, and aims to support Islamic finance structures. It also operates an auction system and will introduce spot trading in 2025.

This agreement highlights the growing demand. The global voluntary carbon market is expected to rise from $2 billion in 2020 to $250 billion by 2050. This growth is fueled by both companies and projects.

A Game-Changing Carbon Credit Pact

The VCM–Enowa agreement is a big step in voluntary carbon markets. It moves from one-time purchases to a long-term approach. Under the deal, Enowa will secure 30 million tonnes of high-quality carbon credits by 2030—about 3 million tonnes annually. This steady volume helps stabilize the market for everyone. It also unlocks vital funding for climate projects worldwide.

For developers, especially in the Global South, such long-term offtake agreements mean:

- Reduce risk,

- Support scalability, and

- Allow for better project planning.

As VCM CEO Riham ElGizy noted:

“The long-term agreement between VCM and Enowa to facilitate the delivery of over 30 million tons of carbon credits by 2030 marks a significant moment in Saudi Arabia’s journey to drive growth in global voluntary carbon markets. It helps Enowa compensate for today’s emissions while creating sustainable infrastructure for the long term.”

Enowa, already active in previous VCM auctions, becomes the first company in Saudi Arabia to enter such a long-term deal. Acting CEO Jens Madrian said it reflects their commitment to NEOM’s goal of 100% renewable energy. NEOM’s green infrastructure vision aligns closely with Enowa’s emissions management strategy.

This deal is huge: 30 million tonnes over ten years equals the yearly emissions of a mid-sized industrial country. This sets a high standard for corporate climate action in the area.

Building a Mature Carbon Market in Saudi Arabia

The VCM–Enowa deal also strengthens Saudi Arabia’s growing carbon trading ecosystem. Launched in November 2024, VCM’s voluntary carbon exchange is the Kingdom’s first institutional-grade platform. It provides key market tools such as auctions, RFQ features, block trades, and a new spot market. These tools improve price transparency, boost liquidity, and give access to a global registry.

Through successful auctions in 2022, 2023, and 2024, VCM has transacted over 4.7 million tonnes of carbon credits with buyers from 15+ countries. Projects include reforestation, soil carbon, clean cookstoves, and renewables. These show a strong demand for quality credits in many regions.

VCM stands out by aligning with both international standards and regional needs. It is creating Shariah-compliant infrastructure. This allows more MENA-based investors to use ethical finance tools. Its support ecosystem helps project developers in Africa and the Middle East. It includes advisory services and registry integrations. This way, developers can gain visibility and find long-term buyers.

This platform arrives as voluntary carbon markets face scrutiny over credibility. Backed by PIF and Tadawul, VCM provides a transparent, high-integrity marketplace. As ICVCM and COP29’s Article 6.4 advance global standards, VCM is positioning itself to lead regionally and globally.

Saudi Arabia aims to replicate its energy market leadership in climate finance. VCM’s success could channel billions into emerging economies and close the climate finance gap—estimated at $1.5–$2 trillion annually by the UN and World Bank. Voluntary carbon markets are increasingly vital to this mission.

Enowa and NEOM: A Blueprint for Net Zero

Enowa, the energy and water subsidiary of NEOM, plays a central role in advancing Saudi Arabia’s carbon neutrality goals. As part of the futuristic NEOM development, Enowa is building a 100% renewable-powered energy system that relies on solar, wind, green hydrogen, and cutting-edge digital infrastructure. This carbon-free framework is central to NEOM’s ambition to become a global model for low-emission urban living.

Enowa’s long-term agreement with VCM reflects its strategy to tackle unavoidable emissions through high-integrity carbon credits, complementing its broader sustainability efforts.

The company is actively involved in deploying smart grid technologies and water recycling systems that support circular economies. Its approach aligns with international net-zero frameworks, aiming to drastically reduce operational emissions while fostering innovation in climate resilience.

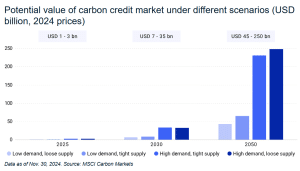

$250B and Counting: Why Voluntary Carbon Markets Are Booming

Voluntary carbon markets are set for explosive growth. Reports predict an increase from $2 billion in 2020 to $250 billion by 2050, with interim estimates ranging from $45 billion to $100 billion by 2030.

MSCI forecasts market expansion from $1.4 billion in 2024 to potentially $35 billion in high-demand scenarios by 2030. Around the world, projects that cut or eliminate carbon are getting more funding through voluntary carbon credits. There is strong demand for credits that also support community development and protect biodiversity.

Why Corporate Commitments Demand Certainty

Companies—especially those in tech, energy, and manufacturing—seek reliable offsets to meet net-zero goals. Long-term purchase agreements like VCM–Enowa’s offer greater credibility and transparency than spot buys.

They make sure that top-quality credits come from projects in developing countries. This aligns emissions cuts with sustainable development. In turn, these agreements help build carbon market capacity in the Global South.

Challenges and the Path to Integrity: Fixing Trust in Carbon Credits

However, voluntary carbon markets face credibility issues. High-profile cases, such as problems in Kenya’s Northern Rangelands project—backed by Meta and Netflix—have sparked concerns. With Verra reviewing the project amid legal and environmental scrutiny, trust in carbon credits has taken a hit.

New rules from COP29’s Article 6.4 and efforts like ICVCM’s framework seek to enhance market integrity and transparency.

VCM’s institutional focus, long-term contracts, and integration with recognized standards are designed to reduce these risks by ensuring quality and oversight.

Saudi Arabia’s Big Carbon Bet Has Global Stakes

Meanwhile, Saudi Arabia’s move through VCM positions it at the forefront of voluntary carbon market expansion in the Middle East. Globally, Asian and South American countries are also scaling their own platforms and frameworks. Deals involving multinational firms and sovereign or semi-sovereign buyers lend scale and legitimacy to these markets.

This shift supports climate finance goals:

- Global climate funding currently stands at roughly $120 billion annually for low‑ and middle‑income countries, well short of the $300 billion yearly target by 2035 agreed at COP29.

Carbon markets like VCM can help fill that gap, particularly in driving private investment.

The VCM–Enowa agreement sets a new standard in voluntary carbon trading—long-term, high-volume, and high-integrity. Voluntary markets will likely grow a lot in the coming decades, and deals like this build trust and stability. They also provide financial security for climate projects in developing economies. With improved standards in place, voluntary carbon credits can become a powerful tool in global efforts to reach net-zero.

The post Saudi Arabia’s Carbon Ambition: NEOM’s Enowa and VCM Ink 30M Tonnes Carbon Credit Deal appeared first on Carbon Credits.