Power Surge: Can Carbon Capture Keep Up with AI’s Energy Demand?

Electricity demand in the United States is rising faster than it has in decades. For years, power use remained steady due to efficiency improvements and shifts in industrial activity. However, recent changes have increased demand significantly.

More people are using electric vehicles (EVs), new factories are opening, and artificial intelligence (AI) is expanding. These factors require more electricity, putting pressure on the U.S. power grid.

One of the biggest drivers of power demand is the rapid growth of data centers. These facilities store and process massive amounts of digital information. Cloud computing, AI, and streaming services all rely on data centers, which require a steady and reliable power supply.

Many power companies have raised their peak electricity demand forecasts by over 50% in just three years, according to a paper by Carbon Direct.

Natural Gas and the Challenge of Lowering Emissions

Currently, natural gas supplies about 40% of the electricity in the U.S. It is the largest energy source for power generation. While renewable energy like wind and solar is expanding, natural gas remains important because it provides steady power, unlike solar panels or wind turbines, which depend on weather conditions.

The downside of natural gas is that burning it releases carbon dioxide (CO₂), a greenhouse gas that contributes to climate change. To meet energy needs while reducing emissions, power companies are looking at carbon capture and storage (CCS). This technology captures CO₂ before it enters the atmosphere and stores it underground.

- CCS can reduce carbon emissions from natural gas plants by 90-95%.

How Carbon Capture Works

Carbon capture technology uses chemical reactions to separate CO₂ from power plant emissions. The captured CO₂ is then compressed and transported to a storage site. It is injected deep underground into rock formations, where it stays permanently. If a storage site is not nearby, the CO₂ must be transported by pipeline, truck, or rail.

Not all power plants are suitable for carbon capture. The technology works best on large power plants that operate continuously. Smaller or backup plants that only run occasionally are not good candidates for CCS because the capture process is expensive and requires steady operation.

The Cost of Carbon Capture

Adding CCS to a power plant increases costs. The price of electricity from a natural gas plant without CCS is estimated at $40–$70 per megawatt-hour (MWh). With CCS, the cost rises to $65–$100 per MWh. These costs come from the capture equipment, extra fuel needed for the process, and the expense of transporting and storing CO₂.

However, tax credits can help reduce the cost. In the U.S., a program called 45Q offers financial incentives for capturing and storing carbon. These incentives make CCS more affordable and encourage companies to invest in clean energy solutions.

Capturing the advantages of natural gas plant with CCS, the Carbon Direct paper noted:

“Natural gas-fired power generation can be built in locations that do not have enough land area available for renewable forms of power generation like wind and solar. They can often be sited conveniently close to electricity transmission infrastructure and end users. Natural gas-fired power generation with CCS is competitive with both geothermal and nuclear electricity in terms of providing enough baseload power. Further, it offers cost advantages and is speedier to bring to market.”

Tech Giants in Trouble: How Carbon Capture and Carbon Credits Can help

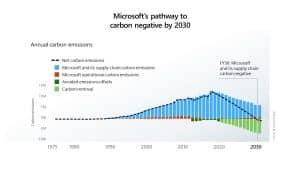

Tech companies like Google and Microsoft are under pressure to reduce emissions from their data centers. AI computing requires huge amounts of power, and companies need clean energy solutions. Many large tech firms have set goals to cut their carbon footprints, but their emissions are rising due to energy demand.

For example, Google’s emissions increased by 13% in 2023 because of higher energy use in data centers. Microsoft has also highlighted the need to clean up its supply chains.

Since data centers need constant power, natural gas plants with CCS could be a solution for providing clean, reliable electricity.

The Role of Carbon Credits

Carbon credits are an important part of reducing emissions. A carbon credit represents one metric ton of CO₂ that is either reduced or removed from the atmosphere. Companies that emit CO₂ can buy carbon credits to offset their emissions.

With CCS, power plants can earn carbon credits by capturing and storing emissions. These credits can be sold to companies needing to meet their climate goals. This system helps create a financial incentive for reducing carbon pollution.

By combining CCS with carbon credits, power producers can reduce costs while helping businesses achieve net-zero targets.

Future Outlook: The Need for More Investment

Experts agree that carbon capture must expand if the U.S. wants to lower emissions while maintaining a reliable power supply. The International Energy Agency (IEA) warns that current investments in CCS are not enough.

Without new projects, carbon emissions from power generation will remain high. The supply gap could reach 1.2 billion metric tons of CO₂ per year by 2050, making it much harder for industries like power generation to reduce their emissions.

Companies planning new power plants should consider making them “capture-ready.” This means designing them so CCS can be added later. However, delaying CCS for too long could increase emissions and make it harder to meet climate goals.

This shortfall highlights the urgent need for increased investment in CCS technology and infrastructure to ensure a significant reduction in carbon emissions from natural gas power plants and other high-emission sectors.

According to the IEA, achieving net-zero greenhouse gas emissions by 2050 requires scaling up CO₂ capture capacity to 1.7 gigatons annually by 2030. This ambitious target requires a substantial financial commitment.

Estimates indicate that capital investments ranging from $665 billion to $1.28 trillion are required by 2050 to scale CCUS. Per McKinsey & Company, annual investment in this technology will hit up to $150 billion after 2035.

Challenges of Carbon Capture

While CCS has benefits, it also faces challenges:

- High Costs: The technology is still expensive, although tax incentives help.

- Infrastructure Needs: Transporting CO₂ requires pipelines, which can take years to build.

- Public Concerns: Some communities worry about storing CO₂ underground.

- Energy Use: CCS requires extra energy, which slightly reduces power plant efficiency.

Despite these challenges, many experts believe that CCS is necessary for reducing emissions in industries that cannot fully switch to renewables, such as steel, cement, and natural gas power.

The demand for electricity is growing, especially due to AI and data centers. While renewable energy is expanding, natural gas remains essential for providing steady power. To reduce emissions, carbon capture technology can be used to trap and store CO₂ from power plants.

CCS can cut emissions by up to 95% and provide low-carbon electricity. Although it is expensive, tax credits and carbon credits can help make it more affordable. As businesses and governments work toward cleaner energy, investing in CCS will be crucial for balancing energy demand with climate goals.

The post Power Surge: Can Carbon Capture Keep Up with AI’s Energy Demand? appeared first on Carbon Credits.