https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2025-01-17 05:22:322025-01-17 05:22:32Protected: Top 4 Carbon Projects in 2025: The Game-Changers in Climate Action You Need to Know Ads

In the fight against climate change, companies big and small face mounting pressure to take responsibility for their carbon footprint. Despite rigorous efforts to reduce greenhouse gas (GHG) emissions, certain hard-to-abate emissions persist—those that cannot be entirely avoided due to technological or operational constraints. Carbon offsetting offers an effective solution for addressing these residual emissions.

Why Do Carbon Offset Projects Matter?

Carbon offset projects are verified initiatives designed to reduce, avoid, or remove GHG emissions from the atmosphere. These projects span various activities, such as protecting natural ecosystems, reforestation, afforestation, and deploying clean energy technologies.

Each tonne of reduced emissions generates a carbon credit, which individuals and companies can purchase to offset their footprints. Notably, removal credits have reached their largest share of retirement activity, signaling a growing shift toward projects that directly eliminate CO₂ from the atmosphere.

For businesses facing the urgency of reducing their environmental impact, carbon offsetting provides a tangible, immediate action. By investing in offset projects, companies can achieve carbon neutrality as well as contribute to sustainable development goals. Below are the top ten carbon credit buyers in 2024, according to the Allied Offsets report.

However, the success of carbon offsetting depends on proper implementation. When done right, these projects can significantly benefit the climate while ensuring meaningful impacts on-site. If done improperly, they risk being seen as a shortcut rather than a complement to essential internal emission reductions.

Given the growing need for corporate accountability, the decision to invest in top-tier carbon offset projects is both strategic and impactful. Here are the top four carbon projects that are worth considering in 2025.

TerraPass: Driving Measurable Impact in Carbon Offsets

TerraPass has been a pioneer in carbon offsets, making sustainability accessible for individuals and businesses since its founding in 2004. To date, TerraPass has offset over 43 million metric tons of CO₂, equivalent to removing more than 9.3 million cars from the road for a year.

The organization supports a wide range of verified projects that directly reduce greenhouse gas emissions, with over 200,000 customers across the globe. One notable initiative is landfill gas capture, which prevents harmful methane emissions from entering the atmosphere. Methane is 25 times more potent than CO₂, and TerraPass’s efforts in this area have a significant climate impact.

TerraPass’s key projects include:

Ideal Family Farms Methane Capture Project (Wisconsin): This project reduces methane emissions by converting agricultural waste into renewable energy, preventing harmful gases from entering the atmosphere.

New Bedford Landfill Gas-to-Energy Project (Massachusetts): This initiative captures landfill gas and converts it into energy, reducing emissions while providing a sustainable energy source.

Waymart Wind Energy Project (Pennsylvania): A wind farm that generates renewable energy, displacing fossil fuel-based electricity generation.

For individuals, TerraPass offers carbon offset packages starting at just $5.99 per month, covering emissions from everyday activities like driving, flying, and household energy use. Their simple carbon calculator helps users identify their footprint and take immediate action.

Businesses can integrate TerraPass into their sustainability strategies with tailored solutions for events, supply chains, or entire operations. Companies like Subaru and Amtrak have partnered with TerraPass to meet corporate social responsibility (CSR) goals, demonstrating its credibility among industry leaders.

The carbon offset provider is transparent about its impact, providing third-party verification for all projects under standards like the Verified Carbon Standard (VCS) and Climate Action Reserve (CAR). This ensures contributions make a measurable difference.

Whether it’s reducing methane, generating clean energy, or offsetting daily activities, TerraPass transforms complex sustainability challenges into actionable steps toward a greener planet.

So, why TerraPass?

Backed by Green-e Climate certification to ensure quality and credibility.

Offers user-friendly tools, such as an advanced carbon calculator, to educate and engage individuals and businesses.

Supports multiple verified projects, ensuring transparent and impactful results.

3Degrees: Advancing Global Sustainability Through Innovative Solutions

3Degrees is a trailblazer in climate solutions, empowering organizations worldwide to achieve renewable energy and carbon reduction goals. Founded in 2007, the company has facilitated over 10 million metric tons of CO₂ reductions, equivalent to the annual energy use of about 1.2 million homes.

The company specializes in renewable energy certificates (RECs), carbon offsets, and consulting services. 3Degrees has helped over 4,000 organizations transition to sustainable energy practices, including industry leaders like Google, Microsoft, and LinkedIn. 3Degrees ensures impactful and lasting contributions to global climate goals by enabling these companies to meet their sustainability commitments.

One of the standout achievements of 3Degrees is its work in renewable energy procurement. It has facilitated over 10 gigawatts of renewable energy transactions globally, supporting solar, wind, and other clean energy projects. These efforts have significantly reduced dependency on fossil fuels and accelerated the transition to a low-carbon economy.

The key projects supported by 3Degrees are:

Cookstove Project in Uganda: This initiative provides energy-efficient cookstoves to communities, significantly reducing deforestation and indoor air pollution. The project improves public health while lowering greenhouse gas emissions.

Kootznoowoo Forestry Project (Alaska): A forest management program led by Indigenous communities that preserves old-growth forests, enhances biodiversity, and sequesters carbon.

Solar Water Heater Initiative in India: By installing solar water heaters in rural households, this project promotes renewable energy use and reduces dependency on fossil fuels, cutting emissions while supporting sustainable development.

3Degrees is also a champion of equity-focused climate solutions. Through projects like forest conservation in the Amazon and clean cookstove initiatives in sub-Saharan Africa, the company mitigates emissions while supporting local communities. These initiatives often deliver secondary benefits, such as improved air quality and job creation, amplifying their positive impact.

For businesses seeking net-zero goals, 3Degrees offers strategic consulting services. Their expertise ensures companies align with frameworks like the Science-Based Targets initiative (SBTi) and adhere to global reporting standards.

With recognition as a certified B Corporation, 3Degrees combines profit with purpose. Its mission to “connect people with solutions needed to combat climate change” reflects its dedication to building a sustainable future.

From large corporations to local governments, 3Degrees delivers actionable, measurable, and transformative climate solutions that make a global impact.

Why pick 3Degrees?

Custom climate solutions for corporations aiming to meet their sustainability goals.

Proven expertise in renewable energy procurement and supply chain decarbonization.

Facilitates broader access to clean energy for businesses and consumers alike.

Rimba Raya Biodiversity Reserve: Protecting Nature, Empowering Communities

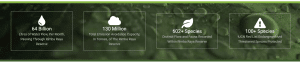

The Rimba Raya Biodiversity Reserve stands as one of the largest REDD+ (Reducing Emissions from Deforestation and Forest Degradation) projects in the world, spanning over 64,000 hectares of tropical peat swamp forest in Central Kalimantan, Indonesia.

The project has a dual mission: combating deforestation and preserving biodiversity while uplifting local communities.

Since its establishment, Rimba Raya has prevented the emission of over 130 million metric tons of CO₂. That equals taking about 28 million cars off the road for a year. Its efforts focus on protecting critical ecosystems that act as carbon sinks, particularly peatlands, which store up to 10 times more carbon than other forest types.

The reserve is home to more than 300 species, including endangered animals like the Bornean orangutan. The project supports rehabilitation programs and has partnered with the Orangutan Foundation International to create habitats for over 350 rescued orangutans.

Rimba Raya’s impact extends beyond environmental preservation. It works closely with 14 villages surrounding the reserve, positively affecting over 10,000 people.

Initiatives include access to clean water, educational programs, and alternative livelihood opportunities, such as sustainable farming and aquaculture. These programs aim to reduce dependency on forest exploitation while improving the well-being of local communities.

The project operates under rigorous certification standards, including the Verified Carbon Standard (VCS) and Climate, Community, and Biodiversity Standards (CCBS). These certifications ensure transparency, accountability, and measurable results.

Rimba Raya’s holistic approach showcases how conservation can balance environmental, social, and economic goals. As a model for REDD+ projects worldwide, it demonstrates that protecting nature and empowering people go hand in hand in addressing climate change.

What makes Rimba Raya noteworthy?

Directly combats deforestation linked to palm oil plantations.

Focuses on biodiversity conservation and sustainable development for local communities.

Aligned with all 17 UN Sustainable Development Goals (SDGs).

MyClimate: Shaping a Sustainable Future

MyClimate is a globally renowned organization offering high-quality carbon offset solutions and climate education programs. Headquartered in Switzerland, MyClimate has been at the forefront of climate action since 2002. To date, it has offset over 19 million metric tons of CO₂ through more than 174 projects worldwide.

The organization focuses on projects that deliver measurable environmental, social, and economic benefits. These include the following initiatives:

Efficient Cookstove Program (Kenya): This initiative distributes energy-efficient cookstoves to rural households, reducing wood consumption by up to 50%. It helps mitigate deforestation, lowers CO₂ emissions, and improves indoor air quality, benefiting families’ health and the environment.

Reforestation in Nicaragua: MyClimate partners with local farmers to restore degraded land through reforestation. This project sequesters carbon, enhances biodiversity, and provides economic benefits to local communities.

Solar Energy for Schools (Tanzania): By installing solar panels in off-grid schools, this project provides renewable energy, enabling better lighting and access to educational resources. It also reduces dependency on fossil fuels, cutting emissions and operational costs.

Biogas Systems in India: This program supports rural families by providing biogas digesters that convert organic waste into clean cooking gas. The project reduces greenhouse gas emissions and reliance on firewood while improving living conditions.

MyClimate’s approach combines innovation with accountability. All projects adhere to rigorous international standards, such as Gold Standard and Plan Vivo, ensuring they deliver real and lasting impact.

MyClimate also partners with companies to create customized sustainability strategies. Brands like Lufthansa and Hilton Worldwide have leveraged MyClimate’s expertise to align their operations with global climate goals. These collaborations highlight the project’s role as a trusted partner in achieving net-zero targets.

One of its remarkable programs, “Cause We Care” empowers companies and customers to support sustainable tourism. Businesses commit to climate action, and customer contributions fund climate projects and local sustainability efforts. This innovative initiative combines emissions reductions with meaningful environmental and social impacts, fostering responsible travel and eco-conscious development worldwide.

What makes MyClimate stand out?

Combines high-quality carbon offset projects with impactful education programs.

Over 74,000 climate pioneers trained and supported globally.

Tailored solutions and tools for individuals and businesses simplify climate action.

Taking Action for a Sustainable Future

Investing in carbon offset projects is a powerful step toward combating climate change while addressing hard-to-abate emissions. With the voluntary carbon market evolving and more companies prioritizing quality and transparency, initiatives like TerraPass, 3Degrees, Rimba Raya, and MyClimate stand out as impactful solutions.

These projects reduce greenhouse gas emissions while promoting biodiversity, create jobs, and improve living conditions in local communities. Keep an eye on these impactful initiatives as they continue to lead the charge in 2025 and beyond. Together, we can take meaningful action today for a greener, more sustainable tomorrow.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2025-01-16 14:50:302025-01-16 14:50:30Top 4 Carbon Projects in 2025: The Game-Changers in Climate Action You Need to Know

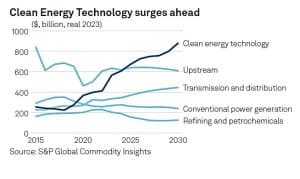

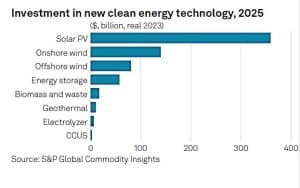

The global energy landscape is undergoing a seismic shift, with 2025 poised to mark a pivotal year for clean energy technologies. According to S&P Global Commodity Insights’ latest report, cleantech energy supply investments will surpass upstream oil and gas spending for the first time, underscoring the growing dominance of renewables in shaping energy production and consumption.

A Billion-Dollar Leap: Clean Energy Investments Overtake Oil & Gas

In 2025, cleantech energy supply spending is forecast to reach $670 billion, a historic milestone in the energy transition as shown below by S&P Global analysis. That figure will further increase by 2030, creating a huge gap between clean energy technology and upstream oil and gas investments.

Solar PV alone is expected to account for half of this investment and two-thirds of installed megawatts. It is then followed by onshore wind investment.

However, despite this financial commitment, current investment levels fall short of the climate goal to triple renewable capacity by 2030. The International Energy Agency’s (IEA) net zero roadmap specifically outlines this as a crucial climate ambition to achieve.

IEA’s Roadmap to Net Zero by 2050

Regionally, China’s capital efficiency in renewable energy investments leads the charge. Projections indicate nearly twice the gigawatts added per dollar spent compared to the U.S. This advantage solidifies China’s role as a major player in renewable energy expansion, even as global supply chain tensions present challenges.

Cleantech Supply Chain Tensions

China remains a dominant force in solar, wind, and battery manufacturing. However, its expansive supply chain faces pressures from a slowing domestic economy. The oversupply of equipment from China continues to drive prices down globally, reshaping industry dynamics.

S&P Global projections further suggest that by 2030, China’s market share in PV module production will decline to 65%, and battery cell manufacturing will drop to 61%. While this diversification may alleviate dependence on a single market, it also raises questions about how other nations will scale their production capabilities.

Battery Storage: The Missing Piece to Renewable Viability

Battery energy storage is becoming indispensable for renewable energy projects, particularly in regions with high solar PV penetration. While solar costs have declined significantly, developers face economic hurdles due to low power purchase agreement (PPA) expectations and the “cannibalization” effect—where midday energy overproduction drives prices to negligible levels.

To address these challenges, integrating battery energy storage has emerged as a critical strategy. Storage solutions enable renewable projects to stabilize energy output and optimize market participation, making investments more financially viable.

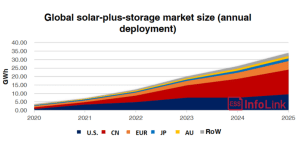

A good example that many call solar-plus-storage system is beginning to gain attention in the U.S. This system is transforming the renewable energy landscape.

By pairing solar panels with battery storage, solar-plus-storage systems address solar power’s intermittency and timing challenges. These hybrid systems provide a steady energy supply, boost grid reliability, and open new revenue streams for solar plants.

Solar facilities can earn through capacity payments and arbitrage—buying energy at lower prices, storing it, and selling when demand drives prices higher. China and the U.S. will continue to dominate this market.

Chart from infoLink

Smart Grids and Smarter Strategies: AI’s Role in the Energy Evolution

Artificial intelligence (AI) is revolutionizing the cleantech sector, particularly in grid planning and renewable energy forecasting. Accurate predictions of intermittent renewable energy generation are crucial to maintaining grid stability.

For instance, AI-driven predictive maintenance for wind farms reduces downtime and increases energy production by up to 30%. AI also improves grid performance, reducing congestion and integrating more renewables without costly infrastructure upgrades.

Moreover, AI-powered trading applications help mitigate risks arising from forecast discrepancies, which can vary by as much as 700%. By enhancing energy management, AI facilitates smoother integration of renewables into the grid.

AI’s impact on grid-enhancing technologies has helped increase grid capacity by 20%, supporting the growing share of clean energy. Additionally, companies like Google, Microsoft, and Tesla are investing heavily in AI, with Tesla’s AI-driven energy storage solutions improving battery performance and extending lifespan by 15%.

However, the rise of AI also introduces risks, including cybersecurity vulnerabilities and ethical concerns, which will require proactive governance to address.

Meanwhile, data centers are also becoming a driving force in corporate clean energy procurement. Currently, these energy-intensive facilities account for 200 TWh, or 35%, of global corporate clean energy purchases. By 2030, their demand is projected to rise to 300 TWh annually, with North America leading this surge.

The growing role of data centers reflects the broader corporate commitment to sustainability, as businesses increasingly prioritize renewable energy to meet climate goals and manage operational costs.

Charging Ahead: 2025 and the Clean Energy Revolution

2025 represents a transformative year for clean energy technologies, with investments and innovations accelerating the global energy transition. From renewable energy expansion to advances in storage systems, the sector is rapidly evolving to meet ambitious climate targets.

Though challenges such as supply chain tensions, economic hurdles, and investment gaps persist, the collective commitment to sustainability and decarbonization signals a promising future for cleantech. As AI, storage solutions, and corporate procurement strategies redefine the energy landscape, 2025 will solidify clean energy’s role as the cornerstone of a sustainable, resilient global economy.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2025-01-16 14:50:302025-01-16 14:50:302025: The Year Clean Energy Dominates with Record $670 Billion Investment, Trumping Oil & Gas

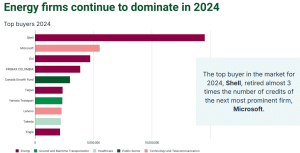

In the race to offset their carbon footprints, two giant companies—Shell and Microsoft—stand out as the largest carbon credit buyers in 2024, according to the Allied Offsets report. Their massive retirements reflect differing strategies and priorities, however, signaling distinct approaches to tackling carbon emissions through carbon markets.

Shell, the world’s largest fossil fuel company, and Microsoft, a technology leader, have been pivotal players in the voluntary carbon market (VCM). However, their activities reveal stark contrasts in how they approach sustainability goals and what projects they support.

Meanwhile, the broader carbon credit market in 2024 showed a growing emphasis on removals and diversification of project types.

Shell: The Emission Offset Leader

Shell retained a massive 14.5 million carbon credits in 2024, taking the top spot for the second consecutive year. This commitment is a significant part of Shell’s strategy to offset its extensive emissions.

Unlike Microsoft, which has heavily invested in carbon removal technologies, Shell’s purchases mainly target projects focused on emissions avoidance.

A large portion of Shell’s credits—9.4 million—came from forestry and land-use initiatives. These projects, focusing on protecting and managing forests to prevent the release of stored carbon, are cost-effective but also face scrutiny over integrity concerns. Interestingly, the energy giant announced plans in November last year to sell part of its nature-based carbon projects.

The company also retired 2.4 million renewable energy credits, a cheaper and more widely accepted option in the market.

Chart from Allied Offsets Report

Moreover, the price difference between Shell’s credits and Microsoft’s illustrates their contrasting strategies. While Shell paid an average of $4.15 per credit, it remains focused on more affordable projects, including renewable energy and forestry.

Despite criticisms over the quality of some of its projects, Shell continues to be a significant player, aligning its credit purchases with its ongoing goal of achieving net-zero emissions by 2050. To achieve that, the oil major aims to reduce emissions from its operations by 50% by 2030, using 2016 baselines.

Image from Shell report

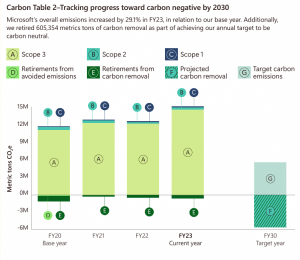

Microsoft: A Carbon Removal Champion

In contrast, Microsoft has pursued a more aggressive approach toward carbon removal, setting itself apart with a robust commitment to investing in innovative carbon capture technologies. The company retired 5.5 million credits in 2024, a distant second to Shell. However, the type of credits the tech giant bought tells a different story.

A key focus for Microsoft has been on bioenergy with carbon capture and storage (BECCS). It is an expensive and emerging technology that is capable of delivering carbon-negative results. BECCS works by capturing the carbon dioxide released during the burning of biomass and storing it underground.

Nearly 80% of Microsoft’s 2024 carbon credits came from BECCS projects, with the largest purchase of 3.3 million credits coming from Sweden’s Stockholm Exergi. While this technology is still in its infancy, it plays a critical role in global pathways to achieving net-zero emissions.

Microsoft’s strategy, however, is not without its challenges. BECCS credits are costly, with average prices of $389 per credit—substantially higher than the costs associated with Shell’s projects.

In 2024, Microsoft’s average credit price was $189, a significant investment considering its aim to neutralize emissions across its operations.

Despite the high costs, Microsoft’s commitment to carbon removal reflects its leadership in the tech industry’s broader sustainability agenda. The major tech company aims to be carbon-negative by 2030.

Image from Microsoft

Microsoft’s strategy to focus on carbon removals seems to be on the right track. The broader carbon market trend reveals the growing interest in carbon removal credits.

Carbon Market Dynamics: Increasing Focus on Quality and Carbon Removal Credits

The VCM in 2024 has shown signs of shifting, with a significant uptick in carbon removal credits, per the report. However, overall retirement activity in the VCM plateaued, with 2024 marking the third consecutive year of minimal growth.

Chart from Allied Offsets report

The decrease in market growth is not necessarily a negative development, as more buyers have shifted toward high-quality, impactful projects.

While Shell and Microsoft represent the extremes in carbon credit purchasing, other buyers are increasingly exploring removals and non-traditional carbon offset projects. Removals, such as those associated with BECCS, saw a larger share of the market, though they still constitute a small portion overall.

This shift reflects a broader trend toward supporting innovative carbon removal solutions, which can deliver long-term, lasting environmental benefits. Another report by the MSCI also reveals the same trend—demand for carbon removal credits is rising.

The market’s composition is also diversifying. Projects related to renewable energy and forestry still dominate. However, their share in total credit retirements has decreased from 80% in 2020 to 70% in 2024.

At the same time, new entrants into the market are pushing for more varied solutions, including technologies for direct air capture and carbon removal, which add complexity to an already challenging marketplace.

Challenges for Credit Buyers and the Market

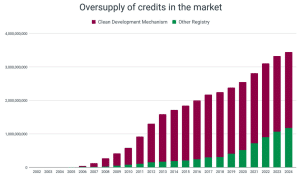

One of the major challenges for buyers is the oversupply of carbon credits in the market, which continues to grow. In 2024, the number of issued but not retired credits increased again, contributing to a potential glut in available credits.

This dynamic is particularly evident in the market for older Clean Development Mechanism (CDM) credits, which have increasingly been criticized for their lack of additionality and impact.

Chart from Allied Offsets report

Despite these challenges, the number of active buyers in the VCM continues to grow. In 2024, more than 6,500 companies participated in the market, a slight increase compared to previous years.

The vast majority of carbon credit buyers continue to come from the financial and energy sectors, with Microsoft representing a key player in the tech space. Even though more companies are entering the market, the rate of growth has slowed. This suggests that carbon credits are becoming a more established component of sustainability strategies.

As we move into 2025, the divergent strategies of Shell and Microsoft may serve as a model for others seeking to engage with the VCM. Shell’s focus on affordability and scale contrasts with Microsoft’s commitment to cutting-edge carbon removal technologies.

Yet, both companies are working towards a common goal—neutralizing their emissions and supporting global climate efforts.

As the market continues to evolve, these two companies are likely to remain at the forefront of shaping how businesses approach their carbon footprint and the critical role carbon credits play in the global fight against climate change.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2025-01-16 11:02:232025-01-16 11:02:23Shell and Microsoft Are The Biggest Carbon Credit Buyers in 2024: What Projects Do They Support?

Greenland, the world’s largest island, is attracting serious global attention. It lies between the Arctic and Atlantic Oceans which makes it strategically important. In 2019, President Donald Trump made waves by suggesting that the U.S. purchase Greenland. Although his proposal was rejected by both Greenlandic and Danish leaders, it highlighted the growing international interest in the icy island.

However, history seems to be repeating itself, as Trump has once again expressed a strong interest in purchasing Greenland during his second tenure.

Why Trump Wants to Buy Greenland?

The idea of the U.S. buying Greenland stemmed from its advantageous location in the Arctic. As climate change melts ice, new shipping routes are opening, making Greenland an even more valuable asset.

Beyond its geographical importance, the island is rich in untapped resources such as rare earth metals, oil, gas, and minerals—critical for industries like technology and defense. With its vast mineral wealth, military significance, and new opportunities brought by climate change, Greenland is rapidly becoming an exciting and attractive place for investment, particularly in the mining sector.

Additionally, securing access to Greenland’s resources could reduce U.S. reliance on imports from countries like China.

Though Trump’s plan didn’t move forward, it highlighted Greenland’s growing geopolitical importance and opened doors for investments, especially in its mining industry. In this article, we’ll highlight three companies to watch in Greenland’s booming mining industry as 2025 unfolds.

1. Amaroq Minerals: Sustainable Growth in Gold Exploration

Amaroq Minerals, founded in 2017, provides sustainable mineral solutions to meet global energy demands. Specializing in gold exploration, the company is actively exploring Greenland’s vast mineral resources. It holds an impressive license portfolio covering 6,072.5 km² in South Greenland.

As of January 2025, Amaroq’s market capitalization stands at around CAD 827 million. This reflects a remarkable growth of over 200% in the past year. The company’s recent accomplishments include discovering high-grade gold at its Eagle’s Nest Exploration Project and starting production at the Nalunaq Mine, one of Greenland’s oldest and richest gold deposits.

Moving on, Amaroq aims to minimize its environmental impact. The company focuses on responsible resource management and conserving biodiversity. By committing to sustainable mining practices, it plays a significant role in the global energy transition.

Source: Seeking Alpha

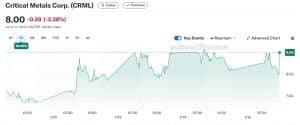

2. Critical Metals: Capitalizing on Rare Earth Elements

Critical Metals Corp is a pioneer in the mining of rare earth elements and critical minerals. The company focuses on recycling industrial by-products, including lithium batteries, to extract valuable metals for the energy transition. This approach supports the European lithium battery supply chain and promotes a circular economy.

One of Critical Metals’ most significant projects is the Tanbreez Rare Earth Mine in Southern Greenland. The mine holds some of the world’s highest-grade rare earth elements, including gallium, a metal used in the electronics and renewable energy industries. Critical Metals has been making strides in advancing sustainable mining processes, including partnerships to improve the recovery of these critical materials.

As of January 2025, Critical Metals has seen a tremendous surge in its market cap, reaching approximately $670.63 million—a staggering increase of over 550% from the previous year. The company’s growth shows investor trust in its ability to provide key metals for Europe’s electrification and energy storage needs.

Source: Yahoo Finance

3. Greenland Resources: Exploring Molybdenum

Greenland Resources Inc. is advancing the Malmbjerg Molybdenum Project in eastern Greenland. This world-class deposit of molybdenum, with copper nearby, is vital for several industries, including steel manufacturing and defense. As of January 2025, its market capitalization is approximately CAD 90.15 million, a 43.92% increase over the past year.

The company has made significant progress in obtaining the necessary environmental and social approvals for its project. The company is also working closely with partners like Rasmussen Global to secure funding from supranational organizations such as NATO’s Innovation Fund.

Molybdenum is critical for military defense and technology, and Greenland Resources’ Malmbjerg Project could supply up to 25% of the EU’s molybdenum needs for decades. Talking about sustainability, the company is using wind and solar power to supply energy to the mine.

Source: Yahoo Finance

Other Players in Greenland’s Mining Landscape

While these three companies are the top players, others are also exploring opportunities in Greenland’s mining sector. Brunswick Exploration Inc., for example, is an early-stage venture focused on lithium and other metals critical for renewable energy. The company recently applied for additional licenses in Greenland following promising discoveries of spodumene, a key lithium-bearing mineral.

Another notable company, Bluejay Mining plc, is advancing its Dundas Ilmenite Project in Greenland. It’s a crucial project for titanium, which is used in various industrial applications. Although recent updates have been limited, Bluejay’s continued efforts show Greenland’s vast mining potential.

So “Greenland is NOT for Sale…”

Credible news and media have reported on Greenland’s Prime Minister, Múte B. Egede’s recent opinion about Greenlanders having no desire to become part of the U.S. Reuters reported that he said in a written comment.

“Greenland is ours. We are not for sale and will never be for sale. We must not lose our long struggle for freedom.”

As said before, Greenlandic and Danish leaders rejected the idea of Greenland becoming a U.S. territory, but the discussion highlighted the island’s rising geopolitical importance amid global power shifts and climate changes.

Despite Trump’s past comments about potentially using force or economic pressure to acquire Greenland, Egede expressed willingness to strengthen cooperation with Washington. He acknowledged why Trump might find the island appealing, given its strategic Arctic location.

Egede further reaffirmed Greenland’s stance at a press conference with Danish Prime Minister Mette Frederiksen in Copenhagen, noting,

“Greenland is for the Greenlandic people. We do not want to be Danish, we do not want to be American. We want to be Greenlandic.”

If we see the brighter side, Greenland’s importance is only growing. The island is becoming an even more attractive destination for mining companies looking to secure valuable resources. With companies like Amaroq Minerals, Critical Metals, and Greenland Resources leading the charge, 2025 is set to be a transformative year for Greenland’s mining sector.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2025-01-15 17:08:122025-01-15 17:08:12From Trump’s Pursual to Mining Boom: Top 3 Greenland Stocks to Watch in 2025

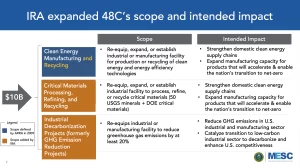

The United States is advancing its clean energy ambitions with the allocation of $6 billion in tax credits under the Inflation Reduction Act’s §48C Qualifying Advanced Energy Project Tax Credit (48C program). Administered by the Department of the Treasury and IRS, the funding will support over 140 projects across more than 30 states.

The focus: boosting clean energy manufacturing, recycling critical materials, and decarbonizing industrial processes. This move underscores the Biden administration’s commitment to building a low-carbon energy future while fostering economic growth in energy-dependent communities.

What is the 48C Program?

The 48C program was initially introduced in 2009 to encourage investments in clean energy infrastructure. Expanded under the Inflation Reduction Act (IRA), it now includes $10 billion in tax credits, with at least 40% reserved for energy communities—regions with economies historically tied to fossil fuels. These communities, often home to closed coal mines or retired power plants, are crucial for the nation’s equitable energy transition.

Since its inception, the program has successfully incentivized over 250 projects. It has unlocked over $44 billion in private investments and created an estimated 30,000 construction jobs.

Clean Energy Manufacturing and Recycling ($3.8 billion)

This allocation supports projects to bolster the domestic production of renewable energy components. Beneficiaries include facilities manufacturing hydrogen electrolyzers, solar photovoltaic systems, wind turbine parts, and EV battery components. These investments help localize clean energy supply chains, reducing dependence on imports and reinforcing energy security.

Critical Materials Processing and Recycling ($1.5 billion)

Critical materials like lithium, copper, and rare earth elements are essential for clean energy technologies. This funding supports refining and recycling these materials, addressing both supply chain vulnerabilities and environmental concerns. For example, projects refining lithium for EV batteries or recycling spent lithium-ion batteries contribute to sustainable resource management.

Industrial Decarbonization ($700 million)

The industrial sector, responsible for nearly a quarter of U.S. greenhouse gas emissions, is a major focus of decarbonization efforts. This funding supports initiatives like installing heat pumps, electric boilers, and other advanced technologies that reduce carbon emissions. Projects in this category aim to eliminate around 2.8 million metric tons of emissions annually, equivalent to taking over 600,000 cars off the road.

Image from the Office of Manufacturing and Energy Supply Chains

Key Impacts of the 48C Program

Strengthening Domestic Supply Chains

The 48C program plays a critical role in addressing vulnerabilities in the U.S. clean energy supply chain. For instance, 80% of global solar panel components are produced in Asia, primarily China. The program incentivizes domestic production to reduce reliance on imports, fostering energy independence and strengthening national security.

Since its inception, the program has been associated with over $2 billion in domestic investments in advanced manufacturing projects, according to Department of Energy estimates.

Supporting Energy Communities

Energy communities, often dependent on fossil fuel industries, face economic hardships as the nation transitions to cleaner energy. The 48C program reserves at least 40% of its $10 billion allocation for these regions, ensuring they reap the benefits of renewable energy growth.

This targeted support has led to infrastructure projects and job creation in historically underserved areas. For example, in 2023, regions like Appalachia and the Gulf Coast witnessed clean energy investments estimated at $1 billion, significantly boosting local economies.

Reducing Carbon Emissions

By supporting decarbonization in heavy industries like steel, cement, and chemicals, the program significantly lowers greenhouse gas emissions. According to EPA estimates, initiatives funded under the 48C program have the potential to reduce carbon dioxide emissions by over 30 million metric tons annually—the equivalent of removing 6.5 million cars from the road each year.

This blend of economic, social, and environmental benefits underlines the 48C program’s pivotal role in steering the U.S. toward a sustainable and equitable energy future.

Ashley Zumwalt-Forbes, Deputy Director for Batteries and Critical Materials at the U.S. Department of Energy (DOE), remarked on the announcement, stating that:

“Particularly noteworthy is the allocation of $1.5 billion towards critical materials recycling, processing, and refining projects – a sector that has outsized importance in our nation’s economic security. “

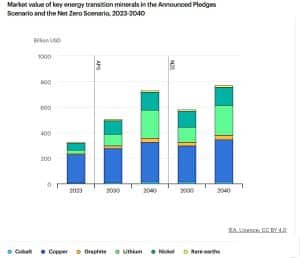

Critical Minerals: Driving the Clean Energy Future

Critical minerals are at the heart of the global energy transition, powering technologies like EVs and renewable energy systems. The International Energy Agency (IEA) reports that demand for these materials surged in 2023, with lithium demand jumping by 30% and nickel, cobalt, and rare earths increasing by 8-15%.

By 2040, the combined market value of critical minerals could exceed $770 billion in the IEA’s Net Zero Scenario.

The United States and its allies are working to reduce dependence on foreign sources, especially China’s dominance over 60-70% of global lithium and cobalt supplies. Measures like the U.S. Defense Production Act aim to strengthen domestic production.

Canada has committed CA$3.8 billion to critical mineral initiatives, though experts emphasize the need to fast-track permitting and expand production.

Moreover, despite slower growth compared to 2022, critical mineral investments increased by 10% in 2023, per the IEA data. Lithium specialists led the surge, with investments rising 60%, even amid weak prices. Exploration spending grew by 15%, driven by Canada and Australia.

Venture capital spending also climbed 30%, with notable growth in battery recycling offsetting reduced funding for mining and refining start-ups. China’s investment in overseas mines hit a record $10 billion in the first half of 2023. The funding focuses on battery metals like lithium, nickel, and cobalt, underscoring its strategic interest in securing critical resources.

From Credits to Clean Energy Transformation

Overall, the clean energy sector requires rapid scaling to meet demand, particularly as the U.S. aims to transition to renewable energy sources. By leveraging the $6 billion allocation from the 48C program, America can position itself as a global leader in clean energy innovation.

By prioritizing domestic production, addressing supply chain vulnerabilities, and supporting energy communities, the 48C program is reducing emissions while laying the groundwork for a sustainable and low-carbon energy future.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2025-01-15 10:28:052025-01-15 10:28:05$6 Billion Tax Credits to Power America’s Clean Energy Future

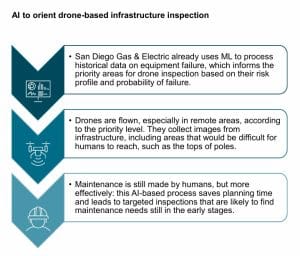

A reality without AI is beyond comprehension! AI is a powerful tool that transforms resource-intensive industries, products, and services by offering data-based suggestions and making smart decisions. As clean tech continues to evolve, the integration of artificial intelligence (AI) will be crucial to driving further advancements.

However, the mix of clean technology and AI brings both exciting opportunities and challenges for shaping a sustainable future.

S&P Global Commodity Insights has revealed a recent study that showcases the immense potential of AI and ML in clean tech. We have discovered some insightful advancements in clean tech, with AI playing a pivotal role.

AI and Microchips: Driving the Clean Tech Revolution

AI and microchips are transforming renewable energy. AI makes processes faster and more efficient, boosting clean energy innovation. Microchips, crucial for AI and data centers, are key to this progress.

In clean energy, these chips enable smarter trading, improve forecasts for wind and solar power, and enhance safety and efficiency.

Machine learning has been used in clean tech for years to monitor wind farms and detect faults. However, applying AI in energy trading was slower. Now, advances in generative AI are changing that. They optimize power markets and improve renewable energy management.

Furthermore, top companies are heavily investing in clean technology, using AI to transform the sector. For instance, Google, Microsoft, and Meta are applying AI in clean energy projects to enhance efficiency and sustainability.

Battery makers like CATL and Tesla are also on board. They use AI to boost battery performance, improve energy storage, and streamline operations. Meanwhile, NVIDIA, the leading chipmaker, is focused on creating advanced AI chips for clean tech.

Together, these companies are revolutionizing technology. They are making renewable energy systems smarter, more efficient, and ready for a sustainable future.

Grid Enhancing Technologies (GETs) play a vital role in optimizing power transmission. These systems help improve the integration of clean energy while reducing the need for costly infrastructure expansions. GETs use a mix of hardware, like sensors and data analytics software to make grids more efficient and adaptable.

So why are they important?

GETs reduce grid congestion by preventing bottlenecks in energy flow.

They help manage peak loads by handling sudden spikes in energy demand.

GETs improve planning by enhancing the accuracy of day-ahead energy forecasts.

They reroute power effectively during outages or maintenance to ensure energy delivery.

How AI Boosts GETs

AI, especially ML is transforming how GETs operate. AI analyzes data in a fraction of time and improves the performance of grid-enhancing technologies.

Real-Time Data

ML uses real-time weather data to adjust transmission line thermal ratings. This improves grid efficiency and capacity to handle more renewable energy without adding new infrastructure. AI also processes different kinds of grid data, like impedance and voltage angles, at high speed. This optimizes power flow, reduces congestion, and boosts efficiency.

Customer Energy Consumption

AI plays a crucial role in understanding customer energy consumption. It accurately predicts energy needs and leverages advanced tools like generative adversarial networks (GANs) to generate synthetic data. These capabilities enhance forecasting accuracy, energy management, and grid reliability.

Supervisory Control and Data Acquisition (SCADA)

Systems like Supervisory Control and Data Acquisition (SCADA) also benefit. AI makes SCADA more accurate and responsive, providing real-time grid performance data that helps operators make better decisions.

As renewable energy grows, smarter grid solutions are essential. In short, GETs, powered by AI, tackle challenges like congestion, peak loads, and clean energy integration.

S&P Global

Supporting Smarter Grid Investments

The rise of renewable energy requires stronger grid infrastructure. AI helps identify weak points in the grid and suggests where investments are most needed. This prevents curtailments and ensures a smoother transition to clean energy systems.

By supporting grid flexibility, AI makes infrastructure investments smarter and more effective. It predicts challenges and optimizes resource allocation, ensuring the grid is ready for the growing share of renewables.

Efficient Wind and Solar Energy Management with AI

Wind energy depends on weather- which is an unpredictable force of nature. So the energy output is also inconsistent. AI solves this problem with weather analyzing tools and historical data for accurate energy forecasts. These forecasts help operators plan better and reduce energy waste.

AI also enhances wind farm operations through predictive maintenance. Sensors collect real-time data to identify potential issues early.

For example, AI detects yaw system misalignments that reduce turbine output or gearbox problems from unusual vibrations.

It eliminates the need for manual pitch inspections by spotting blade alignment issues automatically.

With AI-driven insights, wind farms run efficiently which further minimizes downtime and maximizes energy production. Here’s a snapshot of it.

S&P Global

Solar energy relies on consistent performance, but challenges like shading, dust, and equipment issues can reduce output. Traditional systems often miss early warning signs, as inverters have limited processing capabilities.

AI-based monitoring offers a better solution. By analyzing vast amounts of data quickly, it detects small performance issues that inverters might overlook. This enables real-time adjustments and faster maintenance.

Subsequently, distributed solar systems connecting to low- or medium-voltage grids also benefit from AI. It optimizes energy flow and establishes a uniform distribution of solar power across decentralized networks. By tackling these challenges, AI helps solar systems deliver reliable, clean energy while reducing operational delays.

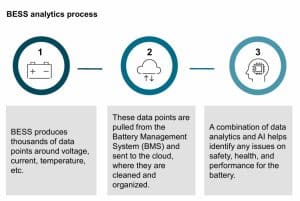

AI’s Role in Battery Management Systems

Measuring the state of charge (SOC) in lithium-iron-phosphate (LFP) battery cells is challenging. These problems and inaccuracies are mostly associated with traditional battery management systems (BMS), that majorly impact battery performance.

But AI provides a better solution to this problem. It uses data analytics and machine learning to spot safety, health, and performance issues. This leads to more accurate SOC predictions. As a result, less downtime is needed for BMS recalibration, thereby maximizing efficiency and revenue.

The process, however, is complex. For instance, AI-based SOC estimation employs the Single Extended Kalman Filter algorithm. This algorithm estimates SOC by calculating the battery’s open-circuit voltage. Machine learning then fine-tunes the Kalman filter for improved accuracy.

S&P Global

Data Complexities in Clean Tech AI

AI offers powerful solutions for clean technology but comes with challenges. Training AI algorithms requires vast amounts of data, which demands advanced data management systems. Therefore, clean tech industries must collect, store, and analyze massive data sets while protecting sensitive information through robust privacy measures.

Similarly, ethical concerns also need much attention. AI systems must prioritize fairness, transparency, and accountability. Clear guidelines are crucial to avoid biases, respect privacy, and ensure clean tech benefits reach all communities equally.

Thus, from this report, we can comprehend how AI is transforming clean energy with smarter tools that improve forecasting, maintenance, and efficiency. As innovations continue to emerge, we can expect AI to crawl more rapidly in clean tech which is driving the future of renewable energy.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2025-01-14 16:52:052025-01-14 16:52:05AI and Clean Tech: A Revolution in Renewable Realms

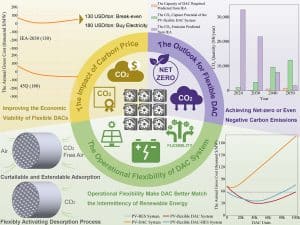

Renewable energy is revolutionizing how businesses address increasing carbon emissions, with solar power leading the charge. As global demand for clean energy rises, innovative technologies like Direct Air Capture (DAC) are emerging as critical tools in tackling carbon emissions.

DAC systems promise a sustainable path toward achieving net-zero emissions, particularly when paired with solar energy. This is what the $415 million funding secured by Origis Energy tackles through its solar project.

Revolutionizing Clean Energy: The Role of Solar in Direct Air Capture

The Swift Air Solar project in Ector County, Texas, developed by Origis Energy, shows the potential of solar energy to fuel innovative solutions. The project represents a significant step in integrating clean energy into decarbonization efforts. It offers the following achievements:

The $415 million project, funded by Natixis Corporate & Investment Banking (CIB) and Advantage Capital, will supply zero-emission solar power to the STRATOS DAC facility in the Permian Basin.

STRATOS, developed by Occidental and its subsidiary 1PointFive, is the world’s first large-scale DAC plant. Expected to capture up to 500,000 tonnes of CO₂ annually, the facility is set to begin operations in mid-2025.

STRATOS will store CO₂ in saline formations, generating carbon removal credits for businesses. 1PointFive has applied for an Underground Injection Control Class VI permit for geologic sequestration, ensuring operations are monitored and verified under an EPA-approved program. This milestone aligns with global goals for sustainable carbon removal and decarbonization.

Construction of Swift Air Solar is already underway, with commercial operations expected to begin by mid-2025. The project will generate clean energy for DAC operations, aligning with Origis Energy’s mission to provide scalable decarbonization solutions. The company’s CEO, Vikas Anand, highlighted this, remarking:

“This is an exciting project, helping to power the world’s first large-scale direct air capture plant. A big thank you to Natixis CIB and Advantage Capital for their partnership.”

The financing for Swift Air Solar includes $290 million in construction and term debt financing and $125 million in tax equity funding. This collaboration highlights the importance of capital, technology, and teamwork in driving renewable energy advancements.

Direct Air Capture technology is designed to remove CO₂ directly from the atmosphere, providing a negative-emission solution for climate goals. However, DAC systems are energy-intensive, and their environmental benefits depend on being powered by renewable energy sources like solar.

The STRATOS facility demonstrates this synergy. By integrating DAC with solar power from Swift Air Solar, the plant will minimize its carbon footprint while maximizing its emission reduction potential.

Additionally, DAC systems are increasingly flexible, allowing them to adapt to the intermittent nature of solar energy. Flexible DAC units can adjust their operations to match solar power output, ensuring efficient energy use and continuous carbon capture.

The Economics of Solar-Powered DAC

Solar power and DAC coupling are both environmentally advantageous and economically promising. Recent research shows that deploying DAC systems with solar power can effectively reduce costs associated with renewable energy curtailment while achieving significant CO₂ capture.

For instance, studies suggest that deploying modular DAC units powered by solar curtailment can achieve the lowest operational costs. These systems can dynamically adjust their processes based on energy availability, making them compatible with fluctuating solar power outputs.

Carbon pricing further enhances the economic viability of solar-powered DAC systems. As carbon prices rise and the costs of DAC components decrease, these systems could provide substantial returns, paving the way for large-scale deployment.

By 2030, PV- or solar-powered flexible DAC systems could meet 15% of global emission reduction goals and help achieve net-zero emissions ahead of 2040. Beyond carbon trading, converting captured carbon into valuable products offers economic benefits, helping offset DAC costs.

Driving Change Through Collaboration and Innovation

The success of the Swift Air Solar project underscores the importance of strategic partnerships in advancing renewable energy. Natixis CIB’s role as the green loan coordinator and Advantage Capital’s investment demonstrates the critical role of financial institutions in fostering innovation.

Nasir Khan, Managing Director at Natixis CIB, emphasized their mission to provide solutions for the energy transition, noting that:

“This financing reinforces our commitment to renewable energy solutions that drive the global energy transition”.

Similarly, Advantage Capital highlighted the transformative impact of their collaboration. The company’s Managing Director Rom Bitting said that this investment aligns with their mission to promote economic growth and environmental impact.

Innovations in the solar industry never stop. Another company that’s pushing America’s renewable energy growth is SolarBank Corporation.

SolarBank: Driving America’s Energy Storage and Solar Energy Growth

SolarBank is a leading solar energy developer, advancing sustainability across North America. Since 2017, it has developed over 250 MW of solar projects in New York and Maryland, focusing on commercial, industrial, and community solar solutions.

Now, SolarBank is part of IESO’s first Long-Term Request for Proposals (E-LT1 RFP and LT1 RFP), targeting 4,000 MW of new dispatchable electricity capacity. The company has also expanded into the electric vehicle charging market, offering innovative solutions to business and residential customers.

With expertise in energy storage, EV charging, and solar energy, SolarBank remains a trusted partner for ESG-driven businesses pursuing Net-Zero goals. Its track record reflects a strong commitment to renewable innovation and growth.

As the global energy landscape evolves, solar power and DAC will play increasingly important roles. Solar’s scalability and cost-effectiveness make it a cornerstone of renewable energy, while DAC provides a viable solution for achieving net-zero emissions. The combination of these technologies offers a pathway to addressing the challenges of climate change.

The Swift Air Solar project exemplifies the transformative power of renewable energy and technology. By coupling solar power with Direct Air Capture, this initiative shows how clean energy can drive innovative solutions to fight climate change.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2025-01-14 15:35:492025-01-14 15:35:49Solar Energy Developer Secures $415 Million to Power the World’s Largest Direct Air Capture Plant

The nickel market experienced downward price pressure in 2024, but 2025 is expected to add more complexities. As demand for critical minerals intensifies and global processing capacity expands, major players in the nickel supply chain will face challenges in predicting prices.

Let’s explore what market research forecasts about the nickel this year.

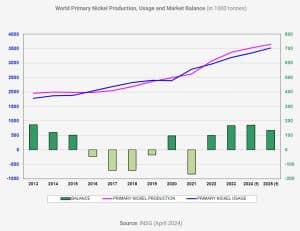

Asia Powers Nickel Growth as Surplus Shrinks

The International Nickel Study Group (INSG) updated its nickel market forecast explaining that the surplus will narrow to 135kt in 2025, with production increasing to 3.649 Mt and demand growing to 3.514Mt.

Narrowing down to Asia, nickel production is set to rise to 3.002Mt in 2025 where Indonesia and China will be the major contributors to growth.

Indonesia: Production will rise from 1.600Mt in 2024 to 1.700Mt in 2025.

China: Output is expected to grow from 1.035Mt in 2024 to 1.085Mt in 2025.

These increases highlight Asia’s dominance in global nickel production, with Indonesia and China continuing to strengthen their positions as key players.

However, 2025 presents an interesting twist! Recently, Bloomberg reported that Indonesia is considering cutting its nickel mine quotas by nearly 40% in 2025. According to Macquarie Group Ltd, the Indonesian government’s proposed restrictions on nickel mining could reduce global supply by more than a third, potentially driving up nickel prices.

These cuts are expected to lower production from 272 million tons in 2024 to just 150 million tons in 2025. Already,Indonesia’s mining limitations have caused supply strains, leading to record nickel ore imports from the Philippines, the world’s second-largest producer, in 2024.

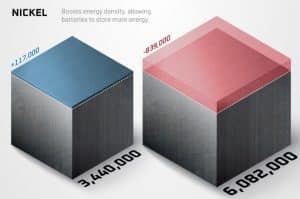

Nickel is essential for battery production, especially in high-energy-density batteries used in electric vehicles (EVs). Yet, the market faces a growing imbalance. A recent Benchmark analysis explained the key trends and risks shaping the future of energy transition materials, focusing on nickel.

It highlights,

By 2034, nickel is expected to face a deficit of 839,000 tonnes—nearly 7X larger than today’s surplus. This shows the urgent need to tackle supply shortages.

The report further explains that approximately $514 billion in investment is required (with $220 billion allocated to upstream projects) to meet global battery demand by 2030.

Of this, nickel alone needs $66 billion—the highest of all critical materials. Without these investments, sustaining the rapidly expanding EV market could become significantly challenging

Benchmark

Challenges in the Nickel Market

Benchmark further explained how the nickel market is grappling with slow project development. While gigafactories and processing plants can start operating within five years, mines often take 5 to 25 years to develop. This mismatch creates a “supply-demand disconnect” that threatens the EV supply chain.

Western nations are also trying to reduce reliance on China, which dominates refining and manufacturing due to lower costs and lenient environmental rules. Shifting production to Western countries, however, increases costs and requires stricter environmental compliance.

Furthermore, the nickel market had its own share of woes in recent years due to oversupply and weak demand. Nasdaq revealed, a brief price surge in early 2024 but it fell sharply by year-end. As 2025 rolled in, nickel traded between $15,000 and $15,200 per metric ton which analysts say to be the lowest since 2020.

Nickel’s role in the energy transition demands immediate investment in mining. Without sufficient raw materials, even the most advanced gigafactories won’t meet EV production goals. Addressing this resource clinch is crucial to stabilizing the supply chain.

Looking ahead, managing price risks, and ensuring steady nickel supplies will remain critical. Stakeholders must navigate these challenges while seizing opportunities in the evolving market for energy transition materials.

Amid the shifting nickel market, Alaska Energy Metals Corporation (AEMC) is leading efforts to boost U.S. nickel independence. Its flagship Nikolai project in Alaska contains valuable resources of nickel, copper, cobalt, and platinum group metals, all crucial for renewable energy and electric vehicles.

UK and Saudi Arabia Forge Critical Minerals Partnership

In the latest developments, Mining.com revealed that Britain will partner with Saudi Arabia to secure critical minerals like copper, lithium, and nickel which are all essential for EVs, AI systems, and clean energy technologies. The agreement aims to strengthen supply chains, attract investment, and create opportunities for British businesses.

Saudi Arabia, valuing its untapped mineral reserves at $2.5 trillion, seeks to position itself as a global hub for mineral trade. For the UK, this partnership supports its industrial strategy focused on economic growth, job creation, and national security.

The deal coincides with ongoing UK-Gulf Cooperation Council (GCC) free trade agreement negotiations. British Industry Minister Sarah Jones will lead a trade mission to the Future Minerals Forum in Riyadh, showcasing UK companies like Cornish Lithium and Beowulf Mining. Jones emphasized the importance of securing mineral supplies to advance AI, clean energy, and technological innovation in a competitive and uncertain global landscape.

As demand for nickel continues to rise, securing the necessary $66 billion in investments will be crucial for meeting the challenges ahead in 2025. However, themarket’s future will depend on addressing supply gaps and adapting to shifting global dynamics.