Carbon Credit Market Heads Toward $270 Billion by 2050 as Quality Reshapes Demand

The global carbon credit market is moving beyond stability and into a phase of structural transformation. While headline numbers suggest a market that has stayed flat in recent years, the underlying dynamics tell a very different story. Quality is now reshaping demand, prices are diverging sharply, and long-term growth signals are strengthening.

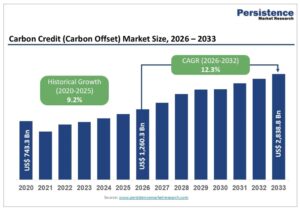

According to market forecasts, the global carbon credit (or carbon offset) market is expected to grow from about $1.26 trillion in 2026 to nearly $2.84 trillion by 2033, expanding at a 12.3% compound annual growth rate. This growth reflects a powerful mix of regulatory pressure, corporate climate commitments, and a steady shift toward high-integrity credits.

However, the real story lies beneath the surface.

Carbon Credit Market Today: Calm on the Surface, Big Shifts Underway

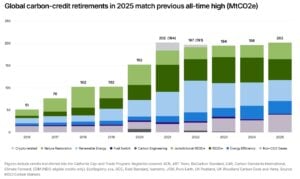

At first glance, the primary carbon credit market appears calm. According to MSCI, in 2025, its value remained steady at just over $1.4 billion, marking the fourth straight year at roughly the same level. Carbon credit retirements also rose modestly, increasing 3% year over year and matching the record highs seen in 2021.

Yet this stability hides major internal shifts.

Rising prices for higher-quality credits helped offset declining demand for lower-quality projects. In other words, the market did not grow in volume, but it evolved in value and composition. This quiet transition is laying the groundwork for stronger expansion in the coming decade.

A Clear Flight Toward Quality

One of the strongest trends shaping the carbon market is the growing divide between high- and low-quality credits.

In 2025, the average global carbon credit price slipped slightly to $3.5 per tonne of CO₂, down from $4.3 the year before. However, this overall decline masks a powerful divergence. Credits rated BBB and above rose sharply in value, climbing from $5.6 to $6.8 per tonne, an increase of more than 20% in just one year.

Meanwhile, lower-rated credits moved in the opposite direction. As a result, the price gap between high- and low-quality credits widened significantly. By the end of 2025, higher-quality credits were trading at a premium of more than 360% compared to lower-quality alternatives.

This growing spread signals a market that increasingly rewards integrity, durability, and verified impact.

Demand Patterns Are Also Shifting

On the demand side, 202 million tonnes of CO₂ equivalent (MtCO₂e) were retired in 2025. Most retirements came from voluntary corporate action, although some credits were transferred into compliance systems such as California’s Cap-and-Trade Program.

After several years of rapid growth up to 2021, total retirements have now stabilized. This trend continued through 2025, suggesting that the market is consolidating rather than contracting.

More importantly, the type of credits being retired is changing. Only about 10% of retired credits were linked to carbon removals, while 90% came from emissions reduction projects. Nearly all removal-based credits came from nature-based solutions, such as forestry and land restoration. This split remained consistent with 2024.

At the same time, demand for renewable energy credits continued to decline. In 2025, they accounted for less than one-quarter of retirements, down sharply from over one-third earlier in the decade. This decline reflects growing concerns about additionality and real-world impact.

Supply Is Expanding—but Selectively

As of the end of 2025, more than 10,200 carbon credit projects were registered across 18 major registries, according to MSCI tracking. These projects issued 294 million credits during the year and more than 2.6 billion credits since the Paris Agreement was signed in 2016.

However, not all supply is valued equally.

Markets are increasingly rewarding project types that demonstrate permanence, measurability, and strong governance. As a result, growth is accelerating in carbon engineering and nature restoration, while traditional renewable energy projects are losing market share.

In fact, despite higher retirement volumes, the market value of renewable energy credits fell by more than 25% year over year. This contrast highlights how price—not volume—is now driving value.

Near-Term Outlook: Slow but Steady Growth

Looking ahead, MSCI modeling suggests that the carbon credit market will begin to expand gradually in the second half of the 2020s, before accelerating more strongly after 2030.

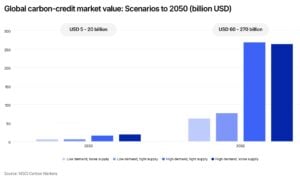

By the end of this decade, the market could be worth between $5 billion and $20 billion, depending on demand strength and supply constraints. While this range is wide, it reflects growing uncertainty around quality, regulation, and buyer preferences rather than weak fundamentals.

Several forces support this outlook. First, corporate climate commitments are growing rapidly. Around 1,300 companies have pledged to reach carbon neutrality by 2030 or earlier. Meanwhile, more than 12,000 companies now have approved or committed Science Based Targets (SBTi)—a nearly 70% increase in just one year.

As these targets approach, companies will need to address residual emissions, creating sustained demand for credible offsets.

Regulation Will Broaden Demand

Beyond corporate buyers, regulation is becoming a major demand driver.

The Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) will enter its second compliance phase in 2027, bringing more consistent demand from airlines. At the same time, companies in regulated markets are increasingly using credits to offset carbon taxes or comply with emissions trading systems.

MSCI estimates that demand from regulated schemes could reach 45 to 180 MtCO₂e by 2030, driven by programs such as California’s Cap-and-Trade and Australia’s Safeguard Mechanism, as well as new national systems.

In parallel, governments are exploring how carbon credits can support Nationally Determined Contributions (NDCs) under the Paris Agreement and future Article 6 mechanisms. This adds another layer of long-term demand stability.

Long-Term Outlook: Big Growth, Big Differences

By 2050, projected market outcomes diverge sharply. Depending on how demand evolves and how tight high-quality supply becomes, the value of retired credits could range from $60 billion to $270 billion.

This wide gap highlights one central theme: credit quality will define the market’s future.

In scenarios where buyers prioritize high-integrity credits, market value grows faster because prices remain strong. In contrast, scenarios flooded with lower-quality supply show weaker confidence, lower prices, and slower growth.

Removal-based credits, especially engineered solutions like direct air capture and biochar, are expected to play a growing role. Although they are more expensive, they align closely with long-term net-zero strategies and offer greater durability.

What This Means for Investors

For investors, the message is clear. The carbon market is becoming larger, more complex, and more selective.

Value is no longer spread evenly across projects. Instead, it is concentrating on high-quality segments that demonstrate strong science, governance, and permanence. Exposure to removal-based solutions and advanced project types is likely to matter more over time.

As the buyer base expands to include corporates, regulated sectors, and sovereigns, carbon credits are shifting from a niche climate tool to a core component of the global transition economy.

In short, the carbon credit market is no longer just growing—it is maturing.

The post Carbon Credit Market Heads Toward $270 Billion by 2050 as Quality Reshapes Demand appeared first on Carbon Credits.