Google Powers U.S. Data Centers with 1.2 GW of Carbon-Free Energy from Clearway

Google has agreed to buy nearly 1.2 gigawatts (GW) of carbon-free energy to power its data centers across the United States. The tech company signed a set of long-term power purchase agreements (PPAs) with Clearway Energy Group (Clearway). These deals will deliver clean electricity from new wind and solar projects in Missouri, Texas, and West Virginia.

The energy will support the electric grid regions where Google’s data centers are located. The agreements are a big step for the tech giant. They help meet its rising electricity needs and cut carbon emissions from its operations.

Amanda Peterson Corio, Global Head of Data Center Energy, Google, stated:

“Strengthening the grid by deploying more reliable and clean energy is crucial for supporting the digital infrastructure that businesses and individuals depend on. Our collaboration with Clearway will help power our data centers and the broader economic growth of communities within SPP, ERCOT, and PJM footprints.”

How Google Secures Carbon-Free Power

A Power Purchase Agreement is a long-term contract between a power buyer and a clean energy producer. In Google’s case, these contracts ensure that the projects Clearway builds will sell electricity to the grid. In return, Google pays for the energy produced over many years.

Clearway agreed to provide Google with 1.17 GW of new carbon-free energy. This energy will support regional grids like SPP, ERCOT, and PJM. The total partnership includes a 71.5 megawatt (MW) clean power deal in West Virginia. This brings the total to around 1.24 gigawatts (GW) of clean energy for Google’s use.

These projects will generate wind and solar power and deliver it into U.S. grid systems that serve Google’s data centers. The total investment in the new energy infrastructure tied to these deals exceeds $2.4 billion.

Construction for the new wind and solar assets is expected to begin soon, with the first facilities planned to start operations in 2027 and 2028.

The states involved are Missouri, Texas, and West Virginia. These states cover parts of major grid regions like SPP (Southwest Power Pool), ERCOT (Electric Reliability Council of Texas), and PJM Interconnection, which deliver power to millions of customers and data centers.

Why Google Is Investing in Clean Power

Google has set clear climate goals tied to its fast-growing energy use. In 2020, the company became the first major corporation to match 100% of its annual electricity use with renewable energy purchases. This means Google buys enough clean power each year to equal all the electricity its operations consume. However, this approach does not guarantee clean energy at every hour.

To address this gap, Google launched a more ambitious target. The company aims to operate on carbon-free energy, 24 hours a day, 7 days a week, by 2030. This goal goes beyond traditional renewable matching. It requires clean electricity to be available every hour in the same regions where Google uses power. This makes energy sourcing more complex and increases the need for new clean generation near data centers.

Google has also committed to reaching net-zero emissions across its operations and value chain by 2030. This includes direct emissions, purchased electricity, and indirect emissions from suppliers and construction.

-

The tech company does not plan to rely heavily on carbon offsets for this goal. Instead, it focuses on cutting emissions at the source, mainly by cleaning up the electricity supply.

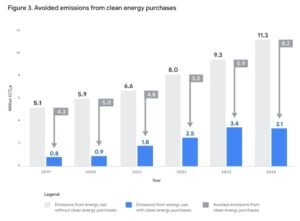

Progress so far shows both gains and challenges. In 2024, Google reported net emissions of about 18 million metric tons of CO₂-equivalent, up from 14.3 million in 2023. The increase came largely from data center expansion and higher electricity demand from artificial intelligence workloads.

At the same time, Google reduced the carbon intensity of its electricity use by about 12% compared with the previous year. This shows efficiency gains, even as total energy use rose.

Clean energy purchases play a key role in this strategy. By signing long-term power purchase agreements, Google helps bring new wind and solar projects online. These projects add clean power to local grids and lower emissions over time.

The nearly 1.2 GW of carbon-free energy announced for U.S. data centers supports this approach. It increases clean supply in regions where Google’s power demand is growing fastest.

Broader Clean Energy Strategy

Google’s clean energy purchasing strategy goes beyond these 1.2 GW agreements. The company continues to enter renewable contracts around the world. For example:

-

Google and TotalEnergies signed a 15-year PPA to supply 1.5 terawatt-hours (TWh) of certified renewable electricity from the Montpelier solar farm in Ohio. This power will help support Google’s data centers in that region.

-

Google is also active in international renewable power agreements. It has signed a 21-year PPA with TotalEnergies. This deal provides 1 TWh of solar power for its data centers in Malaysia.

-

In India, Google made a deal with ReNew Energy. They will build a 150 MW solar project in Rajasthan. This project will generate about 425,000 MWh of clean electricity each year, which is enough to power more than 360,000 homes.

These deals illustrate how Google is diversifying its clean energy supply by securing multiple sources and technologies across continents.

- SEE MORE: Google and NextEra Team Up to Build Gigawatt-Scale AI Data Centers Powered by Clean Energy

- Google’s 3,500-Tonne Carbon Removal Deal with Ebb Signals Growing Confidence in Ocean-Based Climate Solutions

Impact on Data Centers and Regional Grids

Data centers use large amounts of electricity. U.S. data centers’ electricity consumption reached 183 TWh in 2024, accounting for more than 4% of the nation’s total power demand amid surging AI workloads. This marked a continued rise from 176 TWh (4.4%) in 2023. Projections suggest 5% or higher in 2025 as hyperscale facilities expand rapidly.

When powered by fossil fuels, they also produce high carbon emissions. Clean energy purchases help reduce the carbon footprint of these facilities over time.

As data center demand continues to grow, companies like Google are adding new clean power to the grid. Long-term power purchase agreements support the construction of new wind and solar projects. These projects supply clean electricity to regional grids and benefit all users, not only data centers. This helps lower the overall carbon intensity of power systems.

What This Means for Corporate Renewable Leadership

Google’s nearly 1.2 GW clean energy purchase reflects a wider industry shift. Large technology firms are becoming some of the world’s biggest buyers of renewable power. As artificial intelligence and cloud services expand, long-term clean energy contracts help companies secure a stable power supply and manage energy costs.

These corporate agreements also play a key role in the U.S. energy market. Long-term PPAs give developers the financial certainty needed to build new renewable projects. Supported by policy incentives and rising corporate demand, U.S. wind and solar capacity continues to grow. This makes large clean energy portfolios increasingly viable for companies like Google.

The Clearway deal adds to Google’s global portfolio of renewable energy contracts. This portfolio spans multiple regions and energy technologies. By securing large volumes of clean power, Google is strengthening the sustainability of its data centers as digital demand continues to rise.

The post Google Powers U.S. Data Centers with 1.2 GW of Carbon-Free Energy from Clearway appeared first on Carbon Credits.