Cobalt at Crossroads: How Will Oversupply, Price Drops, and LFP Boom Impact Its Future?

According to industry experts, the cobalt market is currently under pressure due to an oversupply and slow demand. The heat is palpable more on cobalt sulfate prices, which are gradually declining, indicating weaker demand. One reason is China’s passenger electric vehicle (PEV) sector, which strongly prefers lithium-iron-phosphate (LFP) batteries that do not rely on cobalt.

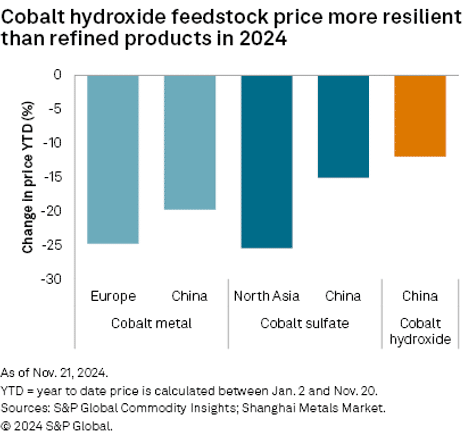

However, as revealed by S&P Global Commodity Insights, the Platts-assessed European cobalt price has held steady at approximately $11.00/lb since October 11, but with suppressed trading activity.

Let’s see what the report reveals further about the current and future cobalt market.

China’s Move to LFP Batteries Weakens Cobalt Market

The report revolved around the cobalt market in China. It highlighted that China’s cobalt metal price stabilized after hitting a low in late September. From September 25 to November 21, the price rose by 5.6% and increased another 2.0% month to November 21, despite some fluctuations.

This recovery was driven by stronger feedstock costs, as cobalt hydroxide prices remained more stable compared to refined cobalt products.

However, according to Shanghai Metals Market, margins for cobalt sulfate production using imported cobalt hydroxide turned negative in Q3 2023. This strained margin significantly impacted China’s cobalt sulfate output.

- From January to October 2023, combined production dropped by 28.1% compared to the same period last year.

The reason for the decline remains the same- a slowdown in the PEV sector. The other significant reason is automakers shifting to lithium-iron-phosphate (LFP) batteries as they are cost-effective and avoid using critical minerals like cobalt and nickel. This transition has reduced the demand for cobalt-containing batteries in China.

Additionally, S&P Global noted, that in October 2024, cobalt-containing batteries accounted for only 20.6% of vehicle installations in China. This figure is a steep drop from nearly 50% in 2021.

Unlocking Cobalt’s Role in Battery Chemistry

Cobalt remains a vital component in many battery chemistries, offering stability and safety benefits. In 2023, demand for cobalt-containing chemistries grew by 15% year-over-year (y/y) to approximately 500 GWh, accounting for 55% of total battery demand.

While this represents a decline from 63% in 2022, cobalt chemistries are expected to maintain a significant market share in the medium to long term as demand continues to grow. Let’s study how experts explain this evolving landscape…

A Shifting Landscape

Cobalt Institute’s latest report revealed that demand for cobalt was mainly driven by high and mid-nickel chemistries driving this growth in 2023. High-nickel chemistries saw a 32% increase, while mid-nickel grew by 15%. Meanwhile, low-nickel and lithium cobalt oxide (LCO) chemistries experienced declines of 11% and 13% y/y, respectively.

It further highlighted,

- Demand for cobalt-containing chemistries rose 15% y/y in 2023, to ~ 500

GWh. This equated to around 55% of battery demand in 2023, down from 63% in 2022.

High-nickel chemistries also increased their market share to 11%, while low-nickel chemistries fell behind nickel-cobalt aluminum oxide (NCA) chemistries for the first time.

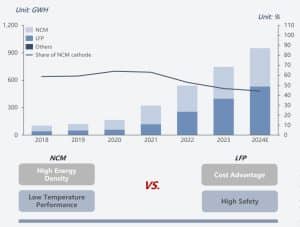

These cobalt-free chemistries now make up 45% of global cathode demand, driven largely by lithium iron phosphate (LFP) batteries. For the first time, LFP overtook nickel cobalt manganese (NCM) cathodes, claiming a 45% market share compared to NCM’s 43%. While manganese-based chemistries also contributed, their impact was minor.

Beyond batteries, cobalt is needed in aviation, energy storage, and electronics and its recyclability makes it sustainable.

Image: LFP vs. NCM: the share of NCM battery cells declines

Source: Cobalt Institute report

Pressures Facing Cobalt

Cobalt, despite its critical role in batteries, faces significant challenges in the supply chain related to cost, composition, and sourcing. Cobalt is costly, but falling prices have improved battery cell cost competitiveness.

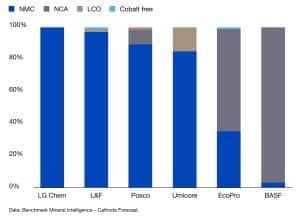

The report highlighted that in 2023, NCM and LFP chemistries dominated the global lithium-ion battery market, making up 88% of cathode demand. Automakers in North America and Europe preferred NCM batteries for their higher energy density and longer range and they were mainly used in high-performance EVs.

On the other hand, LFP batteries have gained market share globally, particularly in China, where their lower cost and reduced reliance on critical minerals like cobalt make them a popular choice. This also means that although NCM chemistries have high energy density they are globally less widely adopted.

Image: 2023 Cathode active materials (CAM) product mix from the major ex. China CAM suppliers, %

Additionally, ethical and environmental concerns regarding cobalt sourcing, particularly from the DRC and Indonesia are extensively scrutinized over its sustainability and responsible extraction practices.

Cobalt Forecast 2024: Price and Production

As cobalt demand continues to face challenges with automakers favoring lithium-iron-phosphate (LFP) batteries, cobalt-containing batteries are considerably losing market share. CMOC expects cobalt-containing batteries to eventually make up less than 10% of the total battery mix.

This declining demand is further reflected in price forecasts as rolled out by S&P Global Commodity Insights noted below:

- Analysts now estimate the cobalt market surplus will widen significantly in 2024, reaching 53,000 metric tons, which is more than 2X of its earlier predictions.

- The growing surplus has also led to a downward revision of cobalt price estimates, with prices now expected to fall to $12.72/lb by 2028.

Batteries now drive three-quarters of global cobalt demand, making the market highly sensitive to changes in cathode chemistries and technologies. As demand for EVs grows, cobalt’s role remains crucial, but the rise of alternatives like LFP will reshape the landscape.

The EV sector’s trajectory in key regions, including the US, China, and the EU, will play a critical role in shaping cobalt’s future. However, with battery technology shifting rapidly and economic policies uncertain, the path ahead remains unpredictable.

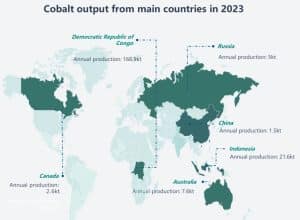

Supply Surge from CMOC, DRC, Australia, and Indonesia

The Democratic Republic of the Congo (DRC), Australia, and Indonesia are the three major countries that control about 73% of the world’s cobalt reserves. Last year, DRC topped the list, accounting for more than 70% of global production.

Source: Cobalt Institute

Source: Cobalt Institute

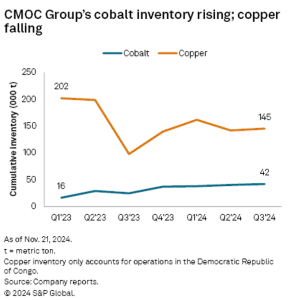

S&P Global forecasts that cobalt production is expected to soar in 2024. It will be significantly driven by Indonesia’s high-pressure acid leaching (HPAL) projects and surge in output from the DRC. Additionally, China’s CMOC, a major producer, has already surpassed its 2023 full-year cobalt production guidance by 21% within the first nine months.

In H1 2024, the company secured the position of the world’s largest cobalt producer with an impressive output of 54,024 tons, marking a staggering 178.22% year-over-year (YoY) growth. This surge not only reflects the company’s pivotal role in the global cobalt supply chain but also signifies a contribution to meet rising demand for battery-grade cobalt.

Notably, CMOC’s production surge is primarily linked to its copper-focused strategy that resulted in increased cobalt inventories.

From this report, we can fairly infer that cobalt can still hold its ground as a key material in high-performance batteries, particularly in Western markets. However, its future will depend on balancing cost, sustainability, and evolving technology trends.

The post Cobalt at Crossroads: How Will Oversupply, Price Drops, and LFP Boom Impact Its Future? appeared first on Carbon Credits.