Trump’s Tariffs and Climate Rollbacks: How 2025 is Shaking Copper Markets and Clean Energy Goals

Donald Trump’s return to the White House in 2025 is already shaking up industries across the globe, particularly those reliant on stable trade and environmental policies. From sweeping tariffs to anticipated rollbacks of key climate initiatives, the impact of these changes could redefine global markets and state-led sustainability efforts.

Among the sectors feeling the weight of this uncertainty are copper markets and renewable energy initiatives.

Copper: A Market Under Pressure

Copper, the backbone of global infrastructure and clean energy transitions, faces unprecedented challenges. Trump’s proposed tariffs, which could range from 10% to 100%, are poised to disrupt the market’s fundamentals.

Targeting major U.S. trading partners, including China, Canada, and Mexico, these tariffs are expected to inflate prices and dampen demand.

David Davidson, an analyst at Paradigm Capital, warns that these trade policies could lead to a tit-for-tat scenario, specifically noting:

“If we get a tit-for-tat trade war, then kiss global economic growth expectation goodbye.”

A strong U.S. dollar and sustained high interest rates, as the Federal Reserve grapples with likely inflation, could further compound these issues by making copper imports prohibitively expensive.

China, which consumes nearly half of the world’s copper, is especially critical in this equation. Economic slowdowns or retaliatory tariffs from China could reverberate across global markets, suppressing demand for the metal.

The country’s faltering property market, which has historically driven copper demand, remains a weak point. Analysts speculate that a substantial stimulus package from China might offset some of these challenges, but its timing and scale remain uncertain.

Tight Supply Chains

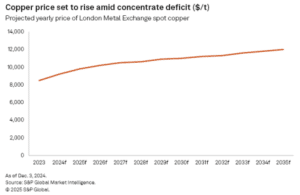

Adding to the turmoil is a looming deficit in copper concentrate supplies. S&P Global Commodity Insights projects a supply shortfall of 540,467 metric tons in 2025. This is exacerbated by delays in reopening First Quantum Minerals’ Cobre Panama mine.

The mine’s closure in 2023 following a dispute with Panama has left the market scrambling for alternatives, and analysts doubt it will resume operations before 2026.

Despite a projected surplus in refined copper, the concentrate deficit could severely impact smelters, particularly in Asia, which rely on steady supplies. Prices will reflect this tension, with the London Metal Exchange forecasting an average copper price of $9,734 per metric ton in 2025.

Last year, there was also a recorded deficit but with an anticipated electric vehicle (EV) boom, where copper is a key component, the demand for this metal will grow. BHP projects a 70% surge in global copper demand, exceeding 50 million tonnes annually by 2050. The traded metal is anticipated to grow at an average annual rate of 2%.

Blue States vs. Trump: The Battle for Climate Progress

While federal climate policy may see significant rollbacks under Trump, blue states (which lean Democratic) are gearing up for a fight. State leaders in progressive regions are determined to protect climate initiatives, even as federal support wanes.

Governors from the U.S. Climate Alliance and America Is All In coalition have pledged to relentlessly advance sustainability efforts.

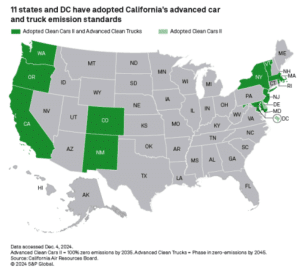

California, a leader in climate action, faces the dual challenge of maintaining its ambitious emissions reduction targets while fending off federal interference.

A key battleground is the state’s waiver to set stricter vehicle emissions standards than those enforced federally. This waiver, which allows other states to adopt California’s rules, is critical to the state’s goal of reducing greenhouse gas emissions 40% below 1990 levels by 2030.

Revoking this waiver, as Trump is widely expected to attempt, could disrupt these efforts and ignite legal battles. Noel Perry, founder of the California think tank Next 10, emphasized the importance of the waiver. Perry noted that:

“California will fight tooth and nail if the Trump administration is going to again attempt to take that waiver away.”

Fiscal Challenges and Climate Goals

Complicating matters further are fiscal challenges in many blue states. California, New York, and Maryland, among others, face significant budget deficits that threaten to undermine their climate initiatives.

California has already reduced its climate-related spending by 21% for the next 8 years, though voters approved a $10 billion climate bond in November 2024 to fund drought mitigation and renewable energy infrastructure.

In New York, a $13.9 billion budget gap between 2025 and 2029 is putting pressure on the state’s ambitious climate goals. The state’s 2019 Climate Leadership and Community Protection Act mandates 70% renewable energy by 2030 and full decarbonization by 2050. However, achieving these targets amid fiscal constraints and uncertain federal policies will be a steep uphill battle.

2025: A Year of High Stakes for Sustainability and Global Markets

Despite the obstacles, blue states are not backing down. Washington Governor Jay Inslee, speaking at the COP29 climate summit, declared that state-led initiatives remain unstoppable. He remarked that Trump won’t be able to stop any of the states from moving forward, citing Washington’s cap-and-invest program and low-carbon fuel standards as examples.

California has allocated $25 million for litigation costs to defend its climate policies. Legal battles could intensify as the Trump administration targets state-level initiatives.

Trump’s trade and climate policies have far-reaching implications. For the copper market, they risk destabilizing supply chains and inflating prices, which could hinder the global clean energy transition.

Meanwhile, his administration’s deregulatory agenda poses challenges to state-led climate progress, even as blue states demonstrate resilience and determination.

With 2025 shaping up as a year of uncertainty, the stakes are higher than ever. Stakeholders, especially industries and governments, must balance economic growth with the urgent need to address climate change. How these competing priorities unfold will define the next chapter in the global effort to achieve sustainability.

The post Trump’s Tariffs and Climate Rollbacks: How 2025 is Shaking Copper Markets and Clean Energy Goals appeared first on Carbon Credits.

Source: Sprott (Bloomberg and TradeTech LLC. Data from 9/30/2014 to 9/30/2024)

Source: Sprott (Bloomberg and TradeTech LLC. Data from 9/30/2014 to 9/30/2024)

Source: National Renewable Energy Laboratory Offshore Wind Market Report

Source: National Renewable Energy Laboratory Offshore Wind Market Report