Europe positions itself as the global driver of the decarbonization agenda. Ambitious targets, regulatory reform and large-scale public funding define the direction. Yet behind the strategy, project pipelines narrow, execution slows down and many initiatives struggle to progress beyond early development. The gap between ambition and delivery continues to widen, making execution-level insight increasingly relevant.

At DECARBON 2026, this perspective takes center stage through insights shared by Marek Drywa, Senior Director Business Development at Worley. His presentation, “Decarbonisation agenda in Europe: market and project observations from the engineering contractor’s perspective,” examines how Europe’s decarbonization efforts perform when viewed from inside active projects.

Drawing on recent European project experience, Worley observes a slowdown since spring 2024 in both the volume and progression of decarbonization projects entering execution. While regulatory frameworks and public funding remain in place, fewer initiatives advance beyond planning into sustained implementation.

At the execution stage, delivery is increasingly shaped by technical complexity, operational constraints and coordination across stakeholders. Engineering timelines, asset readiness and integration challenges now play a more decisive role than strategic intent in determining project outcomes.

Practical perspectives from DECARBON 2026 build on hands-on experience across hydrogen, CCUS, energy storage, pipeline safety and low-carbon fuels. Speakers from LiveEO, SLB, Gasunie and ORLEN reflect on concrete challenges encountered across different segments of the value chain.

Taken together, these contributions highlight recurring structural constraints as well as effective approaches already being applied in practice. The discussion offers a realistic view of what currently supports progress in European decarbonization projects and where delivery continues to stall.

Join the discussion to gain practical insight into Europe’s decarbonization agenda and the realities of turning commitments into executed projects: https://sh.bgs.group/3py

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-02-02 11:14:242026-02-02 11:14:24From Ambition to Execution: How Europe’s Decarbonisation Agenda Performs on the Project Level

According to market researcher Dataforce (via Automotive News), Volkswagen reclaimed the top spot in Europe’s electric vehicle (EV) market in 2025, overtaking Tesla after a sharp rebound in battery-electric vehicle sales. The shift marks a major turning point in the region’s EV race and reflects bigger changes in competition, policy, and the role of carbon credits in the auto industry.

Europe remains one of the world’s most aggressive regions for electrification. Stricter emissions rules, rising fuel costs, and government incentives continue to push buyers toward electric cars. But the latest sales data shows that leadership in the EV market is no longer guaranteed for early pioneers.

Volkswagen’s EV Comeback Was Built on Scale and Choice

Volkswagen sold around 274,000 battery-electric vehicles in Europe in 2025, up 56% from the previous year. Tesla, by contrast, delivered roughly 239,000 units, a 27% decline year over year.

The reversal is striking. In 2024, Tesla outsold Volkswagen by nearly two-to-one. One year later, Volkswagen regained the crown by expanding its lineup and appealing to a wider group of buyers.

Several models drove the surge:

The ID.4 electric SUV sold more than 80,000 units, rising nearly 24%.

The ID.3 hatchback climbed over 44% to almost 79,000 units.

The ID.7 sedan and wagon saw explosive growth of more than 137%, with over 76,000 units sold.

These results show the power of a broad portfolio. Volkswagen offered vehicles across different price points and body styles, from compact hatchbacks to family SUVs and premium sedans. That breadth helped it capture buyers who might not have considered Tesla’s narrower lineup.

Globally, Volkswagen Group said its battery-electric deliveries rose 32% to nearly 983,000 vehicles, even as total vehicle sales dipped slightly. Europe remained its core EV market and a key driver of its decarbonization strategy.

Tesla’s European Slowdown Signals a Competitive Shift

Tesla still led in individual models. The Model Y remained Europe’s best-selling single EV, with more than 151,000 registrations in 2025, although sales dropped sharply from the prior year. The Model 3 ranked among the top sellers but lost ground to new competitors like Skoda’s Elroq.

The company struggled across most major European markets. Germany, once Tesla’s strongest growth engine in Europe, saw registrations fall nearly 48% to around 19,000 units. Other large markets also reported declines, reflecting intense competition and shifting consumer preferences.

Norway was a rare bright spot. Tesla sales rose there as buyers rushed to secure incentives before policy changes expected in 2026.

The broader trend suggests that Tesla’s first-mover advantage is fading in Europe. Legacy automakers are catching up with competitive models, local manufacturing, and strong dealer networks.

Source: Electrek

Europe’s EV Boom Continues Despite Market Shakeups

Jato Dynamics data shows that Europe’s battery-electric vehicle market grew by about 30% in 2025, reaching roughly 2.6 million units sold. That growth came despite economic uncertainty, high interest rates, and uneven government subsidies.

Several factors drove adoption:

Stricter EU emissions rules and fleet-average CO₂ targets

Expanding charging infrastructure across major cities and highways

Lower battery costs and improving vehicle range

A wave of new models across mainstream and premium brands

Analysts say consumers now have more choice than ever. That diversity is accelerating the transition away from internal combustion engines.

Source: Jato

The Global Competition Is Intensifying

Europe is only one battleground. Globally, competition is heating up even faster.

China’s BYD delivered more than 2.2 million battery-electric vehicles in 2025, surpassing Tesla’s roughly 1.6 million units. The Chinese automaker has rapidly expanded its lineup and global footprint, positioning itself as a serious rival in both emerging and developed markets.

In Europe, BYD still trails established brands like Volkswagen, BMW, Hyundai, and Kia. But its rapid growth signals that the global EV market is becoming more fragmented and competitive.

This competition could benefit consumers by lowering prices and accelerating innovation. It could also put pressure on margins across the industry, making carbon credit revenue and government incentives even more important to profitability.

Volkswagen-Tesla Shift Highlights Scale vs. Innovation

For investors, the Volkswagen-Tesla shift highlights two competing EV strategies.

Tesla (TSLA stock) represents innovation-driven growth. It leads in software, autonomous driving, and charging infrastructure. Its carbon credit revenue and energy business provide additional income streams.

Volkswagen represents a scale-driven transition. It has massive manufacturing capacity, strong brand recognition, and deep relationships with European consumers and regulators. Its ability to rapidly expand EV production shows how legacy automakers can pivot when policy and market conditions align.

The broader trend suggests that the EV market will not be winner-takes-all. Instead, it will be shaped by multiple players with different strengths, from Chinese manufacturers to European incumbents and U.S. tech-driven automakers.

Sustainability Strategies Are Becoming a Core Battleground

Volkswagen’s comeback is not just about sales numbers. It reflects a broader sustainability strategy. The company has committed to net-zero emissions across its operations and supply chain, with heavy investments in renewable energy, battery recycling, and low-carbon manufacturing.

The company is expanding battery production in Europe, using renewable electricity at several facilities. It is also working to reduce lifecycle emissions, including raw material sourcing and end-of-life recycling.

Tesla remains a leader in vertical integration, software, and battery efficiency. Its vehicles often have lower lifetime emissions compared to internal combustion cars, especially in regions with clean electricity grids. Tesla also invests in energy storage, solar, and charging infrastructure, reinforcing its clean energy ecosystem.

However, Europe’s focus is shifting toward lifecycle emissions, not just tailpipe emissions. That includes mining, manufacturing, logistics, and recycling. Automakers that can decarbonize their entire value chain may gain a competitive advantage in future regulations and carbon markets.

What This Means for Europe’s Climate Goals

Europe aims to cut transport emissions sharply by 2030 and reach net zero by 2050. Road transport remains one of the largest sources of emissions, making EV adoption critical.

Volkswagen’s surge in EV sales supports these goals by displacing internal combustion vehicles at scale. Tesla’s presence continues to push technology and infrastructure forward. Competition among brands accelerates innovation and lowers costs, thereby increasing adoption.

Carbon markets add another layer of accountability. Automakers that fail to reduce emissions face financial penalties or must buy credits, creating a strong incentive to electrify fleets.

ICCT findings reveal the critical impact of policies adopted in the past 3 years. Road transport emissions in the European Union were projected to peak at nearly 800 million tonnes of CO2 in 2025 and decline thereafter by around one-quarter by 2035. This accelerated decline reflects the impact of the transition from conventional cars to zero-emission vehicles.

Europe Road Emissions

Source: ICCT

Tesla still leads in technology and brand recognition. But Volkswagen’s scale, product range, and regulatory alignment are proving powerful in Europe’s policy-driven environment.

As global competition intensifies and carbon markets evolve, the EV industry will increasingly be shaped by sustainability strategies, regulatory compliance, and lifecycle emissions performance.

Volkswagen’s rise past Tesla in Europe is more than a sales milestone. It is a sign that the clean mobility transition is entering a diverse and competitive phase. Automakers that combine scale, innovation, and carbon strategy will shape the future of transportation—and the future of carbon markets.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-02-02 10:15:052026-02-02 10:15:05Volkswagen Overtakes Tesla in Europe’s EV Market: A Turning Point for Clean Mobility

Apple started fiscal 2026 with a powerful performance. The company reported record revenue, strong earnings growth, and accelerating demand across major regions. At the same time, Apple doubled down on its climate roadmap, highlighting renewable energy use, carbon credits, and ambitious emissions reduction targets. Together, these results show how Apple is balancing profit growth with sustainability leadership.

This analysis breaks down Apple’s Q1 2026 financial performance, regional growth drivers, market reaction, and its climate strategy in simple, easy-to-read language.

In Tim Cook’s words.

“iPhone had its best-ever quarter driven by unprecedented demand, with all-time records across every geographic segment, and Services also achieved an all-time revenue record, up 14 percent from a year ago. We are also excited to announce that our installed base now has more than 2.5 billion active devices, which is a testament to incredible customer satisfaction for the very best products and services in the world.”

Apple’s Q1 2026 Financial Results Show Strong Momentum

Apple reported $143.8 billion in revenue for its fiscal first quarter ended December 27, 2025. That was up 16% year over year, showing strong demand for its products and services.

The company also reported earnings per share (EPS) of $2.84, up 19% from last year. Net income reached $42.1 billion, up from $36.33 billion a year earlier. The board also approved a $0.26 per share dividend, reinforcing its commitment to returning cash to shareholders.

Overall, it beat market expectations on both revenue and profits, signaling strong execution across hardware and services.

Source: Apple

Greater China and India Drive Regional Growth

Apple saw broad growth across regions, but Greater China stood out as the top performer. Revenue from the region surged 38% year over year to $25.5 billion. Record iPhone sales and strong store traffic drove the jump.

Other regions also posted solid gains:

Americas: Revenue grew 11%

Europe: Up 13%

Rest of Asia Pacific: Up 18%

Japan: Up 5%

India was another highlight. Apple achieved quarterly records for iPhone, Mac, iPad, and Services in India. The installed base also grew at a double-digit pace, showing rising brand loyalty and expanding market penetration.

Tim Cook said iPhone demand was strong across all geographies, helping ease earlier concerns about slowing sales in China.

Apple’s stock (AAPL) reacted positively after the earnings release on January 29. Shares rose about 1–2% in after-hours trading, reflecting investor confidence in Apple’s performance.

At the time of reporting, Apple stock traded around $259.48, up slightly during the day. Investors seemed encouraged by strong execution but remained cautious about rising AI-related spending and broader tech market uncertainties.

Source: Yahoo Finance

Apple’s Climate Strategy: A Core Part of Its Business Model

Apple continues to position sustainability as a strategic priority. The company said it supports climate policies and works with policymakers and businesses to align with the Paris Agreement goal of net zero emissions by 2050.

Apple’s long-term goal is to become carbon neutral across its entire global footprint by 2030. The plan focuses on renewable energy, recycled materials, and low-carbon transportation.

It aims to:

Reduce emissions by 75% compared with its 2015 baseline

Address the remaining 25% through high-quality carbon removal projects

Significantly, Apple already achieved carbon neutrality for corporate operations in 2020, making it one of the first major tech firms to reach that milestone.

The company also promotes science-based targets, transparent emissions reporting, and high-quality carbon removal standards. Apple supports strict ESG criteria for carbon credits to ensure real environmental and community benefits.

Renewable Energy and Supplier Decarbonization

Apple reported that renewable energy procured by suppliers avoided about 21.8 million metric tons of greenhouse gas emissions in 2024.

Many semiconductor and display suppliers pledged to cut fluorinated greenhouse gas emissions by at least 90% by 2030. These gases are extremely potent, so reducing them can significantly lower the tech sector’s climate impact.

Apple also supports policies to expand renewable electricity globally, improve grid infrastructure, and invest in energy storage and transmission. The company encourages life cycle emissions assessments and high-integrity mitigation standards.

Use of Carbon Credits and Nature-Based Projects

Apple has used carbon credits to maintain carbon neutrality for its corporate emissions. The company retired credits from multiple certified projects, including: Chyulu Hills project (Kenya), Guinan afforestation project (China), Alto Mayo project (Peru), Cispatá Mangrove project (Colombia), and REDD+ forest conservation project (Guatemala)

These projects follow VCS and CCB standards, which aim to ensure environmental integrity and social benefits. Apple said it regularly updates its life cycle assessment models to improve transparency and accuracy.

Source: Apple

Why Apple’s Financial and Climate Performance Matters

Apple’s strong Q1 2026 results highlight how sustainability and profitability can move together. The company’s revenue growth in China and India shows expanding global demand, while its climate strategy positions it as a leader in corporate decarbonization.

However, Apple’s reliance on carbon credits may attract scrutiny as regulators and investors push for deeper emissions cuts rather than offsets. The tech giant will need to show real reductions across manufacturing, logistics, and product life cycles to maintain credibility.

In conclusion, Apple’s fiscal Q1 2026 marked a powerful start to the year. Revenue and profits surged, driven by strong global demand and regional growth in China and India. Investors responded positively, though cautiously.

At the same time, Apple reinforced its climate ambitions with renewable energy investments, supplier decarbonization efforts, and carbon credit programs. With Apple 2030 approaching, the company faces a critical test: can it continue delivering record financial growth while cutting emissions at scale?

If Apple succeeds, it could set a blueprint for how Big Tech aligns growth with climate leadership in the coming decade.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-02-02 10:15:042026-02-02 10:15:04Can Apple Balance Explosive Q1 2026 Growth with Its Net-Zero Promise?

Visa and Mastercard are two of the largest payment companies in the world. They process trillions of dollars in transactions each year. Their networks connect banks, merchants, and consumers across more than 200 countries.

Full year 2025 earnings show that both companies continue to grow, even as economic conditions remain uncertain. At the same time, investors and regulators are paying closer attention to sustainability and climate commitments. This article compares Visa and Mastercard with their latest earnings data, growth trends, and environmental strategies.

Earnings Show Strong Financial Performance

Earnings Check: Visa’s Momentum Continues

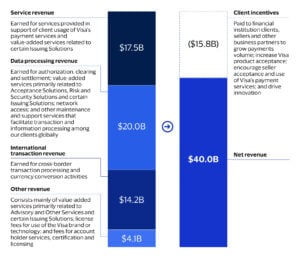

Visa reported strong financial results for its full fiscal year 2025. Net revenue reached $40.0 billion, an 11% increase from 2024. This growth was driven by higher payment volumes, stronger cross-border activity, and more transactions processed on its network.

Visa’s GAAP net income was about $20.06 billion, up from $19.74 billion in the prior year. Diluted earnings per share (EPS) grew to $10.20, compared with $9.73 a year earlier.

Source: Visa

On a non-GAAP basis, net income was roughly $22.54 billion, and non-GAAP diluted EPS reached $11.47, both showing double-digit growth year over year. Total payments volume processed on Visa’s network was 257.5 billion transactions, up 10% from the prior year. Visa’s payment credentials also grew, reaching 4.9 billion by year-end.

Mastercard Delivers: Solid Results and Strategic Shifts

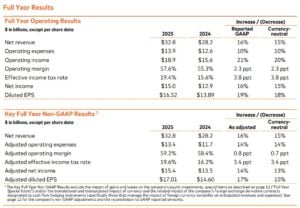

Mastercard also reported strong results for the full year 2025. GAAP net revenue increased to $32.8 billion, up 16% from 2024. On a currency-neutral basis, revenue also grew close to 15%.

The company’s GAAP net income was about $15.0 billion, a 16% increase from the previous year. Mastercard’s diluted EPS rose to $16.52, up from $13.89 in 2024.

Source: Mastercard

On a non-GAAP basis, adjusted net income was $15.4 billion, and adjusted diluted EPS reached $17.01, reflecting 14–17% growth. Transaction activity stayed strong. Gross dollar volume rose by about 9%. Cross-border volume increased by 15%, and switched transactions were up by 10%.

Comparing Growth Drivers and Market Position

Visa and Mastercard share many growth drivers. Both benefit from rising digital payments, increased travel, and global e-commerce expansion. Cross-border transactions are especially important for revenue growth, as they generate higher fees.

Visa reported cross-border growth of about 13%, while Mastercard posted 15% growth in the same area. These figures show that international spending remains a key strength for both companies.

Visa’s larger network gives it higher total revenue. Mastercard, however, often reports higher EPS due to differences in cost structure and share count. Both companies continue to invest in technology, security, and new payment services.

Analysts expect Visa to maintain double-digit revenue growth, while Mastercard is expected to grow at high single-digit to low double-digit rates. These forecasts reflect confidence in long-term payment trends.

Why Emissions Matter for Payment Giants

Financial strength is only one part of the comparison. Sustainability has become a growing focus for payment companies, especially as investors demand clearer climate action.

Breaking Down the Carbon Numbers: 2024 Emissions

Both Visa and Mastercard publish actual greenhouse gas (GHG) emission numbers each year. These figures help show how much carbon each company produces from operations and its value chains.

Visa’s 2024 Emissions

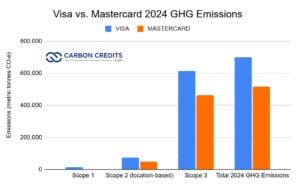

In 2024, Visa shared detailed GHG emissions data. They used the GHG Protocol, which divides emissions into direct and indirect categories. Visa’s sustainability report shows its total operational emissions.

Scope 1 emissions were about 13,510 metric tonnes of CO₂e. For Scope 2, location-based emissions reached 73,448 metric tonnes of CO₂e.

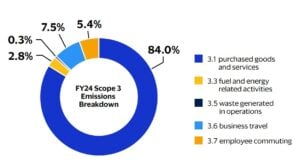

Visa also reported 613,162 metric tonnes of Scope 3 emissions. These are indirect emissions from its value chain. They come from things like purchased goods, services, business travel, and employee commuting. This brings Visa’s total GHG emissions across Scope 1, 2, and 3 to roughly 700,120 metric tonnes of CO₂e in 2024. Scope 3 made up the largest share of these emissions, around 87.6% of the total footprint.

Source: Visa

Visa continues to work toward decoupling its business growth from emissions, even as its operations expand. It measures its footprint each year and includes renewable energy and carbon offsets as part of its strategy to manage impact.

Mastercard’s 2024 Emissions

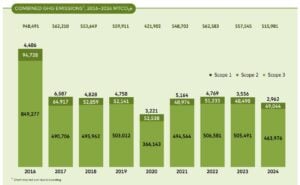

Mastercard also publishes verified GHG data. In 2024, the company’s total Scope 1, 2, and 3 emissions were 515,981 metric tonnes of CO₂e. This represents a 7% drop from 2023 and a 46% cut from the 2016 baseline.

Source: Mastercard

Mastercard’s Scope 1 and Scope 2 emissions made up about 10% of the total. The other 90% came from Scope 3 indirect emissions throughout its value chain. The company has cut emissions in several categories. It is also on track to meet interim targets approved by the Science-Based Targets initiative.

Mastercard’s environmental strategy focuses on cutting operational emissions. It also aims for 100% renewable energy in its offices and data centers. The company also uses tools and programs to help partners and consumers understand and reduce their own emissions.

These emissions figures help illustrate each company’s current footprint and progress. They provide concrete benchmarks as Visa and Mastercard work toward their long-term climate goals.

Data from companies’ 2024 sustainability reports

Visa’s Path to Net Zero

Visa has committed to reaching net-zero emissions by 2040. This target aligns with the Science-Based Targets initiative (SBTi) and a 1.5°C climate pathway.

Visa achieved operational carbon neutrality in 2020. It maintains this status by using 100% renewable electricity across its global offices and data centers. This covers Scope 1 and Scope 2 emissions, as well as parts of Scope 3, such as business travel and employee commuting.

Visa also works to include sustainability in its products. It offers tools that help partners track the carbon footprint of transactions. The company supports initiatives related to greener transport and digital efficiency.

Visa’s approach focuses on reducing its own operational impact while enabling partners and customers to make more informed choices.

Mastercard’s Climate Playbook

Mastercard has also committed to net-zero emissions by 2040. Its target covers the entire value chain, including Scope 1, Scope 2, and Scope 3 emissions.

As of 2024, Mastercard reported a 46% reduction in greenhouse gas emissions from its 2016 baseline. Like Visa, Mastercard uses 100% renewable electricity for its operations.

One of Mastercard’s most visible initiatives is the Priceless Planet Coalition. The program aims to restore 100 million trees by 2025. As of 2024, the coalition had supported the planting of about 26 million trees.

Mastercard also provides tools that help consumers understand the carbon impact of their purchases. The company integrates sustainability standards into its supplier and partner programs.

Side-by-Side: How Their Climate Strategies Compare

Both companies share several similarities in their climate strategies. Each uses renewable electricity and has committed to long-term net-zero targets. Both also work with partners to extend sustainability beyond their own operations.

There are also differences in focus. Visa emphasizes operational neutrality and payment-based tools that support sustainable choices. Mastercard places more emphasis on measurable emissions reductions and large-scale environmental programs, such as reforestation.

Mastercard’s 46% emissions reduction since 2016 provides a clear progress metric. Visa’s early move to carbon neutrality in 2020 shows leadership in operational emissions.

Neither company directly controls most consumer emissions linked to card use. However, both aim to influence behavior through data, tools, and partnerships.

Looking Ahead: Profits, Payments, and Climate Pressure

Visa and Mastercard remain financially strong. Rising digital payments, global travel, and cross-border commerce continue to support earnings growth. Recent results show that both companies are well-positioned for the years ahead.

At the same time, sustainability expectations continue to rise. Regulators, investors, and consumers want clearer climate action from large financial companies. Both Visa and Mastercard have responded with net-zero commitments and measurable steps.

Challenges remain. Most emissions linked to payments sit outside direct operations. Reducing value-chain emissions will require broader collaboration with banks, merchants, and consumers.

Still, both companies have made climate strategy a core part of their long-term plans. Their progress shows how financial performance and sustainability goals are increasingly linked in the global payments industry.

Global investment in clean energy reached a new high of $2.3 trillion in 2025, according to a major industry report. This total was 8% higher than in 2024, showing that investment in low-carbon technologies continued to grow despite economic uncertainty. Researchers say this shows the global interest in cutting greenhouse gas emissions and creating cleaner energy systems.

The clean energy transition includes technologies such as renewable power, electric vehicles (EVs), grid improvements, energy storage, and climate-related tech companies. Together, these areas attracted record funding.

Breakdown of the $2.3 Trillion Investment

The global total of $2.3 trillion in 2025 covered several key clean energy sectors:

Electric transport: The largest category, with $893 billion invested. This includes electric vehicles and charging infrastructure, which are expanding rapidly around the world.

Renewable energy: About $690 billion went into renewable power such as wind, solar, and other clean sources. This was slightly lower than the previous year due to changing regulations in China’s power markets.

Power grids: Investment in grid systems reached $483 billion in 2025. This spending supports the transmission and distribution of clean energy.

Emerging sectors: Hydrogen received $7.3 billion, and nuclear energy received $36 billion.

Although total investment grew, renewable energy funding itself was down nearly 9.5% compared with 2024. This decline was mainly due to new regulatory rules in China, the world’s largest clean energy market.

Overall, clean energy spending has outpaced fossil fuel investment for a second year in a row. Fossil fuel supply investment fell by $9 billion in 2025, mainly due to reduced spending on oil and gas production and fossil power plants.

Regional Power Plays: Who’s Investing Where

Investment levels differ greatly by region. This shows the impact of policy, industry structure, and economic growth.

In the Asia Pacific, investment accounted for nearly 47% of the global total in 2025. China stayed the top market, investing around $800 billion in clean tech. This was despite some drops in its renewable sector.

India saw investment grow by 15%, reaching around $68 billion in 2025. The increase was driven by renewables, grid upgrades, and electrification projects.

The European Union grew its investment by 18% to about $455 billion, making it a major contributor to the global increase.

In the United States, investment increased by 3.5% to about $378 billion. This rise happened even though some federal policies slowed support for certain clean energy programs.

Source: BloombergNEF

These patterns show that all regions invest in clean energy. However, the pace and focus vary based on local strategies and market conditions.

Investment in electric transport, like EVs and charging stations, is now a key player in clean energy spending. In 2025, this area alone attracted $893 billion, making it the top category of global investment.

Electric vehicles are growing fast as battery costs fall and more models become available. Many countries and companies have set targets to phase out fossil fuel vehicles, which boosts demand for EV infrastructure.

Renewable Power and Grids

Even though renewable investment dipped slightly, it still remained a large portion of the total. The $690 billion invested in renewables in 2025 supports new solar, wind, and other clean power plants.

Investment in power grids also grew, reaching $483 billion. Upgrading grids is essential to connect more clean energy to the places that need it. These upgrades include transmission lines, smart grid technologies, and energy storage systems.

Clean Tech Supply Chains and Finance

Investment in factories and supply chains for clean tech also expanded. In 2025, spending on clean energy supply chains reached $127 billion, a 6% increase from 2024. These funds went to battery factories, solar equipment production, and mining for battery metals.

Equity funding in climate-tech companies also rebounded strongly, rising to $77.3 billion — a 53% increase from the previous year. This was the first year of growth in equity funding after several years of decline.

In addition, energy transition debt issuance, loans, and bonds to finance clean energy projects reached $1.2 trillion, up 17% from 2024. This reflects strong interest from both public and private financiers.

Historical Context and Recent Growth

Clean energy investment has been growing steadily over the past decade.

In 2024, global energy transition investment reached about $2.1 trillion, surpassing the $2 trillion mark for the first time. This total was driven by electrified transport, renewable power, and grid investment.

In 2023, investment in clean energy surged to around $1.77 trillion, reflecting rising spending despite geopolitical challenges and market pressures. Electrified transport and renewables both hit new highs that year.

The jump to $2.3 trillion in 2025 continues this long-term growth trend, even though the rate of growth has slowed compared with earlier years. The annual increase dropped from more than 20% several years ago to 8% in 2025 as markets matured and conditions shifted.

Looking Ahead: The Road to $2.9 Trillion

Analysts expect clean energy investment to keep rising in the near term, though uncertainties remain.

BloombergNEF’s base-case scenario shows that global energy transition investment might hit about $2.9 trillion annually over the next five years. This will be above 2025 levels. It shows ongoing interest from both governments and companies.

The International Energy Agency (IEA) offers a broader forecast for total energy investment in 2025. Overall energy investment could reach around $3.3 trillion. This includes spending on both clean and fossil fuels. Clean technologies are expected to get over $2.2 trillion of that total. This would mean clean energy investment continues to outpace fossil fuel spending.

Source: IEA

Experts see these future figures as good signs. However, they say annual investment must grow a lot to reach long-term climate goals, like those in the Paris Agreement. To meet net-zero by 2050, analysts say the world may need to invest over $5 trillion each year by the end of this decade.

What The Record Spend Means for the Energy Transition

The $2.3 trillion clean energy investment in 2025 shows that countries, companies, and investors around the world continue to fund the energy transition. These funds support low-carbon technologies that reduce emissions and improve energy security.

Investment in electric transport helps shift away from fossil fuel vehicles. Renewable energy funding builds new wind and solar capacity. Grid and storage investment enables that power to reach homes, businesses, and industries.

Regional investment patterns show strong gains in the Asia Pacific, Europe, India, and the United States. However, China saw a slight drop in renewable energy funding.

The clean energy transition remains robust, though overall growth rates have slowed compared with earlier years. The trend also shows that climate goals are now a key part of economic and infrastructure strategies. Forecasts indicate a continued expansion of clean energy investment soon. However, meeting long‑term climate targets will need even greater flows of capital across all regions.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-01-30 11:15:002026-01-30 11:15:00Clean Energy Investment Hits Record $2.3T in 2025 Says BloombergNEF: What Leads the Surge?

Microsoft’s Q2 FY26 earnings show a company growing fast while facing new sustainability pressures. Revenue surged on strong AI and cloud demand, carbon removal commitments doubled, and data centers expanded. At the same time, rising water use highlights the environmental costs of AI. Together, the results show how Microsoft is trying to balance financial growth, climate action, and resource management as its AI-driven business scales.

Big Numbers, Bigger Momentum: Microsoft’s Q2 FY26 Performance

Microsoft reported strong results for the second quarter of fiscal 2026, ending December 31, 2025. The company’s total revenue was $81.3 billion, up 17% from the $69.6 billion reported in the same period last year.

Net income, the profit after expenses, was $38.5 billion. This figure rose 60% from about $24.1 billion in the second quarter of fiscal 2025. Microsoft also reported a diluted earnings per share (EPS) of $5.16. This was up 60% from $3.23 per share in the prior year. Operating income also increased by 21% year over year to was $38.3 billion.

The tech giant also reported large growth in its cloud and AI-related businesses. Revenue from Microsoft Cloud reached $51.5 billion in the quarter. This was an increase of 26% compared with the prior year.

Breaking this down:

Intelligent Cloud revenue was $32.9 billion, up 29%.

Productivity and Business Processes revenue was $34.1 billion, up 16%.

More Personal Computing revenue was $14.3 billion, down 3%.

Source: App Economy Insights

The company also reported its remaining performance obligations, future contracted revenue yet to be recognized, at $625 billion. This was up 110% compared with the same time last year.

Microsoft continued to return cash to shareholders. In the quarter, it returned about $12.7 billion through dividends and share buybacks — an increase of about 32% year over year.

These results show that Microsoft continued to grow across major business segments in Q2 FY 2026. Cloud services and AI-related products remained key drivers of revenue growth. At the same time, personal computing revenue, which includes Windows licensing, Surface devices, and search advertising, experienced a small decline.

Despite these robust results, Microsoft’s stock fell about 11% after the earnings. It dropped by $52.95 to close around $428.68 in late trading after hitting a low of $421.11. This is due to investors’ concerns about slow cloud growth and high spending on AI.

Alongside its strong financial performance, Microsoft is also taking major strides in its environmental commitments.

Carbon Removal Leadership: Doubling Impact in 2025

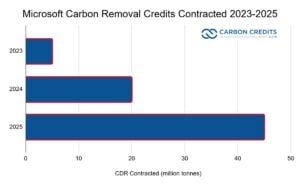

Sustainability remains central to Microsoft’s strategy. In 2025, the company more than doubled its carbon removal agreements to 45 million metric tons of CO₂, up from 22 million tons in 2024.

These purchases include a mix of nature-based solutions. They cover forestry and soil carbon projects, plus direct air capture technologies. The agreements span North America, Europe, and Africa, targeting high-quality, verified removal credits with long-term permanence.

Microsoft’s move reflects a broader trend among tech giants committing to net-zero and carbon-negative strategies. Other big buyers are Amazon, Google, and Stripe. They’re investing in carbon removal to offset emissions that can’t be cut yet.

By securing long-term offtake agreements, Microsoft ensures these projects receive funding to scale operations and deliver measurable climate impact. Analysts predict that global corporate carbon removal purchases might exceed 150 million metric tons each year by 2030. This shows a fast-growing market that mixes corporate sustainability goals with investment chances.

AI’s Hidden Cost: Data Centers and Water Demand

Microsoft also released projections on AI-driven data center water consumption. With AI workloads surging, water use in Microsoft’s global data centers is expected to rise 150% by 2030 compared with current levels. That’s equal to using about 18 billion liters over the said period.

The increase is mainly due to liquid cooling systems used to maintain GPU and CPU performance in AI servers. Water is essential to prevent overheating and maintain efficiency. Microsoft’s water needs are spiking hardest in dry areas.

In Phoenix (hit by 20 years of drought), the company cut its 2030 estimate from 3.3 billion liters to 2 billion by running hotter data centers.

Near Jakarta, Indonesia (a sinking city with drained underground water), the forecast dropped from 1.9 billion to 664 million liters.

In Pune, India (where shortages caused protests and a “No Water, No Vote” push), it fell from 1.9 billion to just 237 million liters—Microsoft wouldn’t say why.

As AI adoption grows, data centers will consume more energy and water, especially in regions with concentrated cloud infrastructure.

In an interview, Priscilla Johnson, Microsoft’s former director of water strategy until 2020, stated:

“Water took a back seat. Energy was more the focus because it was more expensive. Water was too cheap to be prioritized.”

Microsoft is now exploring solutions such as:

Advanced cooling technologies to reduce water intensity per compute unit

Use of recycled water in data centers where feasible

AI-driven energy and resource optimization to manage electricity and water demand

The company emphasizes that AI deployment must be balanced with sustainability practices, ensuring growth does not lead to unsustainable water consumption or carbon emissions.

Microsoft’s Q2 results show that growth and sustainability are connected. Investments in AI, cloud, and enterprise services boost revenue while increasing resource demand. The company’s carbon removal goals and energy-efficient data center plans help reduce environmental impacts.

Key metrics illustrate this balance:

Revenue growth of 9% year-over-year

Cloud revenue of $30.5 billion, up 12%

Carbon removal agreements totaling 45 million metric tons

Projected AI data center water increase of 150% by 2030

These initiatives demonstrate that Microsoft is trying to align profitability with long-term climate goals. Investing in clean technology, energy efficiency, and carbon removal shows that big companies can grow responsibly. This approach also helps reduce environmental impacts.

What Comes Next for AI, Climate, and Capital

Microsoft expects AI adoption to boost demand for:

Data center capacity

Cloud computing

Specialized hardware like GPUs

Analysts predict the global AI data center market could double by 2030, creating both financial and sustainability challenges.

The carbon removal market is also expected to expand. With 45 million tons already contracted, Microsoft’s continued leadership signals corporate influence in scaling carbon removal projects.

Forecasts show that voluntary carbon removal deals might exceed $15 billion each year by 2030. This growth is mainly due to tech companies, industrial firms, and financial institutions.

Water management in data centers is another critical area. Companies need to invest in better cooling and recycled water solutions to help meet rising demand while protecting local water resources. Microsoft’s transparency around water use provides a model for responsible AI deployment globally.

Overall, Microsoft’s earnings report not only reflects strong financial performance but also highlights the company’s sustainability leadership. Growth, carbon removal, and AI infrastructure are linked. They provide insights for companies like Microsoft trying to balance profit with environmental responsibility.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-01-30 10:14:492026-01-30 10:14:49Microsoft Q2 FY26 Earnings: $81B Revenue, AI Momentum, and a 150% Jump in Water Use by 2030

Royal Caribbean Cruises Ltd. (NYSE: RCL) kicked off 2026 with strong financial results for 2025. The company’s success reflects a broader recovery and growth in the global cruise industry. Alongside financial gains, the industry faces growing scrutiny over environmental impact.

Cruise ships are highly carbon-intensive per passenger, prompting major lines—including Royal Caribbean, MSC, Carnival, and Norwegian Cruise Line—to invest in cleaner fuels, energy-efficient technologies, and shore power solutions.

This article looks at the cruise sector’s financial health, passenger growth, and environmental issues. It also discusses how companies are working to balance profits with sustainability.

Smooth Sailing: 2025 Profits and 2026 Outlook

Royal Caribbean Cruises had solid financial results in 2025 and a positive outlook for 2026. The company made nearly $18 billion in revenue in 2025, up from about $16.48 billion in 2024.

Net income also grew to about $4.27 billion, compared with roughly $2.88 billion the year before. Adjusted earnings per share (EPS) rose to $15.64, showing improved profitability.

Source: Royal Caribbean Cruises

The company also generated a strong operating cash flow of about $6.4–6.5 billion and returned around $2 billion to shareholders during the year. Record cruise bookings and higher ticket prices helped drive these results.

Royal Caribbean’s board expects double-digit revenue growth in 2026, along with higher capacity. Adjusted EPS is projected between $17.70 and $18.10. Around two-thirds of 2026 cruise capacity is already booked at strong pricing, supporting this forecast.

Jason Liberty, the company CEO, remarked:

“2025 was an outstanding year, and the momentum is further accelerating into 2026… and we continue to see strong and growing preference for our leading brands and differentiated vacation experiences. We expect another strong year of financial performance with both revenue and earnings growing double digits, and we remain on track to achieve our Perfecta goals by 2027.”

After the earnings call, the company’s stock climbed over 6%, mainly due to strong 2026 guidance.

These results show not only a recovery from pandemic lows but also sustained demand for cruises. Analysts expect this trend to continue as global travel and premium leisure spending grow.

Passenger Waves: Cruise Industry Expansion and Emissions

The global cruise industry is growing fast. Projections show over 38 million passengers by 2026, up from around 37.7 million in 2025. This growth follows strong momentum from 2024 and reflects overall travel trends.

Source: Cruise Lines International Association

Higher demand is encouraging cruise lines to add ships and expand routes. Royal Caribbean, for example, has ordered new Discovery Class vessels and is growing its river cruise segment with more ships planned through 2031. This shows long-term confidence in the market.

Carbon Wake: Cruise Emissions vs Other Travel

Cruising, however, has a higher environmental impact than many other types of travel. Cruise ships are among the most carbon-intensive forms of travel per passenger per distance traveled. This is because they need fuel not just to move but also to run cabins, restaurants, pools, and entertainment.

Even large, efficient cruise ships by Royal Caribbean emit around 250 grams of CO₂ per passenger-kilometer. That is higher than most long-haul flights or hotel stays. Onboard services and hotel-style energy use make cruises even more carbon-heavy.

For perspective:

A five-night cruise of 1,200 miles produces about 1,100 pounds (≈500 kg) of CO₂ per passenger.

A flight covering the same distance plus a hotel stay produces roughly 264 kg of CO₂ per person.

This means a cruise can generate about 2x the greenhouse gas emissions of an equivalent flight-and-hotel trip.

Trains and electric cars have much lower emissions per passenger. For example, traveling by national rail produces about 35 g CO₂ per kilometer, and international trains like Eurostar are even lower at 4.5 g CO₂ per kilometer.

Data source: Voronoi App

Other comparison insights:

Emissions per passenger-kilometer: Large cruise ships emit 0.43–0.65 kg CO₂, depending on occupancy and efficiency. Economy-class flights emit 0.15–0.20 kg, while high-speed rail is around 0.04 kg. Cruises can be 2–10x more carbon-intensive per passenger.

Fuel and technology impact: Using LNG instead of heavy fuel oil reduces CO₂ by 20–25%, but methane slip and upstream emissions can reduce gains. Air lubrication and optimized routing can cut fuel use by 5–10% per voyage.

Ship engines burn huge amounts of fuel. Amenities like air conditioning, theaters, pools, and restaurants add to the energy demand. Cruises remain a luxurious experience, but travelers should know that they usually have a higher carbon footprint than flights, plus hotels or land-based travel. This shows that while cruises are luxurious and convenient, they have a much higher carbon footprint than most other ways of traveling.

Cruise ships also emit sulfur oxides (SOx), nitrogen oxides (NOx), and fine particles, which can harm air quality in port cities and marine ecosystems. Many passengers also fly to and from cruise ports, adding more carbon emissions that are often not included in cruise footprint estimates.

How Cruise Lines Are Addressing Environmental Impact

Cruise companies, including Royal Caribbean, are working to reduce their environmental impact. Many aim to reach net-zero greenhouse gas emissions by 2050 or earlier.

Royal Caribbean’s Destination Net Zero strategy focuses on:

Alternative fuels: LNG-powered ships, biofuels, and fuel cell technology.

New ship technologies: Advanced hulls, air lubrication systems, and shore power connections.

Operational efficiency: Optimized routes and engine improvements to reduce fuel use per passenger.

Source: Royal Caribbean Cruises

Other cruise lines are also taking action to tackle their environmental footprint:

MSC Cruises used efficiency tools and smart itinerary planning to cut 50,000 tonnes of CO₂ in 2024. They are testing hybrid propulsion and shore power at multiple ports. Carnival Corporation is expanding LNG and biofuel use while increasing shore-side electrical connections. They are also researching carbon capture for ships.

Likewise, Norwegian Cruise Line (NCL) is adding LNG-powered ships, battery-assisted propulsion, and energy-efficient onboard systems. NCL is also expanding shore power at ports.

Disney Cruise Line uses hybrid exhaust gas cleaning, advanced wastewater treatment, and fuel-efficient hulls while eliminating single-use plastics onboard. Meanwhile, Princess Cruises applies energy-saving tech, waste reduction, and wastewater treatment, while testing LNG as a fuel alternative.

Overall, the cruise industry faces pressure to reduce carbon intensity. Cleaner fuels, new technologies, and operational efficiency are becoming standard. Environmental responsibility is now a key part of long-term business strategy.

Forecast Horizon: Growth, Finance, and Green Goals

Royal Caribbean and the cruise industry are financially strong. High bookings, growing revenue, and positive forecasts show that demand for cruises is rising. Investments in new ships and offerings aim to meet demand across different traveler groups.

Cruise forecasts show over 38 million passengers by 2026, highlighting ongoing interest. Electric and hybrid propulsion, shore power, biofuels, and fuel-saving technologies are slowly becoming standard.

Challenges remain. Reducing cruise carbon intensity to levels similar to other travel modes will require more alternative fuels, stricter rules, and continued innovation.

Still, many cruise lines have pledged net-zero targets, often aligned with global shipping goals. Passengers are also more aware of environmental impact, driving demand for greener cruises.

Balancing Growth and Emissions

Royal Caribbean’s strong earnings and positive outlook show a resilient and growing industry. Record bookings and strategic investments indicate financial health and long-term growth.

However, carbon emissions remain a major issue. Cruises generally produce more CO₂ per passenger than many other vacations. Cruising is also considered to emit the most emissions compared to other travel methods. Thus, the industry faces pressure to reduce this impact.

Understanding both the financial and environmental sides can help travelers make better choices. For cruise companies and policymakers, balancing growth with emissions reductions is key for the future of cruising.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-01-30 10:14:492026-01-30 10:14:49Royal Caribbean’s (RCL) Record 2025 Profits Meet Carbon Challenges of the Cruise Industry

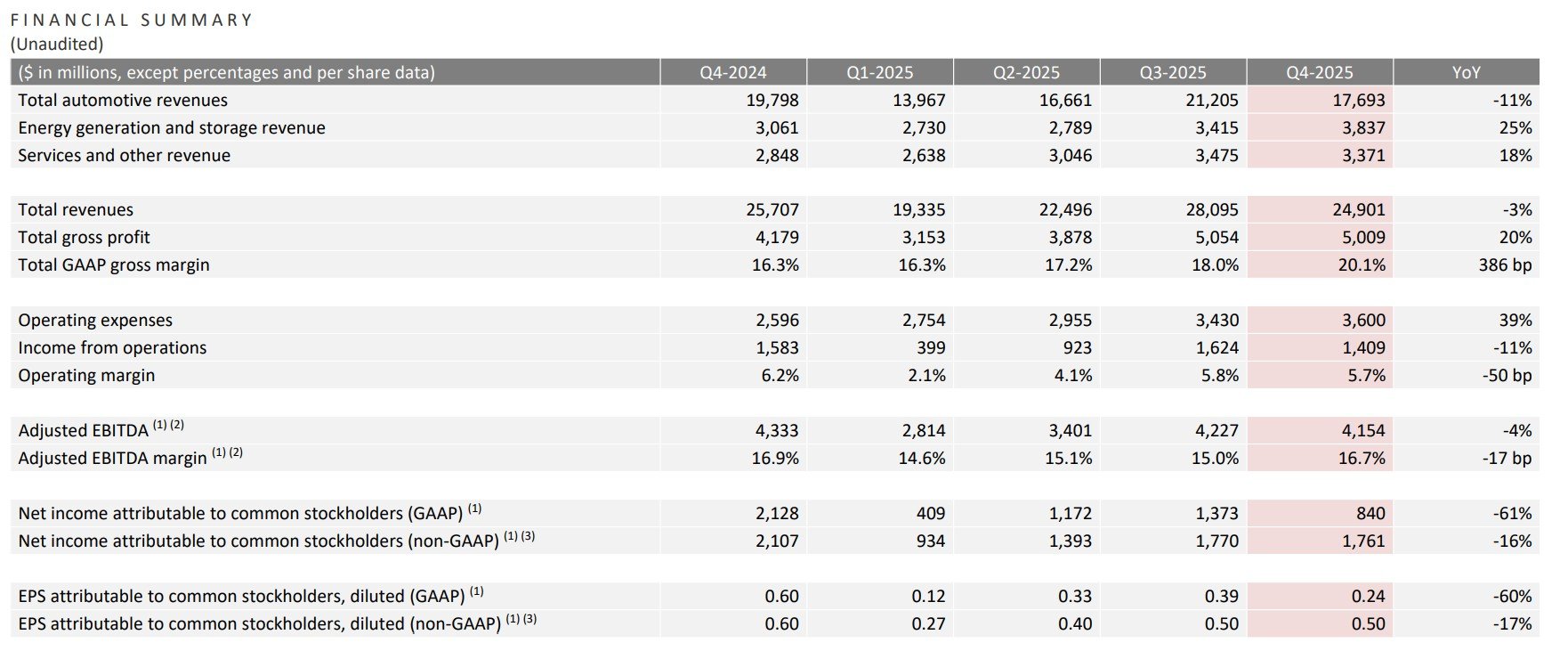

Tesla, Inc. released its fourth-quarter and full-year 2025 earnings on January 28, 2026, showing a mixed financial picture. Revenue exceeded market expectations slightly. However, profits dropped due to weaker vehicle demand and tighter margins.

For the fourth quarter, Tesla reported revenue of about $24.9 billion, a small beat versus analyst forecasts. However, this figure was around 3% lower year over year, reflecting slower growth in global electric vehicle (EV) deliveries. Adjusted earnings per share reached $0.50, down by nearly double digits compared with the same quarter last year.

Source: Tesla

For the full year, Tesla posted total revenue of around $94.8 billion, marking its first annual revenue decline. Sales fell by about 3% year over year, mainly due to price cuts, higher competition, and softer demand in key markets. Net income dropped, and operating margins got tighter. Production costs and pricing pressure hurt the results.

Despite these challenges, Tesla shares moved higher by 3% in after-hours trading. Investors seemed less worried about short-term struggles. Instead, they focused on the company’s long-term strategy, which goes far beyond just vehicle sales.

Strategic Shifts Beyond EVs: Vision for AI, Robotaxis, and Optimus

During the earnings call, Tesla Chief Executive Officer, Elon Musk, highlighted the company’s shift into a technology and energy platform. He noted several initiatives that are expected to shape Tesla’s next phase of growth.

One major focus is autonomous mobility. Tesla continues to prepare for the launch of its Cybercab robotaxi, which the company positions as a future driver of high-margin, recurring revenue. Musk also talked about Optimus, Tesla’s humanoid robot. It’s still in early development, but key to their long-term vision.

Source: Tesla

Musk stated:

“As we increase vehicle autonomy and begin to produce Optimus robots at scale, we are making very big investments. This is going to be a very big CapEx year, as we will get into. That is deliberate because we are making big investments for an epic future. I think all these investments make a lot of sense…But it’s a lot of things. Major investments in batteries and the entire supply chain of batteries. We are also going to be significant manufacturers of solar cells, and we are making massive investments in AI chips.”

Artificial intelligence also featured prominently. Tesla confirmed a $2 billion investment in xAI, Musk’s artificial intelligence venture. The investment reflects the company’s growing emphasis on AI systems that support autonomy, robotics, and advanced software applications.

At the same time, Tesla’s energy generation and storage business remains a key growth area. The company is expanding its battery storage systems. These systems thrive on rising electricity demand, grid instability, and the push for renewable energy. While this segment still represents a smaller share of total revenue, it provides diversification at a time when automotive sales face pressure.

Source: Tesla

These initiatives show Tesla’s plan to rely less on vehicle sales. The EV giant aims to create new revenue streams to support long-term profitability.

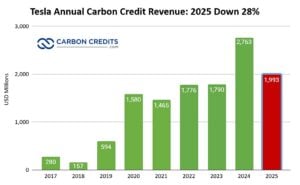

Carbon Credit Revenue: From Record Highs to Slower Growth

In Q1 2025, carbon credit sales fell to $595 million, a 14% decline quarter over quarter. This drop reduced margin support at a time when vehicle pricing pressure remained high.

The decline accelerated in Q2 2025, when Tesla reported $439 million, down 26% from Q1. The weaker credit contribution coincided with continued margin compression in the automotive segment.

In Q3 2025, credit revenue slipped further to $417 million, a 5% sequential decline. This marked the lowest quarterly level of the year. With fewer credits available, Tesla relied more heavily on vehicle sales and cost controls to protect margins.

In Q4 2025, regulatory credit revenue rebounded to $542 million, a 30% increase from Q3. This recovery provided year-end margin support and helped offset weaker automotive profitability. The rebound suggests higher compliance-driven demand late in the year.

Even with the Q4 boost, Tesla’s total regulatory credit revenue for 2025 was still far below 2024, down 28%. That year, Tesla made a record $2.76 billion from credit sales. The 2025 pattern shows lower volumes and greater volatility.

Tesla’s regulatory credits are sold to other automakers that do not meet emissions requirements. These buyers are typically large, global manufacturers such as Stellantis, Toyota, Ford, Mazda, and Subaru.

The EV maker has confirmed its role in carbon credit pooling. This means it shares emissions credits with other automakers. This helps them meet regional rules, especially in Europe. Tesla sells extra zero-emission credits to partner automakers under pooling agreements. In return, they receive payments.

The 2025 data shows that carbon credits are still high-margin and important. However, they no longer provide steady support each quarter. Their effect on operating margin now relies on timing, regulatory cycles, and year-end compliance needs, not steady growth.

A Shifting Financial Landscape: What Earnings Say About Tesla’s Model

Tesla’s latest earnings underline a clear shift in its financial structure. In the past, carbon credit sales helped offset lower vehicle margins and protected profitability. As those credits decline, Tesla must rely more heavily on its core operations and emerging businesses.

The automotive segment continues to face pressure from competition, pricing strategies, and uneven global demand. While Tesla remains one of the world’s largest EV producers, the market has matured, and growth rates have slowed.

At the same time, new business lines such as energy storage, software, autonomy, and AI offer potential upside. Yet, many of these segments require significant investment and may take years to deliver consistent profits.

From a financial perspective, Tesla’s earnings report highlights a transition phase. Short-term results reflect margin compression and revenue contraction. Long-term performance hinges on new technologies. They must scale up and produce a steady cash flow, especially as regulatory credit income decreases.

Driving Sustainability: EVs, Batteries, and Tesla’s Role in Net-Zero

Sustainability is a key part of Tesla’s identity and long‑term plan. The company says its mission is to accelerate the world’s shift to clean energy. It focuses on EVs, energy storage, and renewable integration — all aimed at cutting greenhouse gas emissions.

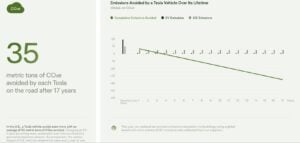

Tesla’s EVs help reduce emissions by replacing internal combustion engine cars. According to Tesla’s 2024 impact figures, customers avoided around 35 million metric tons of CO₂ equivalent in 2024 by using Tesla vehicles, solar products, and energy storage. This was a large jump from prior years.

Source: Tesla

Carbon credits form part of this sustainability ecosystem. By selling credits, Tesla helps other automakers comply with emissions regulations, indirectly supporting lower sector-wide emissions. However, as more manufacturers electrify their fleets, the need for such credits naturally declines.

Battery storage is another part of Tesla’s sustainability work. In 2025, Tesla deployed the highest energy storage, which supports clean energy grids and renewable expansion. Its Powerwall and Megapack units help balance power systems and reduce reliance on fossil fuels.

Tesla has not publicly stated a formal corporate net‑zero target year as some peers do. However, it continues to report on lifecycle emissions, energy efficiency, and avoided emissions in its impact reporting. The company is also working to improve manufacturing, recycling, and supply chain transparency.

As the EV market evolves, Tesla’s role may shift. Carbon credit sales are likely to shrink as more automakers electrify their fleets, and fewer credits are needed. Instead, Tesla’s direct emissions reductions — through cleaner vehicles, grid‑scale storage, AI, and energy products — could become more important in helping global decarbonization.

The global carbon credit market reached a clear turning point in 2025. Volumes declined. Prices rose. Buyer behavior shifted. Policy signals strengthened. At the same time, long-term commitments surged through record-breaking offtake deals.

These changes show a market moving away from scale at any cost. Instead, quality, integrity, and compliance eligibility now shape value. This article reviews the major trends that defined the carbon credit market in 2025 using various industry reports and explains what they mean for 2026 and beyond.

Why 2025 Marked a Turning Point for the Carbon Credit Market

For much of the past decade, growth in the voluntary carbon market was driven by volume. More credits were issued. More were retired. Prices stayed low. Quality concerns often came second.

That model no longer holds.

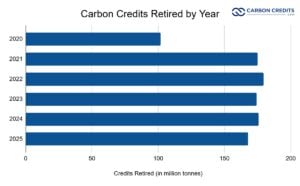

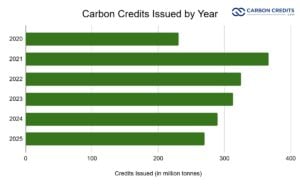

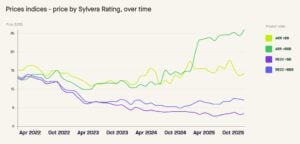

In 2025, total credit retirements fell to about 168 million tonnes, down 4.5% year on year, according to Sylvera report. New issuances also declined, reaching roughly 270 million tonnes, the lowest level since 2020. On the surface, this looks like a contracting market.

Data source: Sylvera

Yet market value moved in the opposite direction. Total spending on carbon credits rose to around $1.04 billion, up from about $980 million in 2024. The average price paid increased to roughly $6.10 per credit.

Source: MSCI Carbon Markets

This shift matters. It shows that market growth is no longer tied to volume alone. Instead, it is driven by higher prices for credits seen as credible, durable, and compliant with future rules.

The reports point to two forces driving this change. First, buyers are paying more for higher-quality credits. Second, compliance-driven demand is starting to reshape the market. Together, these forces signal a transition toward a more structured and selective market.

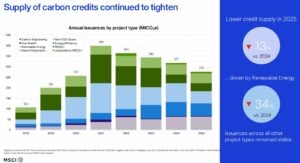

Supply, Demand, Issuances, and Retirements: What Really Changed in 2025

The balance between supply and demand changed in important ways during 2025.

On the supply side, issuances declined across several major project types. Renewable energy credits saw the sharpest drop. These projects have long faced questions around additionality. Many buyers now see them as low impact. As a result, fewer new renewable credits entered the market.

Source: MSCI Carbon Markets

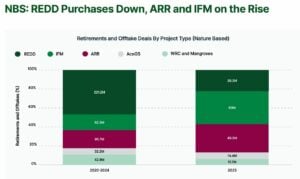

Nature-based credits still dominate total volumes. Forestry and land-use projects remain the largest source of issued and retired credits. However, within this category, the mix is changing.

Buyers are moving away from older REDD+ projects and toward improved forest management, afforestation, reforestation, and agriculture-based projects. Allied Offsets data show the following mix:

Source: Allied Offsets

On the demand side, retirements fell slightly, but this does not signal weakening interest. Corporate demand remained stable in terms of buyer count. What changed was how companies bought credits and what they were willing to pay.

Importantly, compliance use now accounts for about 23% of all retirements. Programs in California, Quebec, South Africa, and Chile contributed to this growth. This share is expected to rise as new compliance systems scale up.

Another key signal comes from inventory data. Credits rated BBB or higher have been in deficit since 2023. In 2025, this deficit continued for a third straight year. At the same time, lower-rated and unrated credits remained heavily oversupplied. Unrated credits alone added an estimated 88 million tonnes to inventory in 2025.

This split highlights a structural imbalance. The market does not lack the credits overall. It lacks the credits that buyers trust.

Nature, Tech, and Removals: The Credit Mix Evolves

The mix of credit types continued to rotate in 2025, reflecting buyer concerns about integrity and future eligibility.

Nature-based credits

Nature-based credits still make up the majority of market activity. However, not all nature credits are treated equally.

Legacy REDD+ projects lost market share. High-profile integrity concerns reduced buyer confidence. Prices weakened for lower-rated REDD+ credits. In contrast, well-rated afforestation and reforestation (ARR) projects gained ground. Buyers showed a clear preference for projects with stronger monitoring, permanence, and land tenure controls.

Agriculture-based credits also expanded. These projects often offer measurable co-benefits for soil health and livelihoods. Buyers increasingly value these attributes.

Technology-based avoidance credits

Credits from renewable energy projects continued to decline. Waste management, landfill gas, and industrial efficiency projects filled some of this gap. These projects often face lower additionality risks and clearer baselines.

Carbon removal credits

Carbon removal credits remain a small share of current retirements. In 2025, durable removals accounted for well under 1 million tonnes of issuances and retirements.

Yet removals are central to the market’s future. This is most visible in the forward market. Most large offtake deals focus on durable carbon removal, such as direct air capture, biochar, BECCS, and enhanced mineralization.

The CDR-focused report highlights why. Net-zero targets increasingly require removals to address residual emissions. Avoidance credits alone are not enough. This structural demand explains why removals command much higher prices and long-term commitments.

Prices, Quality Premiums, and What Buyers Are Paying For

Headline prices only tell part of the story.

In 2025, the average spot price was around $6.10 per credit. But actual prices varied widely by project type, rating, and co-benefits.

Afforestation and reforestation credits traded anywhere from $2 to over $50. Half of the ARR credits fell between $5 and $25. REDD+ credits showed similar dispersion but at lower levels. Quality became the main driver of these differences. For the first time, ratings were clearly embedded in pricing.

ARR projects rated BBB or higher averaged about $26 per credit. Lower-rated ARR projects averaged closer to $14. Unrated projects traded even lower. A similar pattern appeared in REDD+ credits.

Source: Sylvera

Co-benefits added another layer. Projects with strong biodiversity or community outcomes earned clear price premiums. Buyers were willing to pay more for credits that delivered visible social and environmental value beyond carbon.

In the forward market, prices looked very different. Offtake agreements signed in 2025 implied average prices of around $160 per credit. These prices reflect the high costs and limited supply of durable removals, not spot market conditions.

The result is a two-tier market. One tier is a fragmented spot market with wide price ranges. The other is a concentrated forward market built around high-integrity removals.

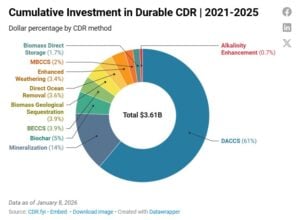

Investments and Movers: Who’s Driving the Market

Private investment in carbon removal companies between 2021 and 2025 reached approximately $3.6 billion, with direct air capture (DAC) attracting the largest share of capital over that period.

Source: CDR.fyi

However, investment activity contracted in 2024 and continued into 2025, even as offtake deals expanded. This highlights a gap between commercial commitments and early‑stage funding scaling.

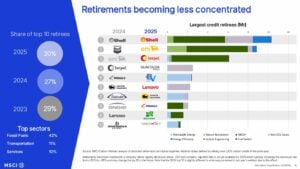

Major Corporate Buyers and Retirees

Corporate engagement shapes much of the 2025 retirement landscape. Several household names emerged as significant purchasers and retirees:

Microsoft remained the single largest buyer of carbon removal credits, accounting for over 90% of removal volume in the first half of 2025.

Energy and utility firms accounted for a sizable portion of total retirements, as indicated in broad market data on retiree sectors.

While comprehensive ranked data for all major buyers in 2025 is not fully disclosed publicly, MSCI analysis of prior data indicates that energy companies, transport firms, and services sectors have historically been among the top retirees when disclosure is available.

Regional retirements also suggest significant corporate participation from Asia, Europe, and North America. This reflects global corporate climate commitments.

Offtake Spotlight: Forward Deals Speak Louder Than Volumes

Offtake agreements were one of the clearest signals of future market direction in 2025.

The total value of offtake deals announced during the year reached about $12.25 billion, up from roughly $4 billion in 2024. This is more than 12 times the value of credits retired in the spot market.

Data source: Sylvera

Yet the volumes involved remain modest. These deals are expected to deliver around 10 million credits per year through 2035. That is less than 10% of current annual retirements.

This gap matters. It shows that buyers are willing to commit large sums to secure limited volumes of high-quality supply. A small group of buyers dominates this space. Microsoft alone accounted for the vast majority of durable removal offtake volume in 2025.

These agreements serve two purposes. They secure future supply in a tight market. They also send strong price signals. If even a fraction of spot market demand shifts toward similar quality thresholds, total market value could grow significantly without higher volumes.

Integrity Meets Policy: Compliance and Ratings Reshape Value

Integrity concerns shaped much of the market’s evolution in 2025.

Buyers are no longer satisfied with claims alone. Ratings, improved methodologies, and third-party assessments now influence decisions. This shift is reinforced by policy.

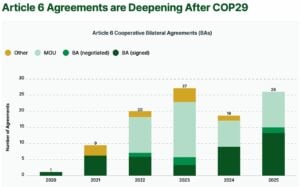

Compliance and voluntary markets are converging. Credits that can meet compliance rules often command higher prices. This is especially true for credits eligible under CORSIA or aligned with ICVCM’s Core Carbon Principles.

In 2025, nearly half of all credits issued came from methodologies potentially eligible for CORSIA. This share continues to rise. At the same time, Article 6 moved from theory to practice. Twenty new bilateral deals were signed in 2025, bringing the total to over 100 agreements.

Source: AlliedOffsets

Moreover, corresponding adjustments emerged as a central issue. Credits with a corresponding adjustment are now clearly differentiated from those without. This distinction affects pricing, eligibility, and long-term demand. Some analysts expect corresponding adjustments to become a tradable element of the market.

Policy signals also strengthened corporate demand. Draft updates to the SBTi Net-Zero Standard clarified how credits can be used alongside emissions reductions. This reduced uncertainty for buyers planning long-term strategies.

The Outlook for 2026 and Beyond

The near-term outlook points to a tighter and more complex market.

In 2026, supply constraints for high-quality credits are likely to persist. New issuances are not rising fast enough to meet demand for BBB+ credits. Prices for trusted nature-based projects are likely to remain firm or increase.

Compliance demand will continue to grow. Modeling suggests compliance use could exceed voluntary demand as early as 2027, driven by CORSIA Phase 1 and expanding domestic systems. By the mid-2030s, domestic compliance markets could become the largest source of demand.

Carbon removal credits will remain scarce in the short term. Actual retirements will lag commitments. However, investment and offtakes signal strong long-term growth. As methodologies mature and costs fall, removals will play a larger role in both voluntary and compliance settings.

The carbon credit market in 2025 did not collapse. It restructured.

For the market as a whole, the direction is clear. Volume alone no longer defines maturity. Quality, integrity, and policy alignment do. Buyers became more selective and prices began to reflect integrity. Policy moved closer to implementation. Offtake deals revealed long-term expectations.

The carbon credit market of 2026 and beyond will likely be smaller in volume than past projections, but higher in value, more regulated, and more closely tied to real climate outcomes.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-01-29 10:15:132026-01-29 10:15:13The Carbon Credit Market in 2025 is A Turning Point: What Comes Next for 2026 and Beyond?