CATL & CHANGAN Make History with World’s First Mass-Production Sodium-Ion Passenger EV

China’s CHANGAN Automobile and battery giant CATL have unveiled the world’s first mass-production passenger vehicle powered by sodium-ion batteries. The launch event took place in Yakeshi, Inner Mongolia, and the vehicle is scheduled to reach the market by mid-2026.

The press release explains that this milestone marks a shift from laboratory research and pilot projects to real-world consumer electric vehicles. It also signals the start of a dual-chemistry battery era, where sodium-ion and lithium-ion technologies work together to meet diverse electric mobility needs.

Why Sodium-Ion Batteries Are Gaining Momentum

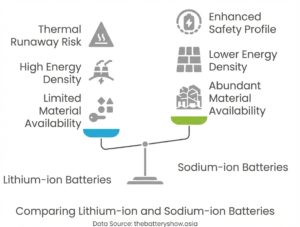

Lithium-ion batteries have dominated electric vehicles for more than a decade. However, concerns over lithium supply, cost volatility, and environmental impacts have pushed researchers to explore alternatives. Sodium-ion batteries emerged as one of the most promising contenders.

Sodium is abundant, widely distributed, and inexpensive. Unlike lithium, it can be extracted from seawater and common salt deposits, reducing geopolitical risks and environmental strain. This makes sodium-ion batteries attractive for countries seeking greater energy independence.

Cold-weather performance is another major advantage. Lithium-ion batteries lose significant capacity in freezing temperatures, which limits EV adoption in colder regions. Sodium-ion batteries, by contrast, maintain strong performance even in extreme cold, opening new markets for electric mobility.

Lithium-ion batteries vs Sodium-ion batteries

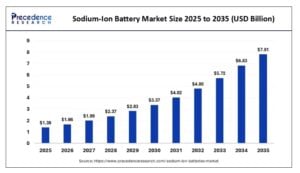

- According to Precedence Research, the global sodium-ion battery market could grow from $1.39 billion in 2025 to $6.83 billion by 2034.

Analysts see 2026 as a turning point, when sodium-ion technology begins large-scale commercialization in vehicles and energy storage.

CATL’s Naxtra Sets New Benchmarks for Sodium-Ion Performance

CATL began sodium-ion research in 2016 and invested nearly RMB 10 billion in the program. The company developed close to 300,000 test cells and assembled a dedicated team of more than 300 R&D engineers, including 20 PhDs.

Research focused on fast-ion transport pathways, composite low-temperature electrolytes, and high-safety electrolyte systems. CATL also leveraged its vast battery management data from millions of deployed units to improve range accuracy and reliability.

This long-term investment highlights how major battery breakthroughs require years of sustained research, testing, and industrial scaling.

Under the partnership, CATL will supply its Naxtra sodium-ion batteries across CHANGAN’s full brand lineup, including AVATR, Deepal, Qiyuan, and UNI. The collaboration positions both companies as early leaders in what could become one of the most disruptive battery technologies of the decade.

Urban and Suburban EVs Made Practical

CATL’s Naxtra sodium-ion battery achieves an energy density of up to 175 Wh/kg, which currently sets a benchmark for mass-produced sodium-ion cells. While this is still lower than leading lithium-ion batteries, it is high enough to support practical passenger vehicles.

Combined with CATL’s Cell-to-Pack (CTP) architecture and intelligent battery management system, the technology enables a pure-electric range exceeding 400 kilometers. As the supply chain matures and chemistry improves, CATL expects future sodium-ion EVs to reach 500–600 kilometers per charge. Range-extended and hybrid configurations could achieve 300–400 kilometers on electric power alone.

These figures cover more than half of the typical daily driving needs in the global new energy vehicle market. For many urban and suburban drivers, sodium-ion vehicles could provide sufficient range at a lower cost.

Cold-Climate Performance Could Transform EV Adoption

One of the biggest barriers to EV adoption is winter performance. Lithium-ion batteries often lose capacity and charging speed in cold conditions, which reduces driving range and convenience.

CATL claims:

- Its sodium-ion battery delivers nearly three times the discharge power of comparable LFP batteries at –30°C.

- Capacity retention remains above 90% at –40°C, and the system continues to provide stable power at –50°C.

This performance could make sodium-ion batteries particularly attractive in regions such as Northern Europe, Canada, Russia, and northern Japan. In these markets, winter range anxiety has slowed EV adoption despite strong policy support.

If sodium-ion batteries deliver on these claims, they could unlock electric mobility in some of the world’s most challenging climates.

Safety Advantages Strengthen Consumer Confidence

Battery safety remains a top concern for automakers and consumers. CATL subjected its Naxtra cells to extreme tests, including crushing, drilling, and sawing. The batteries reportedly showed no smoke, fire, or explosion and continued delivering power even after physical damage.

These results suggest sodium-ion batteries could offer inherent safety advantages over some lithium-ion chemistries. Reduced thermal runaway risk could lower insurance costs, simplify thermal management systems, and improve consumer confidence.

Safety improvements are also critical for regulatory approval and large-scale adoption, especially in densely populated cities.

A Dual-Chemistry Future for Electric Mobility

Both companies emphasized that sodium-ion batteries will not replace lithium-ion batteries. Instead, both chemistries will coexist and complement each other.

Lithium-ion batteries will remain dominant in high-energy applications such as long-range EVs, aviation, and premium vehicles. Sodium-ion batteries are likely to excel in cost-sensitive segments, cold-climate markets, entry-level EVs, and stationary energy storage.

This dual-chemistry ecosystem could accelerate electrification by offering tailored solutions for different use cases. It also diversifies supply chains and reduces reliance on critical minerals.

Choco-Swap Network Could Supercharge Sodium-Ion EV Growth

To support sodium-ion adoption, CATL plans to deploy more than 3,000 Choco-Swap battery swap stations across 140 Chinese cities by 2026. Over 600 of these stations will be located in colder northern regions.

Battery swapping could reduce charging times from hours to minutes, improving convenience for drivers and commercial fleets. It also allows centralized battery management, which can extend battery life and optimize grid integration.

If successful, this infrastructure could give China a major advantage in next-generation EV ecosystems.

Market Outlook: Rapid Growth Across Multiple Sectors

Gao Huan, CTO of CATL’s China E-car Business

“The arrival of sodium-ion technology marks the beginning of a dual-chemistry era.

CHANGAN’s vision shows both its responsibility for energy security and its strategic

foresight. Much as it embraced electric vehicles years ago, CHANGAN is once again

taking the lead with its sodium-ion roadmap. At CATL, we value the opportunity to

work alongside such an industry leader and fully support its strategy, combining our

expertise to bring safe, reliable, and high-performance sodium-ion technology to

market.”

According to data released by SPIR:

- Global sodium-ion battery shipments reached 9 GWh in 2025, representing a 150% year-on-year increase.

- Analysts expect strong growth in energy storage, light-duty vehicles, and passenger EVs starting in 2026.

- By 2030, sodium-ion batteries could reach 580 GWh in energy storage and over 410 GWh in automotive applications. This would be enough to support around 10 million new energy users.

Energy storage is expected to be the largest early market, followed by entry-level EVs and commercial vehicles. Passenger cars are now entering the commercialization phase, signaling broader industry confidence.

Supply Chain Security and Geopolitical Implications

One of the most strategic benefits of sodium-ion batteries is supply chain resilience. Sodium is around 1,000 times more abundant in the Earth’s crust and roughly 60,000 times more abundant in oceans than lithium.

This abundance reduces the risk of supply shortages, price spikes, and geopolitical conflicts associated with lithium, cobalt, and nickel. Countries without lithium resources could still build domestic battery industries using sodium.

For governments, sodium-ion technology offers a pathway to greater energy independence and localized manufacturing.

Environmental and Lifecycle Benefits

Sodium-ion batteries also offer environmental advantages across their lifecycle. Sodium extraction is less water-intensive than lithium brine mining, which has raised concerns in South America’s lithium triangle. Production often uses less hazardous materials, such as iron and carbon-based cathodes.

Research suggests sodium-ion battery production could reduce carbon emissions by up to 60% per kWh compared with some lithium-ion chemistries. Recycling processes may also be simpler and more energy-efficient.

However, sodium-ion batteries currently require more material per kWh due to lower energy density, which could offset some emissions benefits. Continued improvements in chemistry and manufacturing are expected to close this gap.

China’s Strategic First-Mover Advantage

China is taking a lead in next-generation battery technologies by moving sodium-ion batteries from lab research to large-scale commercialization.

Mordor Intelligence report shows that lithium-ion dominated with a 75.5% share in 2025, while sodium-ion is expected to register the fastest CAGR of 18% between 2026 and 2031. Through advanced R&D, robust manufacturing, and supporting infrastructure, Chinese companies are turning experimental technology into market-ready solutions.

The CHANGAN–CATL partnership illustrates this shift. Their sodium-ion passenger car, launching in 2026, marks one of the first instances of mass-produced vehicles powered by this chemistry. The technology promises lower costs, enhanced safety, strong cold-weather performance, and more secure supply chains, making it a practical complement to lithium-ion batteries.

As the dual-chemistry era unfolds, sodium-ion batteries are set to expand the possibilities for electric mobility and energy storage. By combining affordability, reliability, and environmental advantages, they could play a central role in the global transition to clean energy and reshape the future of electric vehicles.

- MUST READ: China Adds Power 8x More Than the US in 2025, with $500B Energy Build-Out in a Single Year

The post CATL & CHANGAN Make History with World’s First Mass-Production Sodium-Ion Passenger EV appeared first on Carbon Credits.