SolarBank Unveils 2024 Milestones: US$67.5 Million and a Bold AI Energy Bet

SolarBank Corporation (Nasdaq: SUUN) (Cboe CA: SUNN) (FSE: GY2) has marked a successful 2024 with major financial transactions, strategic acquisitions, and key project developments. The company continues to expand its role in clean energy, delivering reliable and sustainable power across North America.

SolarBank is an independent renewable energy developer specializing in distributed and community solar projects across Canada and the U.S. The company focuses on solar, battery energy storage, and EV charging solutions, serving utilities, commercial entities, municipalities, and residential customers.

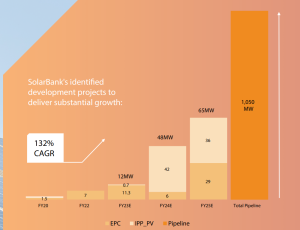

With a pipeline exceeding one gigawatt and over 100 megawatts of completed projects, SolarBank continues to drive the clean energy transition forward. Dr. Richard Lu, CEO of SolarBank, highlighted the company’s achievements last year, stating,

“We experienced another year of tremendous growth and accomplishments in 2024 with a number of significant milestones achieved, including project completions, major acquisitions, execution on the development pipeline, major project sales and senior stock exchange listings. We predict continued forward momentum on these projects and new initiatives, on all of which we will provide ongoing updates as appropriate.”

Big Money Moves: SolarBank Key Financial Transactions and Acquisitions

SolarBank secured over US$ 67.5 million in financial commitments from strategic and financial partners. Among the key deals are:

- $49.5 million transaction with Qcells for the sale and construction of four solar projects in New York. These projects will use U.S.-manufactured Qcells solar modules, aligning with the broader $2.8 billion investment by Qcells in U.S. solar manufacturing.

- $25.8 million project finance facility from the Royal Bank of Canada to fund two battery energy storage projects acquired through Solar Flow-Through Funds Ltd.

- $45 million acquisition of Solar Flow-Through Funds Ltd. (SFF), strengthening SolarBank’s portfolio and expanding its renewable energy footprint.

Corporate Growth and Market Presence

SolarBank has strengthened its corporate presence through stock exchange listings and leadership expansion. The company made a significant leap in market positioning when it began trading on the Nasdaq Global Market on April 8, 2024. It achieves qualification under the second-highest tier of eligibility requirements. This move not only enhances SolarBank’s visibility but also provides greater access to capital markets.

Earlier in the year, on February 14, 2024, SolarBank secured a listing on Cboe Canada, a trading platform that handles over US$ 67 billion in average daily trading volume. This dual listing underscores the company’s growing reputation and financial stability.

In addition to market expansion, SolarBank has reinforced its leadership team. Chelsea L. Nickles, a renewable energy expert with over 20 years of experience, joined the board as an independent director. Her background includes significant contributions to offshore wind projects for Ørsted, a global leader in the sector, positioning her as a valuable asset to SolarBank’s strategic vision.

The Data Center Pivot: Eyeing AI-powered Solutions

In addition to solar energy, SolarBank is venturing into the growing data center sector. The company aims to become a developer, owner, and strategic partner in data center infrastructure, integrating sustainable energy solutions to support artificial intelligence (AI) and high-performance computing.

While no data center projects are under development yet, SolarBank is actively exploring opportunities and plans to provide updates on future agreements.

Key Solar Projects and Developments

SolarBank has made significant progress in expanding its renewable energy portfolio with multiple projects across North America. Notable developments include:

- $41 million transaction with Honeywell International Inc.: SolarBank reached mechanical completion on three community solar projects under an Engineering, Procurement, and Construction (EPC) contract with Honeywell. The company expects to retain operations and maintenance responsibilities post-construction.

- Fiera Real Estate Pilot Project: Construction began on a 1.4 MW rooftop solar project in Alberta for Fiera Real Estate. The company manages over US$7 billion in commercial real estate.

Other major solar projects in the pipeline include:

- Geddes Solar Project (3.7 MW DC) in New York: Expected to provide green energy to 500 homes.

- Greenville, NY Community Solar (14 MW DC total): Expected to serve 1,600 homes.

- Nassau, NY Solar Project (3 MW DC): Designed to supply energy to 350 homes.

- Skaneateles & Lewiston, NY (19.3 MW DC total): Three community solar projects expected to power 2,260 homes.

- Camillus, NY Solar Project (3.15 MW DC): Designed to provide energy to 360 homes.

- Nova Scotia Community Solar Program (31 MW DC total): Projects developed in partnership with TriMac Engineering to supply green energy to 4,000 homes.

Ongoing and Future Projects

SolarBank continues to expand with new developments across multiple locations. Some key upcoming projects include:

- Oak Orchard Project (7 MW DC) in Clay, NY.

- Boyle Project (5.4 MW DC) in Broome County, NY, incorporating agrivoltaics, where solar panels share land with agricultural activities.

- Hwy 28 Project (7 MW DC) in Middletown, NY.

- Silver Springs Project (2.9 MW DC) in Gainesville, NY.

- Three Pennsylvania Community Solar Projects (24.8 MW DC total), pending state legislative approval.

- North Main Project (7.2 MW DC) in Wyoming County, NY.

- West Petpeswick Project (3.1 MW DC) in Nova Scotia.

Future-Proofing Growth: Risks, Rewards, and What’s Next for SolarBank

Despite its strong progress, SolarBank faces several risks that could impact its growth trajectory. The completion of solar projects depends heavily on third-party financing, which may introduce delays or unforeseen construction challenges.

Additionally, regulatory and policy uncertainties could affect the economic feasibility of future developments and solar growth, as government incentives play a crucial role in clean energy investments.

SolarBank’s planned entry into the data center market also comes with risks. While the company sees significant potential in this sector, no agreements have been finalized, and the initiative remains in the exploratory phase. The success of this venture will depend on securing viable partnerships and developing infrastructure that aligns with sustainability goals.

SolarBank’s rapid growth in 2024 highlights its strong position in the renewable energy sector. With successful financial deals, key acquisitions, and a growing project portfolio, the company is well-positioned to capitalize on clean energy demand.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: SUUN.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Please read our Full RISKS and DISCLOSURE here.

The post SolarBank Unveils 2024 Milestones: US$67.5 Million and a Bold AI Energy Bet appeared first on Carbon Credits.