Li-FT Power Strikes Deal with North Arrow Minerals to Expand Lithium Portfolio in Canada’s Northwest Territories

On December 19, Li-FT Power Ltd. (LIFT) announced that it had signed a definitive agreement with North Arrow Minerals Inc. to acquire three lithium projects in Northwest Territories, Canada. In this deal, LIFT will now fully own the DeStaffany, LDG, and Mackay Lithium Projects. In exchange, North Arrow will receive 250,000 common shares of LIFT.

The deal also includes the transfer of reclamation bonds, ensuring responsible environmental practices. However, regulatory approvals are pending for the transaction to close.

Francis MacDonald, CEO and Director of Li-FT Power, commented,

“The acquisition of North Arrow’s lithium portfolio further positions LIFT as the leading lithium exploration company in the Northwest Territories. The DeStaffany Project is located close to our BET and Echo pegmatites which creates synergies from a logistical standpoint, as well as increases the overall resource base for the eastern sector of the Yellowknife Pegmatite Province. The LDG and Mackay properties give LIFT a foothold in an emerging spodumene district located near the Diavik and Ekati diamond mines and provide long-term upside for the Company. We will continue to seek out accretive acquisitions within the Northwest Territories, especially around our existing resource base.”

Li-FT’s Commitment to Lithium Exploration

Li-FT focuses on acquiring and developing lithium projects in Canada, including its flagship Yellowknife Lithium Project, located in the Northwest Territories. In addition to this flagship venture, LIFT owns three early-stage exploration properties in Quebec, which show strong potential for uncovering buried lithium pegmatites.

- READ MORE:

- Li-FT Power Reveals Initial Mineral Resource of 50.4 Million Tonnes at Yellowknife Lithium Project

- Li-FT Power Secures $21 Million Through Strategic Private Placement

The company also manages the Cali Project in the Northwest Territories located within the Little Nahanni Pegmatite Group.

A MESSAGE FROM Li-FT POWER LTD.

This content was reviewed and approved by Li-FT Power Ltd. and is being disseminated on behalf of CarbonCredits.com.

Exploring Hard Rock Lithium Deposits in Canada.

Lithium, one of the most essential ingredients in the production of batteries, lithium powers some of our most important devices. As you may already know, it will also be one of the hottest resources in the coming decade. And one of the fastest-developing North American lithium juniors is Li-FT Power Ltd (TXSV: LIFT | OTCQX: LIFFF | FRA: WS0).

Moving on, let’s deep dive into these 3 lithium projects acquired by LIFT POWER.

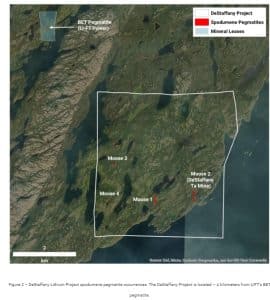

1. The DeStaffany Lithium Project

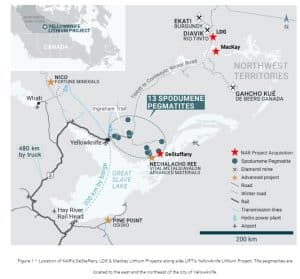

The DeStaffany lithium property spans 1,843 hectares along the north-central shore of Great Slave Lake in the Northwest Territories. It lies just 18 kilometers northeast of the Nechalacho mine and 115 kilometers east of Yellowknife.

The property hosts two significant pegmatites—Moose 1 and Moose 2—rich in lithium, tantalum, and niobium. While these pegmatites were explored in the 1940s for tantalum and niobium, their lithium potential remains largely unexplored. Recent discoveries of additional pegmatites by North Arrow highlight further opportunities on the property.

The Moose pegmatites are located within just 1 kilometer from Great Slave Lake. This property benefits from accessibility via Yellowknife and Hay River throughout the year. LIFT plans to advance the project through mapping, sampling, and prospecting. The next phase will focus on preparing for initial drilling to assess the spodumene pegmatites further.

Moose 1 Pegmatite

The Moose 1 pegmatite stretches 370 meters, with widths ranging from 4.5 to 6 meters and a maximum of 11 meters. Although drilling has never been conducted, historical channel sampling in 2009 revealed spodumene mineralization with lithium levels of 1.5% Li2O over 7.5 meters.

Moose 2 Pegmatite

The mining potential of Moose 2 is promising. It has been mapped over a 450-meter strike length and measures up to 30 meters wide. Bulk sampling in the 1940s and 1950s focused on tantalum and niobium, producing concentrates, but its lithium content remains untapped. Spodumene mineralization is widespread, with lithium grades of up to 1.98% Li2O identified along a 250-meter stretch.

The DeStaffany Lithium Project has been blessed with abundant resources and has a strategic location. These advantages contribute significantly to LIFT’s growing portfolio.

2. The LDG Project

The LDG Project, covering 8,600 hectares is located near Rio Tinto’s Diavik diamond mine. Early exploration has identified ten spodumene pegmatites, with two having outcropping dimensions up to 20 meters wide and 400 meters long. The till-covered terrain offers favorable conditions for discovering buried lithium deposits.

3. The Mackay Project

The Mackay Project, spanning 8,661 hectares, lies south of the Diavik diamond mine. Two spodumene-rich areas have been identified. The MK1 site features pegmatite dykes with lithium grades of up to 3.74% Li2O from grab samples. Meanwhile, the MK3 site includes a 130-meter pegmatite exposure with grades reaching 5.25% Li2O. These findings highlight the high lithium potential of the region.

Experienced Oversight

The lithium miner significantly highlighted that all technical details in this update were reviewed by Dr. Ron Voordouw, a Qualified Person under NI 43-101 standards. This ensures that the information meets absolute professional and regulatory standards.

North Arrow Driving Exploration Success with Global Expertise

Based in Vancouver, BC, North Arrow Minerals is an exploration company primarily focused on advancing the Kraaipan Gold Project in Botswana. It also explores the diamond potential in the Naujaat (NU), Pikoo (SK), and Loki (NWT) projects.

The company’s leadership team, including its management, board of directors, and advisors, brings extensive and proven expertise in global exploration and mining. Kenneth Armstrong, P.Geo. (NWT/NU, ON), serves as North Arrow’s President and CEO, overseeing exploration programs. He is a Qualified Person under NI 43-101 and ensures all projects adhere to industry standards.

He expressed his opinion on this deal as well, noting,

“We are pleased to proceed with this transaction as it provides North Arrow with exposure to the continued evaluation of these NWT lithium properties as well as Li-FT’s advanced Yellowknife Lithium Project while allowing our team to focus on exploration of the Kraaipan Gold Project in Botswana, where geophysical surveys, geochemical baseline analyses, and target evaluation are currently underway.”

With these strategic moves, Li-FT strengthens its position in Canada’s growing lithium market, paving the way for sustainable energy solutions.

- MUST READ: The Lithium Paradox: Price Plummet, Supply Surge, and Demand Dip – What’s Happening Now?

- RELATED: Live Lithium prices

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: LIFT.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

Please read our Full RISKS and DISCLOSURE here.

The post Li-FT Power Strikes Deal with North Arrow Minerals to Expand Lithium Portfolio in Canada’s Northwest Territories appeared first on Carbon Credits.

Source: Walmart

Source: Walmart Source: Walmart

Source: Walmart Source: Walmart

Source: Walmart

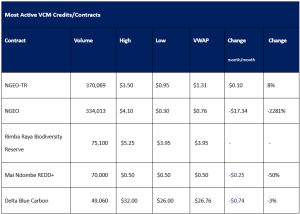

(GEO®) contracts experienced significant price fluctuations in November. The VWAP for block trades under the N-GEO contract dropped from $18.10 in October to just $0.77.

(GEO®) contracts experienced significant price fluctuations in November. The VWAP for block trades under the N-GEO contract dropped from $18.10 in October to just $0.77.

Source: Government of Canada

Source: Government of Canada