Copper Prices Surge Above $13,000: Best Copper Stocks to Watch in 2026

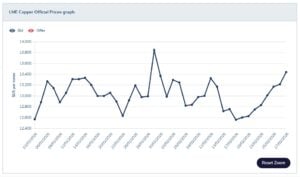

Copper has re-entered the spotlight. Prices on the London Metal Exchange surged to a record $14,527.50 per metric ton on January 29 and continue to hover above $13,000. That rally did not happen by chance. Instead, it reflects a powerful mix of AI-driven demand, tight global supply, and rising geopolitical risk.

Today, copper sits at the center of the electrification and digital revolution. From AI data centers and electric vehicles to renewable power grids and defense systems, the red metal powers it all. As a result, investors, miners, and manufacturers are repositioning for what many now call a structural copper deficit.

AI and Electrification Are Redefining Copper Demand

The global critical minerals market is entering a new phase. According to the International Energy Agency (IEA), the sector could grow two to three times by 2040. That expansion may require between $500 billion and $600 billion in new capital investment.

Electric vehicles need roughly four times more copper than traditional combustion cars. Wind turbines and solar farms require vast cabling networks. Meanwhile, grid upgrades demand heavy copper wiring to handle rising electricity loads.

AI-powered hyperscale data centers consume enormous amounts of copper for power distribution, cooling systems, and grounding infrastructure. A single large AI facility can require up to 50,000 metric tons of copper. That is three to four times more than a conventional data center.

J.P. Morgan estimates that copper demand from data centers alone could reach around 475,000 metric tons in 2026. That represents an annual increase of about 110,000 tons.

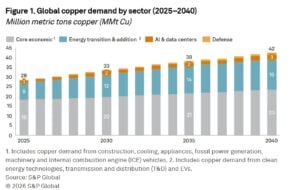

- S&P Global study projects that global copper demand will grow from 28 million metric tons a year in 2025 to 42 million metric tons by 2040 – an increase of 50% above current levels.

Major tech players are already securing supply. In January, Amazon Web Services signed a two-year agreement with Rio Tinto to purchase domestically produced copper from an Arizona mine. The deal marked one of the first direct links between low-carbon copper and AI infrastructure development.

Deficit or Surplus? Analysts Clash Over Copper’s Outlook

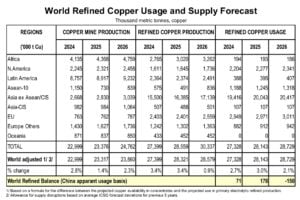

While demand accelerates, supply struggles to keep pace. Analysts now describe copper’s imbalance as structural rather than cyclical. J.P. Morgan projects a refined copper shortfall of roughly 330,000 metric tons in 2026.

Meanwhile, the International Copper Study Group (ICSG) expects the market to shift to a 150,000-ton deficit after previously forecasting a surplus of 209,000 tons.

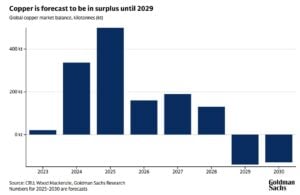

Even Goldman Sachs recently called copper the commodity with the highest growth potential this year, labeling it a “core target of the AI and electrification supercycle.” It projected that the copper market would record a surplus of around 160,000 metric tons this year. As a result, supply and demand are moving closer to balance. Given this outlook, the bank does not expect the global copper market to slip into a sustained shortage anytime soon.

Mining projects face permitting delays, rising capital costs, and operational disruptions. Ore grades are declining at several mature mines. Political tensions in key producing regions have also added uncertainty.

For example, Freeport-McMoRan continues working to restore full operations at its massive Grasberg complex. The company expects production to ramp up in the second quarter of 2026, with about 85% of operations restored by the second half of the year. However, full recovery across all mining zones may not happen until 2027.

Freeport’s new smelter also remains on standby after a previous fire, though management expects concentrate intake to resume later in 2026. These challenges illustrate a broader trend: supply is not flexible enough to respond quickly to demand shocks.

US Inventories Surge, But Global Tightness Persists

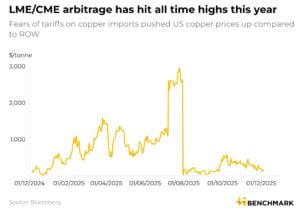

Interestingly, the United States experienced a sharp rise in refined copper imports during 2025.

As per the latest reports, after the White House postponed its decision on tariffs, the price gap between U.S. copper traded on the CME and copper traded on the LME quickly narrowed. As a result, the trading opportunity disappeared for a short time. However, copper imports into the U.S. soon picked up again.

In December alone, nearly 200,000 metric tons entered the U.S. market. According to the World Bureau of Metal Statistics (WBMS), total U.S. refined copper imports reached 1.4 million tons in 2025. That marked a year-on-year increase of 730,000 tons.

Similarly, according to Benchmark, earlier in 2025, the price gap between U.S. and global copper prices rose to nearly $3,000 per ton. That large difference pulled huge volumes of copper into the country.

It estimates that more than 730 kt of copper is effectively “trapped” in the U.S. This surge created a sizeable inventory build inside the country.

Yet, global supply remains tight. Much of the imported metal reflects precautionary stockpiling and strategic positioning rather than structural oversupply. Outside North America, deficits still loom large.

Therefore, while U.S. warehouses appear full, the broader market remains stretched.

Best Copper Stocks to Watch as the Deficit Deepens

With prices elevated and deficits emerging, mining companies are scaling up investments. Selective producers with strong balance sheets and operations in stable jurisdictions may benefit most if copper prices reaccelerate. In this global outlook, Canadian and allied-country producers enjoy added appeal.

For instance:

Teck Resources

The miner reiterated 2026 production guidance of between 455,000 and 530,000 tonnes. The company continues ramping up the Quebrada Blanca Phase 2 project in Chile, with peak capital spending nearing $2 billion. A proposed merger with Anglo American could create one of the world’s top five copper producers.

Hudbay Minerals

It reported record revenue and EBITDA in 2025. The company doubled its quarterly dividend and increased 2026 capital spending to support both sustaining operations and growth initiatives, including the Copper World project in Arizona.

Lundin Mining

Similarly, Lundin Mining delivered record revenue of $4.1 billion in 2025. Copper production reached over 331,000 tonnes at competitive cash costs. The company expects output to remain stable in 2026, while continuing to advance development projects across its portfolio.

Developers also see opportunity. Capstone Copper projects 2026 production between 200,000 and 230,000 tonnes. It plans significant sustaining and exploration investments to strengthen long-term growth. In addition, North American manufacturers are expanding. Revere Copper Products secured a $207.5 million credit facility in January to fund capacity expansion tied to electrification and data center demand.

So it’s clearly the industry is preparing for sustained strength.

Can Prices Stay Above $13,000?

The key question now is sustainability. A Reuters poll of 31 analysts published January 29 placed the median 2026 copper price forecast at $11,975 per ton. That figure sits well below recent peaks, yet it represents the highest consensus forecast ever recorded.

In other words, even cautious analysts expect historically strong pricing.

In conclusion, copper’s surge above $14,000 per ton signals more than a short-term rally. It reflects a big structural change. AI data centers, electrification, and energy transition projects are rewriting demand projections. At the same time, supply growth struggles under operational, political, and financial constraints.

Although price volatility will likely persist, the broader setup remains supportive. Producers with low costs, strong balance sheets, and exposure to stable jurisdictions may offer strategic advantages in this new cycle.

In many ways, copper has become the backbone of the AI and clean energy economy. And if current trends continue, the red metal’s supercycle may only be getting started.

READ MORE:

- Rio Tinto’s FY25 Profit Falls 14%, but Copper Projects and Sustainability Efforts Stand Out

- Copper Drives BHP’s $6.2B Profit Surge in FY26 Half-Year Results

The post Copper Prices Surge Above $13,000: Best Copper Stocks to Watch in 2026 appeared first on Carbon Credits.