Demand for battery-grade nickel is projected to grow significantly by the end of the decade due to rising electric vehicle (EV) adoption. However, the nickel market faced more volatility and uncertainty in November 2024, according to S&P Commodity Insights data. It is largely due to macroeconomic and political developments following Donald Trump’s U.S. presidential election victory.

Trump’s Victory Fuels Nickel Market Volatility

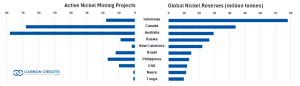

Nickel is vital for producing stainless steel and alloys used in equipment, transport, buildings, and power generation. Major nickel producers include Indonesia, the Philippines, Russia, and Australia, with Indonesia having the highest nickel reserves while Australia has the most active mining projects.

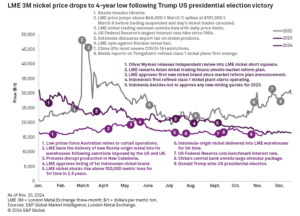

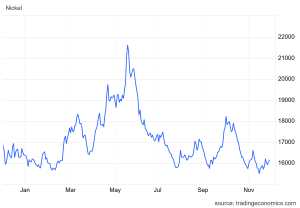

Nickel futures are traded on the London Metal Exchange (LME), reflecting its global industrial importance. The LME three-month nickel price dropped to a four-year low of $15,540 per metric ton on November 15.

Concerns over Trump’s potential economic policies, particularly their implications for China, the industrial metals’ top consumer, have fueled investor caution. A stronger U.S. dollar and increased LME nickel inventories further worsen the downward pressure on prices as shown above. This highlights a risk-off sentiment across metals markets.

Nickel prices initially saw an uptick after Trump’s election win, rising from $16,007 per metric ton on November 4 to $16,587 per metric ton on November 7.

This temporary boost mirrored gains in U.S. equity markets. However, optimism quickly faded as the trade-weighted U.S. dollar index climbed to a one-year high, fueled by market expectations that Trump’s policies—such as higher tariffs on Chinese imports—could revive U.S. inflation.

The prospect of prolonged high interest rates from the Federal Reserve further strengthened the dollar. This makes nickel and other commodities more expensive for non-dollar investors.

Investor sentiment in the nickel market took another hit following China’s unveiling of a 10 trillion yuan fiscal stimulus package on November 8. The measures failed to meet market expectations for more aggressive economic support. This disappointment, coupled with rising nickel inventories and a nearly 4x increase in net short positions on LME nickel, accelerated the price decline.

By mid-November, the LME three-month nickel price had plunged to levels not seen since November 2020, underscoring the market’s vulnerability to both economic and geopolitical developments.

In late November, nickel rebounded to $16,040 per tonne amid Indonesia’s tighter mining policies. Approved quotas could drop 27% by 2026, while license fees for low-grade ore may be reduced.

According to the Indonesian mining minister, nickel ore imports surged 50-fold, as officials prioritized domestic reserves and warned of dwindling stocks to stabilize prices.

IRA Under Threat: What Trump’s Plans Mean for Nickel and EVs

The implications of Trump’s election for the U.S. Inflation Reduction Act (IRA) add another layer of uncertainty to the global nickel market.

Signed into law by President Joe Biden in 2022, the IRA has been a key driver of clean energy initiatives. This includes a $7,500 consumer tax credit for electric vehicles.

However, Trump’s transition team is reportedly considering repealing this tax credit as part of broader tax reform efforts. Such a move could slow the adoption of EVs in the U.S. This could undermine a major driver of global primary nickel demand over the next five years.

Additionally, Trump’s administration may tighten the IRA’s foreign entity of concern (FEOC) guidelines, which currently disqualify companies with significant Chinese ownership from benefiting from the EV tax credit. For instance, Indonesia—a leading producer of nickel—has been working to reduce China’s influence to qualify for IRA incentives.

In a recent deal between PT Vale Indonesia and China’s GEM Co., GEM’s stake in a $1.42 billion nickel plant was capped at 25% to comply with the guidelines. However, stricter FEOC rules could make it even harder for such projects to qualify for U.S. tax incentives. This can potentially limit Indonesia’s ability to expand its nickel exports to the U.S.

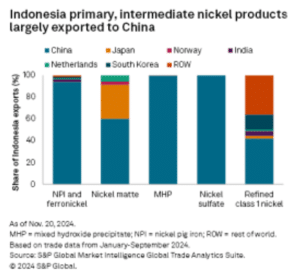

China remains a dominant player in Indonesia’s nickel sector. Between January and September 2024, Indonesia exported 129,860 metric tons of nickel sulfate exclusively to China.

If Indonesia faces challenges in accessing U.S. markets due to stricter IRA policies, its reliance on China is likely to deepen. This dynamic could reshape global nickel supply chains, with potential long-term implications for battery manufacturing and EV production.

Short-Term Pain, Long-Term Gain? Nickel’s Future Outlook

Beyond U.S. policy developments, other global factors are contributing to nickel market uncertainty. Escalations in the Russia-Ukraine war have dampened investor confidence, while concerns about slowing economic growth in China continue to weigh on demand projections.

The interplay of these factors has led to reduced risk appetite among investors, as evidenced by the sharp rise in short positions on LME nickel.

Despite these challenges, S&P Global’s fundamental outlook for primary nickel supply and demand remains broadly unchanged from previous forecasts. However, the near-term trading environment is expected to remain difficult.

Amid all these challenging market conditions, an emerging player is targeting U.S. nickel independence. Alaska Energy Metals Corporation (AEMC) is leading efforts to support the U.S. energy transition through its flagship Nikolai project in Alaska. The site holds a significant resource of nickel, copper, cobalt, and platinum group metals essential for renewable energy and electric vehicles.

The Canadian nickel junior’s dual focus on sustainability and critical mineral supply underscores its commitment to reducing U.S. reliance on imports.

With the nickel prices already at a multi-year low, the market’s recovery will depend on clearer policy signals and stronger demand drivers, particularly from the EV and clean energy sectors.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: AEMC.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png2024-11-29 08:44:352024-11-29 08:44:35Nickel Prices Fall to a 4-Year Low: What Causes The Plunge?

Cryptocurrency has revolutionized the financial world, offering decentralized, secure, and borderless transactions. However, its rise has come with a significant downside—high energy consumption. The world’s most popular cryptocurrency, Bitcoin relies on energy-intensive mining processes to secure its network, emitting lots of carbon dioxide. Meanwhile, other blockchain applications also contribute to this growing energy demand.

As the crypto industry expands, so do concerns about its environmental impact. This article explores how cryptocurrency and blockchain technology affect global energy consumption and carbon emissions. It explores how Green AI enables sustainable blockchain solutions. It also explains how blockchain can help carbon markets address some of its most pressing issues.

But first, let’s unveil how energy-intensive cryptocurrency mining is and whether Bitcoin can be truly green.

Can Bitcoin Be Truly Green? The Carbon Footprint of Cryptocurrency Mining

High energy consumption in cryptocurrency mining directly translates to significant carbon emissions, especially when powered by fossil fuels.

Bitcoin mining is notorious for its immense energy consumption. Here are the facts about crypto mining’s environmental impact:

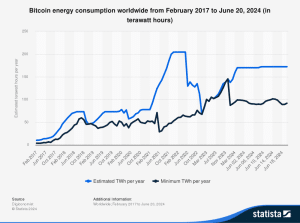

According to recent data, the Bitcoin network consumes around 127 terawatt-hours (TWh) of electricity annually—more than entire countries like Argentina and the Netherlands. This energy usage stems from the Proof-of-Work (PoW) mechanism, where miners compete to solve complex mathematical puzzles, requiring powerful hardware and vast amounts of electricity.

To put this into perspective, Bitcoin mining accounts for 0.55% of global electricity consumption, equivalent to the energy use of some large industrial sectors. As a result, the environmental cost of mining continues to spark debate, urging the industry to explore more sustainable practices.

Higher energy use translates into more carbon emissions…

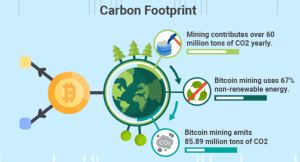

On average, a single Bitcoin transaction is responsible for emitting 300 to 400 kilograms of CO₂, equivalent to the carbon footprint of over 800,000 Visa transactions or 50,000 hours of YouTube streaming.

Globally, Bitcoin mining emits an estimated 69 million metric tons of CO₂ annually, comparable to the emissions of countries like Greece.

Image from GREENMATCH

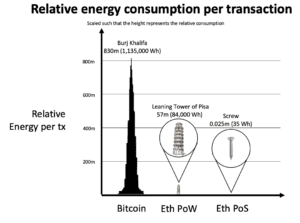

Moreover, cryptocurrency transactions, particularly those on the Bitcoin network, consume far more energy than traditional payment systems. As mentioned above, Bitcoin transactions use a lot more power than Visa processes.

A single Bitcoin transaction = 100,000 Visa transactions.

PayPal, another widely used platform, also operates with significantly lower energy consumption, processing thousands of transactions with minimal electricity use. This stark difference underscores the inefficiency of current cryptosystems compared to traditional financial networks.

The substantial environmental cost underscores the urgent need for cleaner energy sources and innovative solutions to reduce the crypto industry’s carbon footprint.

The Growing Role of Renewable Energy in Bitcoin Mining

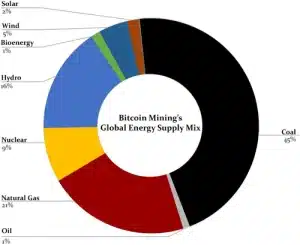

Recent data suggests that over 50% of Bitcoin’s mining network now uses renewable energy sources such as hydroelectric, wind, and solar power. For instance, regions like Iceland and Quebec, known for abundant renewable energy, have become hotspots for mining operations.

This transition is driven by economic and environmental incentives. Renewable energy is often cheaper than fossil fuels, reducing operational costs for miners. Furthermore, as governments introduce stricter regulations on carbon emissions, miners are motivated to adopt greener practices to avoid penalties and maintain their social license to operate.

Proof-of-Stake and Other Energy-Efficient Consensus Mechanisms

Bitcoin operates on a Proof-of-Work consensus mechanism, which is energy-intensive by design. Miners compete to solve complex mathematical problems, consuming significant electricity in the process.

In contrast, Proof-of-Stake (PoS) systems, like Ethereum’s, the second-largest blockchain, recent transition, eliminate the need for energy-hungry computations.

Instead of miners, validators are chosen based on the number of tokens they hold and are willing to “stake.” This drastically reduces energy consumption—Ethereum’s shift to PoS has cut its energy use by 99.95%, setting a benchmark for other cryptocurrencies.

Before its transition to Proof-of-Stake in 2022, Ethereum consumed around 78 TWh of electricity annually, comparable to Chile’s total energy use. Even smaller blockchains, such as Litecoin and Dogecoin, utilize PoW, albeit with lower energy requirements.

Source: Ethereum

On the other hand, many altcoins, including Cardano and Solana, have adopted PoS or other less energy-intensive models. These networks drastically reduce energy consumption, making them more sustainable.

However, the cumulative impact of various blockchains still adds to the global energy demand, highlighting the need for widespread adoption of greener technologies.

Apart from changing consensus mechanisms, innovative solutions like KlimaDAO offer a new way to address crypto’s carbon footprint.

KlimaDAO allows users, including Bitcoin miners, to purchase tokenized carbon credits, effectively offsetting their emissions. These credits represent verified reductions in greenhouse gases and are retired after purchase to ensure accountability.

One carbon credit equals one metric ton of CO₂ reduced or removed from the atmosphere.

Such initiatives align with broader climate goals, enabling the crypto industry to contribute positively to carbon neutrality. Another emerging trend that could help the industry tackle its environmental impact is Green AI (Artificial Intelligence).

Green AI: Powering Sustainable Blockchain Solutions

The concept of “Green AI” focuses on leveraging artificial intelligence to enhance sustainability and reduce environmental impact, aligning technology with climate action goals. AI can be used to optimize energy usage across various industries, minimizing emissions and maximizing efficiency.

For instance, AI-powered solutions can streamline energy grids, predict resource consumption, and identify areas for improved sustainability. It also supports the development of AI models and algorithms that optimize energy consumption in data centers, making them more energy-efficient.

Green AI includes using AI tools to track carbon emissions, forecast energy usage, and help industries transition toward renewable energy. For example, AI can optimize electricity demand response, helping utilities manage energy more efficiently while reducing carbon footprints.

By integrating AI with sustainability strategies, organizations can achieve measurable reductions in energy consumption, significantly lowering the carbon footprint of industries like manufacturing, transportation, and data management.

AI is also revolutionizing how blockchain networks manage energy. By analyzing real-time data, AI algorithms can predict network congestion, optimize transaction processing, and ensure efficient use of computing resources.

This dynamic allocation of energy minimizes waste and prevents overuse during low-demand periods. For example, predictive models powered by AI can anticipate peak activity times, enabling miners to adjust operations and reduce unnecessary energy expenditure.

AI-Driven Tools to Track and Reduce Crypto Carbon Emissions

AI also plays a critical role in monitoring and mitigating the carbon emissions of blockchain activities. Platforms equipped with AI can measure the carbon output of each transaction, offering insights into the environmental impact of specific operations. These tools provide actionable recommendations for reducing emissions, such as shifting workloads to energy-efficient times or integrating renewable energy sources.

For instance, projects like CryptoCarbonRank leverage AI to provide transparency on carbon emissions across various blockchain networks, empowering users and developers to make greener choices.

Bridging Blockchain and AI for Improved Transparency

Combining blockchain’s transparency with AI’s analytical capabilities has transformed the carbon credit market. Blockchain ensures the integrity of carbon credits by recording transactions in a tamper-proof ledger, while AI automates the verification process. This synergy prevents issues like double counting and fraud, which have historically plagued carbon markets.

AI-driven platforms also facilitate the issuance and trading of tokenized carbon credits. These innovations streamline the offset process, making it accessible to a broader audience while ensuring credibility and trust in global carbon offset initiatives.

Now, let’s consider specifically Bitcoin mining and how current efforts and innovations are helping the network become more sustainable.

The Evolution of Bitcoin Mining: Toward Sustainability

Bitcoin mining has historically depended on fossil fuels, contributing to significant carbon emissions. However, the industry is evolving as miners increasingly adopt renewable energy sources.

For example, China’s 2021 crackdown on crypto mining led many operations to relocate to countries with abundant renewable resources, such as the U.S. and Canada. In Texas, some mining companies use excess wind and solar power, stabilizing the state’s energy grid while reducing reliance on coal and natural gas.

As of 2024, nearly 40% of Bitcoin mining is powered by renewable energy sources, a significant improvement from previous years.

Source: AGU Pub

The shift toward renewables not only lowers carbon emissions but also reduces operational costs. Renewable energy, especially in regions with surplus capacity, is often cheaper than fossil fuels, creating a win-win scenario for miners and the environment.

From Proof-of-Work to Proof-of-Stake: Emerging Energy-Efficient Alternatives

Bitcoin’s PoW mechanism is the main culprit behind its high energy use and carbon pollution. By design, PoW requires miners to solve computational puzzles, consuming vast amounts of electricity. This has led to Bitcoin’s annual energy consumption surpassing that of some mid-sized countries.

Emerging alternatives like Proof-of-Stake are changing the game. PoS eliminates the need for energy-intensive computations, relying instead on validators who are selected based on their stake in the network. Ethereum’s switch to PoS has set a precedent, showcasing that major blockchains can significantly reduce energy consumption without compromising security or decentralization.

Cardano and Solana are among the leading PoS blockchains prioritizing energy efficiency. Cardano consumes only about 6 gigawatt-hours (GWh) annually, a fraction of Bitcoin’s energy use. Solana, known for its high-speed transactions, operates on a hybrid model with minimal energy requirements.

These networks demonstrate that advanced blockchain functionalities, such as smart contracts and decentralized applications (dApps), can be achieved without compromising environmental goals. Their energy efficiency also aligns with growing investor demand for greener technologies.

Crypto Projects for Nature-Based Carbon Solutions

Innovative projects like SavePlanetEarth (SPE) are tackling Bitcoin’s environmental challenges through nature-based solutions. SPE leverages blockchain technology to support reforestation and afforestation initiatives.

By tokenizing carbon credits linked to these projects, SPE provides a transparent and efficient way to offset emissions.

These initiatives not only mitigate the carbon footprint of Bitcoin mining but also contribute to broader environmental goals, such as biodiversity conservation and ecosystem restoration. Such projects demonstrate how blockchain and crypto can play a proactive role in addressing climate change.

Revolutionizing Carbon Markets with Blockchain

Talking about climate, carbon markets offer significant financial instruments that can help fund various emissions reduction initiatives.

However, traditional carbon credit systems often face challenges such as fraud and lack of transparency. Blockchain technology addresses these issues by providing a decentralized and immutable ledger for tracking and verifying carbon credits. Each credit is tokenized, representing a verified reduction or removal of greenhouse gas emissions.

By using blockchain, every transaction is transparent and traceable, ensuring the authenticity of carbon credits. This enhances accountability, especially for organizations looking to meet sustainability targets.

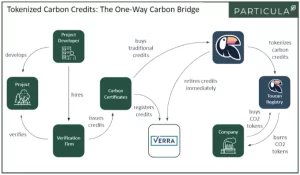

The Toucan Protocol is a prime example of how blockchain enhances trust in carbon markets. The platform tokenizes carbon credits, making them accessible to a broader audience. Each credit is verified and traceable, ensuring its integrity.

Image from Medium

Toucan also allows users to bundle smaller carbon offsets into larger, more marketable assets. This scalability supports global efforts to reduce emissions and makes it easier for companies and individuals to participate in offsetting programs. By combining blockchain’s transparency with innovative tokenization, Toucan is driving progress in carbon markets.

Major carbon standards like Verra and Gold Standard are exploring ways to integrate decentralized systems to improve the verification process.

Blockchain in Renewable Energy Grids

Blockchain is also transforming renewable energy grids by enabling peer-to-peer energy trading. In these systems, households, and businesses with solar panels can sell excess energy directly to others. Blockchain ensures secure and transparent transactions without the need for intermediaries.

Projects such as Power Ledger in Australia and LO3 Energy in the U.S. are leveraging blockchain to create localized energy markets. These initiatives promote renewable energy adoption while increasing grid efficiency and resilience.

The Issues of Double Counting, Scalability, and Trust

One of the most significant challenges in carbon offset markets has been double counting, where the same carbon credit is sold multiple times or claimed by different entities. Blockchain technology provides an effective solution by offering a transparent and tamper-proof record of each carbon credit transaction.

With blockchain, each carbon credit is tokenized, and its transaction history is recorded on a decentralized ledger. This ensures that once a credit is sold or retired, it cannot be reused or misrepresented, drastically reducing the risk of double counting.

Platforms like CarbonX are already implementing blockchain to safeguard the integrity of carbon offset programs. It is a private blockchain ledger designed to capture IoT-based greenhouse gas data for accurate reporting, management, and conversion into carbon commodities.

As Emission Trading Systems (ETS) and Carbon Tax programs continue to roll out globally, blockchain technology is poised to play a crucial role in ensuring compliance with environmental regulations. It also offers new opportunities for carbon asset trading, enhancing transparency and efficiency in the carbon market.

Not only that. Tokenization is a game-changer for carbon credits, making them easier to trade and track across borders.

By converting carbon credits into tokens, blockchain allows for fractional ownership, lower transaction costs, and greater liquidity in carbon markets. This scalability is crucial in meeting the global demand for offsets as businesses and governments strive to achieve their net-zero goals.

As mentioned earlier, the transparency of blockchain ensures that tokenized carbon credits are traceable, improving trust among buyers and sellers.

Blockchain’s Potential for Global Carbon Market Integration

Blockchain has the potential to integrate regional carbon markets into a unified global system, enabling seamless trading of carbon credits across borders. Using blockchain to track credits from multiple countries and regions ensures that the credits are authentic and can be used toward global emissions reduction goals.

This integration not only supports international climate agreements but also fosters collaboration between countries, corporations, and environmental organizations. As such, blockchain could ultimately drive the global carbon market toward greater transparency, efficiency, and scalability. It can then provide a unified approach to tackling climate change.

Final Thoughts

Cryptocurrency and blockchain technology have transformed global finance and data systems, but their environmental impact cannot be ignored. Bitcoin and other crypto networks consume vast amounts of energy, contributing to significant carbon emissions. However, the industry is actively working toward sustainability, with renewable-powered mining, energy-efficient blockchains, and carbon offset initiatives leading the way.

As crypto adoption grows, the balance between innovation and environmental responsibility will be crucial. By embracing greener technologies, the industry can pave the way for a more sustainable digital future.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png2024-11-28 16:18:252024-11-28 16:18:25The Energy Debate: How Bitcoin Mining, Blockchain, and Cryptocurrency Shape Our Carbon Future

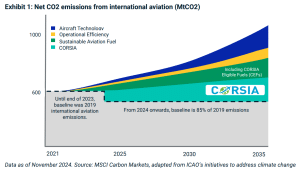

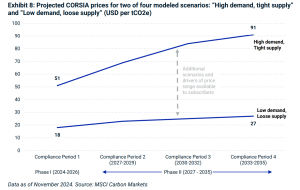

A report analyzing carbon credit demand for over 400 airlines under the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) projects significant fluctuations in credit prices and airline costs.

According to modeling by MSCI Carbon Markets, CORSIA-eligible carbon credits could cost between $18-51 per tonne of carbon dioxide equivalent (CO2e) during Phase I, rising to $27-91 in Phase II. If airlines pass these costs on to consumers, international ticket prices could increase by 0.5-1.0% in Phase I.

Alternatively, if airlines absorb the costs, their operating profits could decrease by up to 4%. The impact will vary depending on different demand and supply scenarios.

We crunch the report and here are our key takeaways.

What Are CORSIA Credits? A Flight Plan for Emission Reductions

The aviation sector is one of the fastest-growing contributors to global greenhouse gas (GHG) emissions. As international air travel expands, airlines face increasing pressure to mitigate their environmental impact.

The CORSIA, developed by the International Civil Aviation Organization (ICAO), is designed to limit emissions growth in international aviation. By purchasing carbon offsets known as CORSIA credits, airlines can balance emissions exceeding 2020 levels and invest in sustainability.

CORSIA credits allow airlines to compensate for their emissions by funding projects that reduce or remove CO2. These projects include renewable energy initiatives, reforestation, and carbon capture technologies. Verified under internationally recognized standards such as the Verified Carbon Standard (VCS) and the Gold Standard, these credits ensure that emission reductions are real, additional, and permanent.

CORSIA aims to cap international aviation emissions at 2020 levels. Through its two implementation phases—voluntary (2021–2023) and mandatory (from 2024)—the program encourages investment in global sustainability while aligning the aviation industry with broader climate goals.

Carbon Credit Demand: Will Airlines Keep Up with Rising Costs?

CORSIA’s demand for carbon credits hinges on international aviation growth and decarbonization efforts. Using a bottom-up modeling approach, MSCI Carbon Markets analysts assess individual airline emissions, growth rates, and adoption of sustainable practices to project credit needs.

Demand Scenarios

Three scenarios highlight the variability in credit demand:

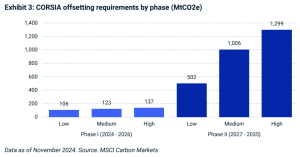

High-Demand Scenario: Strong aviation growth (+4% annually) and slow adoption of sustainable aviation fuels (SAFs) result in higher offsetting needs. Estimated demand reaches 137 million metric tons of CO2 equivalent (MtCO2e) in Phase I (2024–2026) and 1,299 MtCO2e in Phase II (2027–2035).

Medium-Demand Scenario: Moderate aviation growth and increased decarbonization lower credit demand to 123 MtCO2e in Phase I and 1,006 MtCO2e in Phase II.

Low-Demand Scenario: Limited growth and poor adoption of SAFs reduce requirements to 106 MtCO2e in Phase I and 502 MtCO2e in Phase II.

Regional and Airline-Level Insights

Demand will be concentrated among major airlines and regions. For instance, the top 10 airlines are expected to account for 40% of cumulative demand by 2035.

European carriers are likely to lead credit purchases despite regional compliance mechanisms such as the EU Emissions Trading System (ETS). If the ETS is expanded to cover more flights, global demand for CORSIA credits could decrease by 25–50% by 2050.

Supply Struggles: Why CORSIA Credit Availability Could Impact Aviation

The supply of CORSIA-eligible credits faces significant challenges. Credits must meet ICAO criteria, including corresponding adjustments that prevent double counting of emissions reductions under a country’s Nationally Determined Contributions (NDCs). This process requires host countries to authorize projects and align carbon accounting frameworks—a complex and underdeveloped requirement.

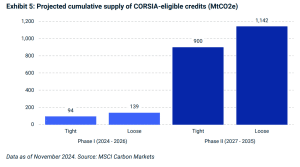

As of late 2024, ICAO-approved registries like Verra, Gold Standard, and Climate Action Reserve have expanded the potential credit pool to 230 MtCO2e. However, only 7 MtCO2e of these credits meet Phase I criteria due to limited corresponding adjustments.

Most eligible credits have been issued by a single REDD+ project in Guyana under ART TREES.

A lack of Letters of Authorization (LoAs) from host countries further constrains supply. Of 40 major credit-producing countries assessed, only two are highly prepared to issue LoAs. Without accelerated regulatory progress, substantial credit supply growth is unlikely until the late 2020s.

Projections and Flexibility

Supply projections factor in registry eligibility, crediting timelines, and the readiness of host countries to provide corresponding adjustments. A 30% reduction is applied to projects not yet in the registry pipeline. Despite these hurdles, expanded registry approvals and government action could gradually increase the availability of CORSIA-compliant credits.

Scenarios for Carbon Prices: How High Will CORSIA Credits Soar?

The prices of CORSIA credits will depend on supply-demand dynamics, influenced by credit availability, international aviation growth, and compliance requirements.

Under high-demand and tight-supply scenarios, Phase I credit prices are expected to range between $18 and $51 per ton of CO2. Prices could climb to $27–$91 per ton during the fourth compliance period (2033–2035) as demand peaks.

Supply-Demand Scenarios

Tight Supply: A potential deficit of 12–43 million tons of CO2 in Phase I could drive prices higher.

Loose Supply: A surplus of 2–33 million tons of CO2 may stabilize prices during Phase I. Airlines also have a grace period until January 2028 to offset emissions, easing initial supply constraints.

In Phase II, higher demand from aviation and other sectors, such as corporate voluntary commitments and sovereign programs, could lead to significant price increases.

Market Value Estimates

The market for CORSIA-eligible credits could reach $2–$8 billion by Phase I and grow to $5–$66 billion by the fourth compliance period. This growth reflects both rising demand and the financial implications of carbon market integration.

Implications for Airlines and Carbon Markets

CORSIA credits are an essential tool for airlines to manage emissions and comply with climate regulations. However, reliance on credits is only a short-term solution.

Long-term strategies include investment in SAFs or Sustainable Aviation Fuel, fleet upgrades, and operational efficiencies. Airlines with slower decarbonization may face higher offsetting costs, incentivizing innovation and sustainable practices.

Geopolitical factors and regulatory developments will heavily influence the carbon market. Expanding participation and ensuring the environmental integrity of credits are critical to maintaining trust and achieving emissions reductions.

CORSIA credits are pivotal to the aviation industry’s efforts to cap emissions and contribute to global climate goals. Although challenges remain in scaling credit supply and ensuring regulatory compliance, CORSIA serves as a transitional mechanism while the sector invests in greener technologies. As demand for high-quality offsets grows, the aviation industry’s collaboration with carbon markets will shape the roadmap of global emissions reductions.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png2024-11-28 12:17:382024-11-28 12:17:38CORSIA Credits Soaring Costs: How They Are Reshaping Aviation’s Future

Ever since Trump came to power, there have been serious speculations about the future of America from a climate perspective. We saw clean energy stocks tumbling like a pack of cards and Trump’s “drill, baby, drill” policies eventually taking shape.

Well, at this conjecture Reuters came up with an interesting report explaining that Donald Trump’s energy team is planning an aggressive agenda to reshape U.S. energy policy. He will prioritize expanding liquefied natural gas (LNG) exports, increasing offshore oil drilling, and streamlining permits for federal land projects.

These actions signal a dramatic shift from the Biden administration’s climate-focused pro-renewables policies. Let’sdeep dive into what’s onTrump’s agenda…

Fast-Tracking LNG Exports, Restart Oil and Drilling

The report further highlighted that under the Biden administration, several significant LNG projects were delayed. Venture Global’s CP2, Commonwealth LNG, and Energy Transfer’s Lake Charles facilityall of them are based inLouisiana. Trump wants to de-freeze and approve these projects which would send a strong message of support for the natural gas sector.

Federal records revealed,

“Five U.S. LNG export projects that have been approved by the Federal Energy Regulatory Commission are still awaiting permit approvals at the Department of Energy (DOE).”

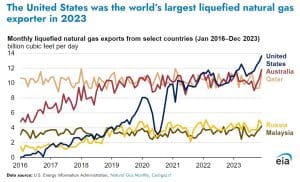

The U.S., as the leading LNG exporter, plays a key role in global energy. With Europe seeking U.S. gas to cut reliance on Russia, Trump aims to seize the opportunity. This means there would be faster approvals, unlocking massive LNG infrastructure investments.

EIA notes, that in 2023 the U.S. LNG exports averaged 11.9 billion cubic feet per day (Bcf/d)—a 12% increase (1.3 Bcf/d) compared with 2022.

Notably,Trump’s team also aims to accelerate oil and gas drilling off the U.S. coast and on federal lands. Federal lands currently account for a quarter of U.S. oil production and 12% of natural gas output.

During his first term, drilling permits took significantly less time to process compared to the Biden administration. This time he plans to reinstate a concrete long-term drilling plan that would expand offshore lease sales and fast-track all permit approvals to increase energy product. His focus will primarily be on regions having rich oil reserves.

Now taking about the stats, Reuters reported,

“According to federal data, oil output on federal lands and waters hit a record in 2023, while gas production reached its highest level since 2016.”

The report also revealed that Trump is most likely to persuade the IEA on pro-oil decisions. However, his advisors have urged him to suppress funding unless the IEA adopts a more pro-oil stance.

Dan Eberhart, CEO of oilfield service firm Canary said,

“I have pushed Trump in person and his team generally on pressuring the IEA to return to its core mission of energy security and to pivot away from greenwashing.”

A symbolic yet bold move would be Trump’s push to approve the Keystone XL pipeline, a project canceled downrightly by Biden. However, reviving the pipeline has challenges, as land easements have been returned and construction would require starting from scratch. Even so, Trump’s endorsement signals a commitment to fossil fuel infrastructure.

Trump’s Stance on Inflation Reduction Act:A “Green Scam”?

Prior to his win, we have read and seen all around how he openly criticized the Inflation Reduction Act (IRA), calling it a “green scam”. He also pledged to repeal it if he returned to power once again.

This bold statement has raised questions about the future of the Biden administration’s $369 billion energy transition agenda. While his rhetoric may signal trouble for renewable energy sectors like electric vehicles (EVs) and wind power, Trump’s track record suggests a more nuanced approach to industrial policy and critical mineral supply chains.

But Critical Minerals are Safe in Trump’s Hands…

The IRA has funneled significant resources into renewable energy, but it also supports rebuilding America’s industrial base. For instance, $75 million was allocated to upgrade Constellium’s aluminum rolling mill in West Virginia. Efforts like these align with Trump’s earlier policies emphasizing industrial revitalization and reduced reliance on foreign nations for critical resources.

In 2020, Trump declared the United States’ dependence on foreign critical minerals a national emergency. A second Trump administration is unlikely to abandon this push for metal self-sufficiency. Instead, he may amplify efforts to boost domestic production of key materials like aluminum, nickel, and lithium.

The good news is cross-party consensus on this issue suggests that funding for industrial projects tied to critical minerals may be safe, even under a Republican administration.

America First: China in Scrutiny

Both the Department of Energy (DOE) and the Department of Defense (DOD) have prioritized investments in rebuilding U.S. metals capacity. While the DOE focuses on EV battery metals like lithium, the DOD has diversified its investments toward antimony to zirconium. All these moves align toward reducing dependency on China for critical minerals.

Projects like Talon Metals’ Tamarack nickel initiative in Minnesota have already received federal funding. However, the nickel market faces significant challenges due to Indonesia’s mining boom, which has driven down prices. Most of Indonesia’s nickel production is controlled by Chinese entities, complicating matters for U.S. companies like Ford, which are sourcing Indonesian nickel for EV batteries.

Trump’s “America First” philosophy highlights his strong opposition to critical metal imports from China. His administration will probably scrutinize even joint ventures like Ford’s collaboration with Indonesia’s Vale and Huayou Cobalt. Even if these ventures technically qualify for IRA subsidies, their ties to Chinese supply chains may face new barriers under his administration.

Can America Be Great Again?

Despite Trump’s bitterness about the IRA, his administration may continue supporting parts of it that align with domestic industrial goals. Consequently building U.S. mineral independence will significantly reduce reliance on China and secure advanced technology materials.

Concisely, this means a second Trump presidency might prioritize America’s self-sufficiency while addressing IRA’s initiatives to fit in his “Make America Great Again” agenda.

This report suggests that Trump’s policies could possibly reinforce a robust U.S. oil, gas, and critical minerals industry. While his decision on renewables like EVs and tariffs on imports are still uncertain, he prioritizes critical minerals which is assuring for national security and economic competitiveness.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png2024-11-28 11:16:482024-11-28 11:16:48Trump’s Tactic to Make America Great Again: Expanding Domestic Oil, Gas, and Critical Minerals

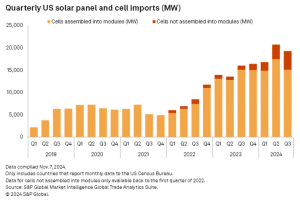

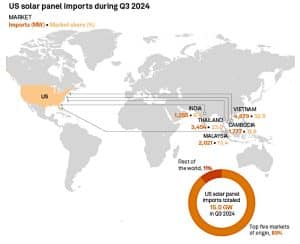

US imports of crystalline-silicon solar cells saw a dramatic increase in the third quarter of 2024, rising more than fourfold compared to the same period in 2023, according to S&P Global Commodity Insights. This surge reflects the growing demand from rapidly expanding domestic solar panel factories, fueled by policy shifts and significant investments in US solar manufacturing.

Solar Power Driving Up the Clean Energy Revolution

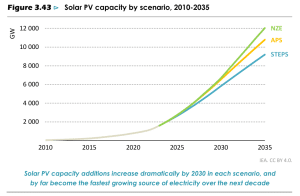

Solar energy is accelerating global energy transitions, driven by affordability and technological advancements. According to the IEA’s World Energy Outlook 2024, solar photovoltaic (PV) systems are a leading force in clean energy deployment.

By 2030, solar could account for over 40% of new power capacity, emphasizing its pivotal role in global decarbonization efforts.

Moreover, renewables’ electricity generation share will climb from 22% to 58% by 2035, driven primarily by solar PV. This growth is supported by record investment and strong policy support in renewables, helping to address energy security concerns and reduce emissions.

The 2022 Inflation Reduction Act (IRA), central to Biden’s clean energy policy, provides up to $1.2 trillion in tax incentives over a decade to drive clean energy growth. Its advanced manufacturing tax credit has spurred over $34 billion in solar investments. This resulted in numerous new or expanded solar module factories across the U.S.

Solar module production capacity in the country has skyrocketed, exceeding 45 GW as of October. At peak production, these solar manufacturing facilities could fulfill most of the U.S. solar demand projected for 2025.

Imports of photovoltaic (PV) cells not yet assembled into panels reached 4,230 MW in Q3. That is a sharp increase from 903 MW in the third quarter of 2023, according to S&P Global Market Intelligence’s Global Trade Analytics Suite.

Over the first nine months of 2024, unassembled PV cell imports totaled 9,454 MW, up nearly 286% from 2,448 MW during the same period in 2023.

This increase follows President Joe Biden’s August decision to raise the annual cap on tariff-free PV cell imports from 5 GW to 12.5 GW. Biden highlighted the solar industry’s “positive adjustment to import competition” and the growth in module production capacity as key reasons for the policy change.

The IRA has played a pivotal role in incentivizing domestic solar panel production through lucrative tax credits. However, despite these gains, a lack of crystalline cell, wafer, and ingot manufacturing capacity in the US leaves panel manufacturers heavily reliant on imported components.

With President-elect Donald Trump promising to introduce new tariffs on foreign-made goods to support US manufacturing, the solar industry is preparing for potential shifts in trade policy that could impact supply chains.

Robust Module Imports

While domestic module production ramps up, imports of fully assembled solar panels remain strong. The US imported 15 GW of modules in Q3 2024, slightly lower than the record 17.4 GW in Q2 but consistent with Q3 2023 levels, per S&P Global report.

For the first nine months of 2024, total panel imports reached 47.3 GW, up from 41 GW in the same period last year. Combined cell and module imports for January–September exceeded 56.7 GW, representing a 31% increase from the 43.4 GW imported during the same period in 2023.

With this robust supply chain, the US solar market could install over 46 GWdc of solar panels in 2024. Plus, an additional 43.3 GWdc in 2025, according to S&P Global Commodity Insights.

The majority of crystalline solar cell imports in Q3 came from factories in Southeast Asia as shown above. Malaysia led the pack, accounting for 37.3% of U.S. imports, followed by Thailand (27.6%) and South Korea (20%). Vietnam and Laos contributed smaller shares, at 4% and 3.7%, respectively.

Panel imports, including both crystalline and thin-film technologies, were also primarily sourced from Southeast Asia. Vietnam supplied 32.5%, Thailand contributed 23%, and Malaysia accounted for 13.4%. Other key contributors included Cambodia (11.8%) and India (8.4%).

Leading the Solar Revolution: Top Companies Driving Innovation

As solar energy is gaining momentum globally, key players are also making significant strides.

For one, Toronto-based SolarBank Corporation, focusing on utility-scale and community solar projects across North America, just delivered 600 MW of clean energy in the U.S. and Canada. Expanding into new markets like New York, its initiatives offset significant carbon emissions, accelerating the energy transition.

Another solar company is NextEra Energy, a clean energy powerhouse headquartered in Florida. With over 72,000 MW of generating capacity, it leads in wind and solar power production. NextEra is reducing carbon emissions through renewable energy and innovative technologies.

Similarly, Arizona-based First Solar specializes in thin-film PV panels, boasting a lower carbon footprint and superior durability. With 25 GW of installed capacity and a target to reach 16 GW annual production by 2025, its innovations power major solar farms worldwide.

These companies showcase the transformative potential of solar energy in achieving a sustainable future.

As the country prepares for potential changes in trade policy under Trump’s administration, companies must adapt to evolving regulations. For now, the combination of robust imports and growing domestic production capacity positions the U.S. solar market for sustained growth, supporting the transition to clean energy.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png2024-11-27 14:44:562024-11-27 14:44:56US Solar Imports Surge 286% as Domestic Manufacturing Expand, S&P Global Data Says

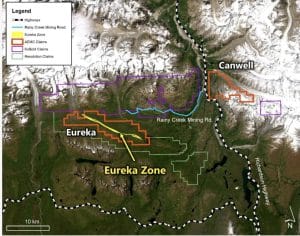

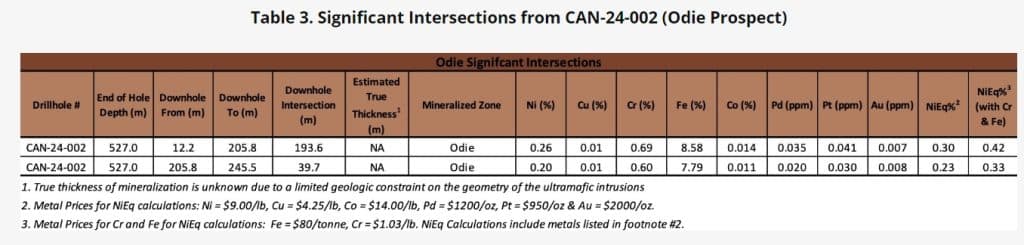

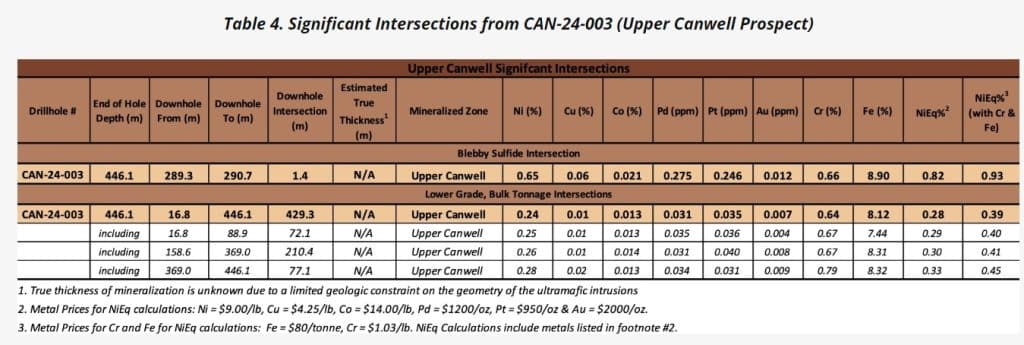

Alaska Energy Metals Corporation (AEMC) has unveiled exciting findings from its 2024 inaugural exploration drilling program at the Canwell claim block which is a part of the Nikolai Project in Alaska. The Canwell area hosts three key prospects—Emerick, Odie, and Upper Canwell—located about 30 kilometers northeast of AEMC’s nickel-rich Eureka deposit.

AEMC’s Eureka Deposit: A Foundation for Growth

Exploring deeper, AEMC’s flagship Eureka deposit is a massive polymetallic resource with over 3.9 billion pounds of nickel in the Indicated category and 4.2 billion pounds in the Inferred category. This deposit also includes critical materials such as cobalt, chromium, platinum, and palladium. It also holds copper, iron, and gold which positions AEMC as a significant player in the strategic metals sector.

The advantage doesn’t end here, having such a rich resource potential aligns with U.S. government priorities for securing domestic supplies of strategic metals.

Nikolai Project – Property Location Map

Breaking Ground at Canwell: Promising Results for Nickel and Critical Metals

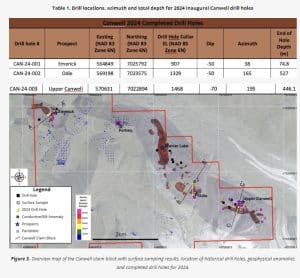

According to the company’s press release they used one surface diamond drill rig to drill three holes across the Emerick, Odie, and Upper Canwell prospects, covering a total of 1,047.9 meters. Each hole targeted geological, geophysical, and geochemical anomalies, providing valuable data for understanding the region’s mineralized ultramafic systems.

Alaska Energy Metals Chief Geologist Gabe Graf commented,

“After 20 years of limited exploration on the Canwell property, the information collected from these drill holes will aid our understanding of the mineralized ultramafic systems within the Wrangellia Terrane of interior Alaska. In fact, the blebby sulfides intersected at the Upper Canwell prospect is the first subsurface indication for higher-grade sulfides on the property. Furthermore, the potential for coarser-grained nickel sulfides and additional disseminated sulfide zones on the Nikolai Project is encouraging, and we are excited to continue advancing the geologic understanding of the property. We look forward to getting back into these areas in the next exploration season.”

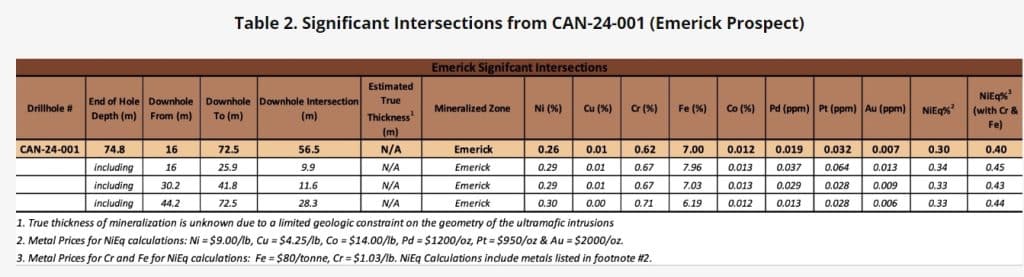

Drill hole CAN-24-001 started with 16 meters of overburden, followed by serpentinized peridotite containing 0.2–0.5% sulfide minerals. The drilling reached a depth of 72.5 meters before encountering challenging rock conditions. These included intense fracturing, clay alteration, and serpentinization, which made sulfide estimation difficult.

Non-mineralized mafic dikes were also present within the peridotite. Drilling became harder due to poor rock quality, and the hole was abandoned at 74.8 meters due to a large fault. Unfortunately, it did not reach the targeted magnetic anomaly or the base of the ultramafic intrusion.

Rather than retrying, the team decided to postpone further drilling on this target until 2025. The key findings were:

Drill hole CAN-24-002 started with 12.2 meters of overburden, followed by serpentinized dunite containing 0.2–6.0% nickel sulfide and Ni-Fe alloy. This mineralized zone extended to a depth of 245.5 meters. Within the dunite, several non-mineralized gabbroic dikes were found.

At 245.5 meters, the drill hit an unmineralized diorite intrusion, which continued down to 527.0 meters. The targeted DIGHEM magnetic anomaly is believed to mark the contact between the mineralized dunite and the diorite intrusion. This area also showed increased pyrrhotite content, offering valuable clues for further exploration. The team discovered:

Drill hole CAN-24-003 began with 16.8 meters of overburden, followed by serpentinized and faulted dunitic rocks. These rocks showed 0.5–5.0% nickel sulfide and Ni-Fe alloy mineralization. Several cross-cutting gabbroic dikes with minimal sulfide mineralization were also encountered.

Due to challenging terrain, the drill site was relocated north of the original plan. This adjustment allowed the team to test multiple geophysical targets and resulted in drilling down the dip of the intrusion.

The targeted DIGHEM magnetic anomaly showed higher sulfide content and better nickel grades, confirming its exploration potential. The key findings were:

AEMC upholds stringent Quality Assurance – Quality Control for its Nikolai Project to ensure the best practices for logging, sampling, and analysis of samples.

As revealed by the company,

“For every 10 core samples, geochemical blanks, coarse reject or pulp duplicates, or Ni-Cu-PGE-Au certified reference material standards (CRMs) were inserted into the sample stream.”

Furthermore, drill cores were flown daily to the McLaren River Lodge in Alaska, where they were meticulously logged, labeled, and cut. Half of each core was archived, while the other half was sent to SGS Laboratories in Burnaby, B.C., for detailed analysis using advanced geochemical methods.

This indicates that the company integrates environmental, social, and governance (ESG) principles into its operations. At the same time focusing on sustainable practices and carbon reduction. With offices in Anchorage and Vancouver, AEMC aims to supply critical materials essential for national security and clean energy.

What’s Next for AEMC?

Significantly, the recent results at Canwell strengthen the vision for district-wide exploration across the Nikolai Project. By confirming nickel mineralization and identifying promising areas for future drilling, AEMC has highlighted the potential for major discoveries in Alaska’s interior.

They plan to revisit the site in the 2025 season, targeting expanded sulfide zones and higher-grade nickel deposits. In addition to the Nikolai Project, AEMC is advancing the Angliers-Belleterre Project in Quebec, which holds potential for high-grade nickel-copper sulfides and white hydrogen.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: AEMC.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png2024-11-27 13:44:562024-11-27 13:44:56Alaska Energy Metals Corporation Unlocks Vast Nickel and Critical Mineral Potential at Canwell Property, Nikolai Project, Alaska

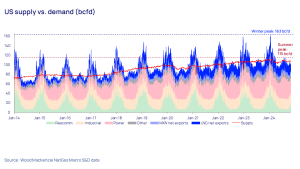

The natural gas market has immensely benefitted this year from robust storage levels and stabilized prices after the sharp spikes of 2022. However, challenges such as volatile pricing, seasonal demand fluctuations, and supply-demand imbalances persist. The emergence of renewable natural gas (RNG) and LNG export projects reflects ongoing structural shifts in this dynamic energy landscape of North America.

Industry experts predict that the North American natural gas market is projected to grow at a 5% CAGR between 2022 and 2027. This will be driven primarily by increasing industrial demand from the refining, petrochemical, and fertilizer sectors.

Winter 2024: What Will Drive North America’s Natural Gas Markets?

Apart from production levels and storage capacity, the North American natural gas market is also shaped by power market trends, LNG exports, imports, and changing weather patterns. But which of these will play the most critical role in the upcoming season? Let’s study the Wood Mackenzie findings…

Cold Snaps Impact Demand and Supply

Changing weather conditions significantly impact the natural gas market. And this is the direct effect of climate change. Cold snaps not only just spike demand, they also disrupt supply. Freeze-offs, where water or liquids in gas wells solidify and block production, are a recurring issue in North America.

Wood Mac reports that historically, these events have reduced about 0.7% of Lower 48 output during winter. However, losses vary and depend on the location and intensity of the cold. These disruptions are most critical because they hit supply when demand peaks.

LNG Exports Fluctuate Gas Price

LNG exports are driving growth in the U.S. gas market, with new projects like Venture Global’s Plaquemines in Louisiana and Cheniere Energy’s Corpus Christi expansion boosting capacity. However, this surge constricts domestic gas supplies, especially when demand is at its highest level.

For instance, natural gas inflows for LNG exports dropped from 15 billion cubic feet per day (bcfd) to 7 bcfd to meet local needs due to severe cold this January. This shortage drove Henry Hub prices to $13, with some regions experiencing even higher spikes. This showed that LNG exports are increasingly acting as “synthetic storage,” thereby balancing supply when stored gas falls short.

Production Choices May Strain the Supply

North American natural gas producers are increasingly managing supply through proactive decisions. Companies like EQT and Expand Energy (formerly Chesapeake Energy) have found strategic ways to adjust the supply based on market price.

Some techniques like delaying the activation of new wells or turning existing wells on and off can transform gas production into “synthetic storage“. However, this widely adopted approach is expected to still keep markets unpredictable this winter.

Naturalgas demand for electricity generation has also become more unpredictable. Several factors influence this surge, including the retirement of coal plants, low gas prices fueling coal-to-gas switching, and an overall increase in power load.

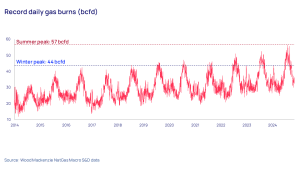

Power generation during summer hit a record high of 58 bcfd of gas, surpassing 50% of the total U.S. production of just over 100 bcfd. Last winter, demand also peaked at a record 44 bcfd, reflecting a year-round trend.

However, renewable energy plays a key role in the power sector. Simply put, during summer solar availability is high, while wind power is low and it’s just the opposite during winter. These fluctuations increase reliance on natural gas during extreme weather.

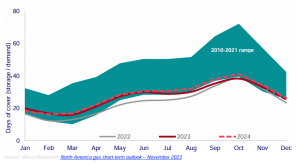

Storage Shortfalls and Supply Concerns

Storage capacity acts as a buffer during high demand or low supply. The report revealed that in recent years, storage capacity was limited. This was mainly due to narrow summer-winter price spreads which offered very minimal commissioning to set up new storage facilities. The planned 50 billion cubic feet of capacity falls short of market needs.

The demand for stored gas remains substantially high during peak winters like in January 2024 which led to 64 bcfd withdrawals. Conversely, the “days of cover” metric, measuring storage relative to demand, remains low in the cold. Thus, raising supply concerns.

Price Volatility

We can comprehend now that North America’s natural gas market faces significant instability due to storage-related struggles. However, this year storage inventories showed a 10% surplus compared to the five-year average which caused a sharp price drop in Henry Hub gas prices.

Despite this surplus, long-term storage capacity lags behind market expansion. Currently, U.S. storage covers only 25 days of full demand—a historic low. Without significant expansion, volatile prices could dominate the years ahead.

US L48 storage represented as days of demand cover

North America’s Natural Gas Market: Opportunities Amid Challenges

We have studied the challenges that North America’s gas market faces but at the same time, it has transformed significantly tapping the opportunities that lie ahead. Quite evidently, natural gas will play a vital role while replacing coal and renewables, bolstering the energy mix.

Several ongoing and upcoming projects will expand capacity and address the challenges related to price, demand, and supply of natural gas.

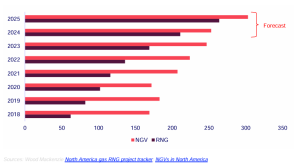

Renewable Natural Gas Gains Momentum

Renewable Natural Gas (RNG) has emerged as a promising tool for decarbonization. Supported by policies like California’s Renewable Gas Standard, RNG production is growing, with 324 projects in operation across the U.S. and Canada.

In 2024, demand-side contracting is expected to gain traction, particularly in hard-to-decarbonize sectors and heavy-duty transportation. Companies like Walmart and UPS are already testing RNG-powered fleets which signals a transition toward sustainable fuel solutions.

North American gas RNG production and NGV demand

LNG Export Boom: North America’s Next Wave

With rising U.S. and Canadian gas production and storage levels hitting highs in 2023, the North American gas market eagerly waits for the upcoming LNG export projects. While the timelines for large-scale terminals like Plaquemines and Golden Pass are well-known, the impact of this new demand surge remains uncertain.

Low gas prices have recently discouraged production growth. However, forward price projections showing premiums of up to $4/mmbtu for late 2024 and 2025 signal more lucrative returns when this demand kicks in.

Some promising LNG projects in North America includePlaquemines LNG Phase 1 in Louisiana, Golden Pass LNG, The Corpus Christi, Fast Altamira FLNG project in Mexico, LNG Canada, etc.

These developments highlight the growing structural demand for LNG across North America and beyond. While challenges persist, the region’s LNG export potential is poised to reshape global energy markets.

All in all, natural gas continues to be pivotal for North America’s energy system. However, it’s crucial to tackle challenges like weather, limited storage, redundant infrastructure, and the need to integrate renewables smoothly. So, overcoming these hurdles will be key to ensuring the sector’s growth and stability in the future.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png2024-11-26 12:47:362024-11-26 12:47:36What’s Shaping North America’s Natural Gas in 2024? Insights from Wood Mackenzie

With 85 million electric vehicles (EVs) expected on the road by 2025, the demand for lithium is skyrocketing. However, traditional lithium extraction methods pose serious environmental risks. They deplete water supplies, contaminate ecosystems with chemicals, and rely heavily on energy-intensive mining processes that expand the carbon footprint.

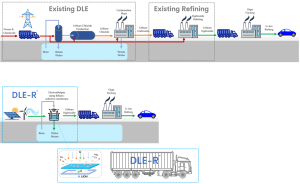

ElectraLith, a Melbourne-based startup backed by Rio Tinto, is tackling these issues with its Direct Lithium Extraction (DLE) technology. This innovative process bypasses the need for water and chemicals, extracting lithium directly from brine solutions.

The lithium tech startup is set to conclude a funding round worth A$27.5 million (almost $18 million) next week to support its global growth initiatives. CEO Charlie McGill confirmed the plans, as reported by Reuters.

ElectraLith’s Game-Changing Lithium Technology

Traditional lithium production can take months and devastate water-stressed regions like Chile’s Atacama Desert. ElectraLith’s proprietary DLE-R technology completes the process in hours, drastically cutting production time and environmental costs.

The tech’s advanced filtration membranes convert lithium into lithium hydroxide while reinjecting unused brine into aquifers, ensuring minimal environmental disruption.

According to McGill, this breakthrough is especially critical in areas where water scarcity makes conventional mining untenable. He specifically noted that:

“You can’t get a water permit [referring to water-stressed regions like the Colorado River basin]… So we show up and we are like, ‘We don’t need water.’”

Backed by Rio Tinto, venture capital firm IP Group, and Monash University, ElectraLith is preparing to scale its operations. The company’s upcoming funding round, which has been oversubscribed—is a testament to investor confidence despite a challenging market.

The funds will support the construction of ElectraLith’s first pilot plant at Rio Tinto’s Rincon operations in Argentina, set to be operational within a year. Two additional pilot plants are planned, as the company aims to produce lithium hydroxide at half the cost of competitors.

Transforming the $10 Billion Lithium Industry

Direct Lithium Extraction is expected to drive the lithium industry’s growth to over $10 billion in annual revenue within the next decade. ElectraLith’s energy-efficient process not only accelerates production but also positions the company as a leader in sustainable EV battery material supply.

By addressing the dual challenges of water scarcity and environmental impact, ElectraLith’s technology could redefine lithium production. As McGill emphasizes:

“This isn’t just a better method—it’s a necessary one for the future of EVs and the planet.”

With its revolutionary approach, ElectraLith is paving the way for a greener, more efficient future in lithium extraction and EV battery manufacturing.

Cutting Costs and Carbon, Not Corners: Lithium at Half the Price?

Lithium prices have been a driving force in the EV battery market, with significant fluctuations impacting producers and manufacturers.

After peaking at nearly $85,000 per metric ton in late 2022, prices have recently cooled, stabilizing around $26,000 per metric ton. While this decline offers some relief to EV makers, it has created challenges for lithium producers, especially those reliant on cost-intensive extraction methods.

High-cost concentrate operations, including Nemaska, Mt Cattlin, and North American Lithium (NAL), are at risk of losses unless spodumene prices rise above $800/ton.

To stay competitive, Sayona Mining and Piedmont Lithium, the two owners of NAL, announced a merger to streamline costs. This partnership, unlike the large-scale acquisition of Arcadium Lithium by Rio Tinto, focuses on cutting corporate overhead and operational inefficiencies.

However, challenges remain. Protectionist trade policies and the potential repeal of the US EV tax credit could dampen demand for Canadian lithium exports, adding further pressure to high-cost producers.

ElectraLith’s Direct Lithium Extraction technology offers a significant cost advantage. By producing lithium hydroxide at nearly half the cost of traditional methods, the company is poised to thrive even in volatile market conditions. This cost efficiency could help buffer against future price fluctuations, ensuring a steady supply of affordable lithium for EV battery production.

The cost of lithium is a critical factor for the industry, per Charlie McGill. However, their technology allows them to maintain competitiveness, even in challenging markets.

Lithium Prices: A Story of Volatility

The lithium market remains dynamic, with prices responding sharply to changes in supply and demand.

On November 13, the Platts-assessed lithium carbonate DDP China price surged by 6.4% to reach 83,000 yuan/ton, a three-month high. This rally followed production curtailments at key Australian mines and stronger-than-expected battery and cathode demand in China.

Although prices eased to 79,500 yuan/ton by November 21, they still marked a 6.7% increase from the start of the month.

Spodumene concentrate prices have stayed stable, averaging $820-$830/ton through mid-November, according to S&P Global data. Meanwhile, China’s traction battery production in October demonstrated unusual resilience, declining only 1.3% month-over-month compared to a 10.1% drop a year earlier.

Data suggests a recovery in battery and cathode output, further boosting demand for lithium.

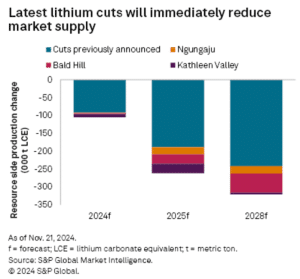

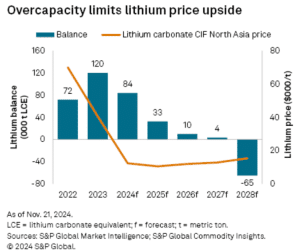

A wave of supply curtailments, shown in the S&P Global chart below, has also tightened the market. The latest cuts include halting operations at the Bald Hill and Altura mines and reducing 2025 production by 73,000 metric tons of lithium carbonate equivalent (LCE). Meanwhile, Australia’s Kathleen Valley mine has announced plans to delay and trim production.

The tightening supply coincides with lithium carbonate prices hovering just above $10,000/ton (CIF Asia basis), putting high-cost producers under pressure. Some companies, like Mt Cattlin, are already planning to transition into care and maintenance by mid-2025, while others seek strategic mergers to cut costs.

Outlook for 2025 and Beyond

Lithium supply reductions are expected to shrink the market until 2027, driving a deeper deficit by 2028. Prices for 2028 are projected at $15,344 per tonne, a 4.7% increase, per S&P Global forecast.

With supply cuts narrowing the market surplus and demand from the EV industry projected to grow, lithium prices may find support in the medium term.

Ultimately, lithium prices are expected to remain volatile as demand accelerates. Amid all this, ElectraLith’s revolutionary direct lithium extraction tech could help stabilize supply chains and drive the global energy transition forward.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png2024-11-26 11:50:492024-11-26 11:50:49Rio Tinto-Backed Lithium Startup’s $18M Funding: How Can It Revolutionize the Industry?

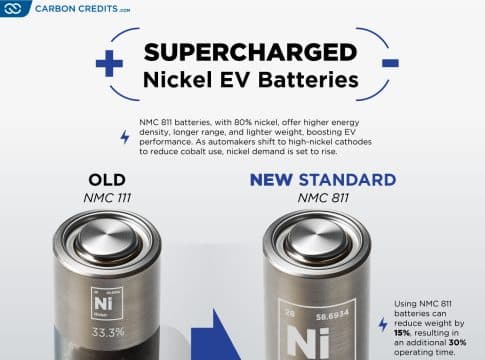

As automakers prioritize energy efficiency and sustainability, nickel-rich batteries are becoming essential in the electric vehicle (EV) market. This silvery-white metal is now one of the most coveted elements for high-performance batteries that can power the future of electric mobility.

In this nickel revolution, high-nickel cathodes, such as those in NMC 811 batteries are taking the lead. These batteries offer higher energy density, reduced weight, and extended driving ranges which are vital consumer needs.

To name a few, top EV brands like Tesla, Volkswagen, Ford, and Stellantis are betting on NMC 811 batteries. Notably, these batteries reduce reliance on cobalt- a high-risk material, making them a more sustainable and cost-effective choice for the EV industry.

The Rise of NMC 811: Old vs. New

Traditional NMC 111 batteries rely on equal parts nickel, manganese, and cobalt. In contrast, the new standard—NMC 811—packs 80% nickel, cutting cobalt and manganese usage to just 10% each. This shift brings some powerful benefits to the new generation batteries:

15% weight reduction

30% longer battery life

Improved energy density and range

These upgrades not only enhance EV performance but also align with sustainability goals by reducing dependency on cobalt.

So, What Sets NMC 811 Batteries Apart?

The latest generation of NMC 811 batteries differs significantly from earlier versions, thanks to advancements in their composition.

Increased Nickel Content: The 8:1:1 ratio in NMC 811 refers to a higher proportion of nickel compared to cobalt and manganese. This shift enhances energy density, allowing EVs to travel farther on a single charge.

Cobalt Reduction: By minimizing cobalt content, these batteries reduce supply chain risks and improve affordability without sacrificing performance.

Lighter and More Efficient: Lightweight and longer battery life make them energy efficient for EVs, thereby contributing to better overall performance and lower energy consumption.

The Future of Nickel: Surge in Demand with Battery Innovation

We have seen and read earlier that battery nickel demand has faced challenges in 2024 mainly due to weak EV sales in Western markets. However, despite these short-term setbacks, the long-term outlook for nickel appears highly promising. Projections suggest that demand for battery-grade nickel will grow by 27% year-on-year in 2024, highlighting its critical role in the EV revolution.

According to the Benchmark Nickel Forecast, batteries will drive over 50% of nickel demand growth by 2030, with consumption expected to reach 1.5 million tons by the decade’s end.

This growth reflects the increasing reliance on nickel-based chemistries, which are expected to dominate sustainable battery manufacturing. The Benchmark analysis also shows that such prototypes will account for 85% of battery cell production capacity outside China by 2030.

Thus, it seems inevitable that high-nickel chemistries, precisely the NMC 811 batteries will be the key driver for nickel demand and represent a significant breakthrough in the EV industry.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: AEMC.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png2024-11-25 15:01:572024-11-25 15:01:57Powering the Future of Nickel with NMC 811 Batteries