Crypto Market Tops $3 Trillion Amid ‘Trump Bump’, Bitcoin Hits All-Time High at $93K

The global cryptocurrency market has surpassed $3 trillion, fueled by renewed investor optimism following Donald Trump’s re-election as U.S. President. Alongside this, Bitcoin has reached an all-time high at $93,434.

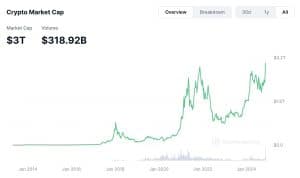

According to CoinMarketCap, the total market cap currently sits at $3 trillion, up 4% in the past day. CoinGecko reports an even higher figure of $3.15 trillion, tracking over 15,000 cryptocurrencies, compared to CoinMarketCap’s 10,000.

The $3T Surge: What’s Driving the Crypto Boom?

This milestone marks an all-time high, surpassing the 2021 bull run. The surge, dubbed the ‘Trump Bump,’ reflects expectations of a pro-crypto regulatory environment under the new administration.

Trump’s campaign promises, including making the U.S. a global crypto hub and establishing a national Bitcoin reserve, have strengthened market confidence.

Institutional appetite for digital assets continues to grow. A recent survey of 400 global institutional investors revealed that 57% plan to increase their crypto allocations, with many aiming to do so within the next 6 months.

Companies like MicroStrategy have also made significant investments, recently acquiring $2 billion in Bitcoin.

Analysts predict further growth but caution against potential corrections, citing external risks like weak U.S. economic data.

Bitcoin’s Record-Breaking Rally: Is $100K Next?

Bitcoin has been a key driver of this crypto rally, hitting a new all-time high (ATH) of $93,434 on November 13. Its market cap now stands at almost $1.8 trillion, comprising 60% of the total crypto market.

Altcoins are also experiencing significant gains, contributing to the broader market’s upward momentum.

Maksym Sakharov, CEO of DeFi platform WeFi, attributes the surge to “Bitcoin’s price rally above $93,000, growing demand, and regulatory clarity.” Bitcoin has more than doubled in 2024, fueled by the launch of spot Bitcoin ETFs and increased institutional interest.

Many crypto analysts suggest Bitcoin’s rally is far from over. Some predict it could hit $100,000 in the coming months.

Galaxy Digital CEO Mike Novogratz offers an even bolder outlook, forecasting a potential surge to $500,000—if Bitcoin gains traction as a national reserve asset in the U.S.

Bitcoin Surpasses Silver, Becomes World’s 8th Largest Asset

Even more remarkable, Bitcoin has reached a new milestone. It surpassed silver with a market cap of $1.8 trillion, positioning itself as the world’s 8th largest asset. This marks a significant leap in Bitcoin’s trajectory, as it now trails only major players like gold, Apple, and Microsoft, according to Companies Market Cap.

The surge comes as Bitcoin’s price hit over $93,000, with even more bullish projections ahead. In contrast, silver fell by 2%, helping Bitcoin secure its spot ahead of the precious metal.

Institutional Momentum Drives Bitcoin’s Rise

Institutional activity played a crucial role in today’s rally. BlackRock’s iShares Bitcoin Trust (IBIT) recorded $4.5 billion in trading volume, reflecting the growing interest in Bitcoin from major financial players.

Bloomberg’s Eric Balchunas highlighted this trend, noting that Bitcoin ETFs and related assets, including MicroStrategy and Coinbase, reached a combined trading volume of $38 billion.

Optimism in the crypto market has surged following Donald Trump’s re-election, with analysts suggesting his pro-crypto stance could pave the way for favorable regulations. This sentiment has fueled predictions that Bitcoin could surpass the $100,000 mark by the end of 2024.

However, behind all this hype with the crypto industry, particularly Bitcoin’s sudden surge, lurks the digital asset’s environmental impact.

Crypto’s Environmental Toll: Balancing Growth and Sustainability

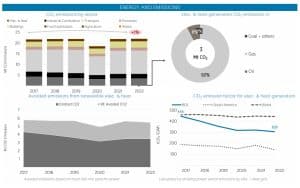

The rising energy consumption of crypto mining has sparked global concern due to its environmental impact. The White House’s 2022 report highlighted the substantial electricity demands of cryptocurrency mining, which now rival the energy consumption of countries like Poland.

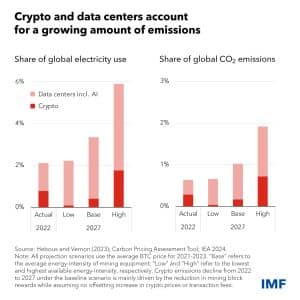

In an analysis by the International Monetary Fund (IMF), crypto mining and data centers made up 2% of global electricity demand in 2022. This figure could rise to 3.5% within three years, matching Japan’s current electricity usage—the fifth highest in the world—according to projections from the International Energy Agency.

- Bitcoin’s proof-of-work (PoW) consensus mechanism is a primary contributor, with global electricity use for PoW estimated between 97 and 323 terawatt-hours annually. This translates to significant greenhouse gas emissions, with Bitcoin alone responsible for around 88 million metric tons of CO₂ each year.

The U.S. accounts for nearly 46% of Bitcoin mining emissions, releasing about 15.1 million metric tons of CO₂ annually. Other major contributors include China and Kazakhstan, emphasizing the global nature of the issue.

The mining process also has indirect environmental impacts, such as electronic waste and water usage, with one Bitcoin transaction consuming thousands of gallons of water.

Efforts to reduce Bitcoin’s carbon footprint include transitioning to less energy-intensive consensus mechanisms like proof-of-stake (PoS) and adopting renewable energy sources for mining.

However, regional emission reduction efforts often fall short due to the global supply chain’s carbon intensity. For instance, even countries with cleaner energy grids, like Norway, face indirect emissions from imported mining equipment manufactured in coal-reliant regions like China.

Interestingly, recent studies challenge the perception of Bitcoin mining’s environmental impact.

Bitcoin Mining’s Role in Carbon Reduction

Research from the Bitcoin Policy Institute (BPI) highlights how mining increasingly relies on renewable energy, turning surplus energy into a valuable resource. By using excess power from renewable sources like wind and solar, mining helps stabilize grids and reduce energy waste, proving that it can contribute to carbon reduction rather than exacerbating emissions.

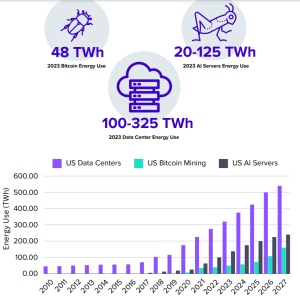

The researchers also compared the energy use of Bitcoin mining, data centers, and AI server energy in the U.S. in 2023. Bitcoin used 48 TWh in 2023, while AI servers consumed between 20 and 125 TWh. On the other hand, data centers have the biggest power consumption, ranging from 100 to 325 TWh.

The following chart shows the historical results and forecasts up to 2027.

Another report from the Digital Assets Research Institute (DA-RI) reveals flaws in past research on Bitcoin’s energy use. It critiques outdated models that overlooked miners’ shift to renewable energy, resulting in sensational headlines and misinformed policies.

The new findings urge regulators to base decisions on empirical data, underscoring Bitcoin’s potential to align with global carbon reduction goals.

These studies suggest that sustainable Bitcoin mining could play a crucial role in green initiatives. By leveraging clean energy, mining could evolve into a climate-friendly industry, offering both economic and environmental benefits. As this perspective gains traction, policymakers may adopt more balanced regulations, supporting sustainable growth in the crypto sector.

The post Crypto Market Tops $3 Trillion Amid ‘Trump Bump’, Bitcoin Hits All-Time High at $93K appeared first on Carbon Credits.

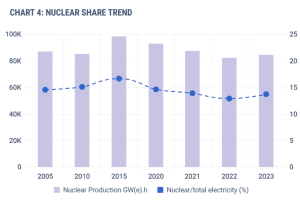

Source: IAEA

Source: IAEA

Natural Capital Monetization (NCM) platform to facilitate technology transfer and bolster

Natural Capital Monetization (NCM) platform to facilitate technology transfer and bolster