Top 4 Carbon Removal Stocks Set to Suck Up and Cash In

More companies and governments are investing in carbon removal technologies to help them reach net-zero emissions. With stricter climate rules and companies feeling pressure to reduce carbon footprints, carbon removal stocks are becoming appealing investment options.

Why Carbon Removal Stocks Are Gaining Traction in 2025

Carbon removal companies work to take carbon dioxide (CO₂) from the air. They either store it for good or change it into useful products.

Carbon removal is different from carbon offset initiatives. While offsets balance emissions by reducing them elsewhere, carbon removal actively eliminates CO₂. This makes it essential for industries that struggle to cut emissions.

The carbon removal sector could grow quickly in the next few years. More policymakers, companies, and investors are showing support to scale up the industry. In 2025, here are the top four carbon removal stocks worth watching and keeping on your radar. Let’s break down each one of them, what technology they’re innovating, and other major initiatives.

1. Net Power Inc. (NYSE: NPWR): Innovating Zero-Emissions Energy

Net Power Inc. is a U.S.-based clean energy technology company founded in 2010, specializing in generating reliable, on-demand electricity from natural gas with near-zero emissions. The company is revolutionizing the energy sector with its proprietary Allam Cycle technology.

It generates electricity from natural gas while capturing and storing CO₂ emissions. Furthermore, it can capture around 97% of CO₂ emissions during the process. This innovative approach also virtually eliminates other pollutants, including nitrogen oxides (NOₓ) and sulfur oxides (SOₓ).

Net Power’s modular plant design occupies about 15 acres per facility and offers scalability from 250 megawatts (MW) up to 2 gigawatts (GW). The company is aiming to deploy its first utility-scale power plant by 2028.

Unlike traditional natural gas plants, Net Power’s system prevents emissions from reaching the atmosphere, offering a potential breakthrough for clean energy production.

Operational Developments:

-

La Porte Demonstration Facility: The company completed major plant upgrades and initiated the first phase of the equipment validation program with Baker Hughes.

-

Project Permian: Located near Midland-Odessa, Texas, this is Net Power’s first utility-scale project. Front-End Engineering and Design (FEED) work continued with Zachry Group and was on track to conclude in Q4 2024. The project aims for initial power generation between the second half of 2027 and the first half of 2028.

-

Air Separation Unit (ASU) Partnership: Net Power announced Air Liquide as the ASU supplier for Project Permian, integrating this component into the overall plant design.

Strategic Initiatives:

Net Power has improved site evaluations for new projects in North America. This includes locations in Alberta, Canada, and several sites in the U.S. These efforts involve collaborations with natural gas producers, carbon sequestration providers, and data center developers.

The company signed a Limited Notice to Proceed (LNTP) with Baker Hughes. This deal is worth about $90 million. It covers the purchase of long-lead materials for the turboexpander and important equipment for the first utility-scale power plant.

These developments underscore Net Power’s commitment to advancing its clean energy technology. It is also expanding its project portfolio despite financial challenges.

2. Shell Plc (NYSE: SHEL): Leading in Carbon Capture Initiatives

Shell Plc, a global energy conglomerate, is making significant strides in carbon removal to align with its net-zero emissions targets. The company has pledged to reduce absolute emissions by 50% by 2030 compared to 2016 levels. Carbon removal, particularly carbon capture and storage (CCS), plays a critical role in achieving this goal.

CCS captures carbon dioxide (CO₂) from industrial processes. It stores the gas underground to stop it from entering the atmosphere.

Shell’s Major CCS Initiatives:

-

Quest Project (Canada): Since 2015, the Quest facility at Shell’s Scotford complex in Alberta has captured and stored over 8.8 million tonnes of CO₂. Shell is moving forward with the Polaris CCS project at Scotford. This project aims to capture about 750,000 tonnes of CO₂ each year. It will cut emissions from the refinery by up to 40% and from the chemicals complex by 22%.

-

Northern Lights Project (Norway): In collaboration with Equinor and TotalEnergies, Shell is investing $714 million to expand the Northern Lights carbon storage facility. This expansion will boost CO₂ injection capacity from 1.5 million to over 5 million tonnes each year. It will tackle nearly 10% of Norway’s annual emissions.

-

Gorgon Project (Australia): As a partner in the Gorgon CCS project operated by Chevron, Shell contributes to one of the world’s largest CCS operations. By December 2023, the project had stored more than 10 million tonnes of CO₂.

-

Daya Bay CCS Hub (China): Shell, along with ExxonMobil and CNOOC, is exploring the development of a large-scale CCS hub in Guangdong Province. The proposed facility aims to capture up to 10 million tonnes of CO₂ annually, supporting China’s goal of carbon neutrality by 2060.

These initiatives reflect Shell’s commitment to deploying CCS technologies globally. It works with industry partners and governments to mitigate carbon emissions and support the transition to a low-carbon energy future.

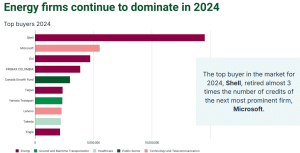

Carbon Credit Market Leadership

Shell showed its commitment to cutting emissions by retiring 14.5 million carbon credits in 2024. Most of these credits backed forestry and land-use projects that aim to protect current carbon stores.

The company has invested in nature-based solutions. These include reforestation and wetland restoration, which both help enhance carbon sequestration.

3. Delta CleanTech Inc. (CSE: DELT): Specializing in Carbon Capture Solutions

Delta CleanTech Inc., established in 2004 and headquartered in Calgary, Alberta, focuses on clean energy technology. The company specializes in carbon capture, utilization, and storage (CCUS). It also works on solvent and glycol reclamation, as well as carbon credit validation and management.

- Note: The company has changed its name to Regenera Insights.

Key Business Areas

-

CO₂ Capture Technology: Delta provides CO₂ capture solutions using its LCDesign® technology. This technology is scalable for facilities that manage 1 to 1,000 tonnes of CO₂ daily.

-

Solvent and Glycol Reclamation: Through its subsidiary, PurificationRX, Delta provides solvent purification technologies aimed at reducing emissions and promoting material reuse.

-

Carbon Credit Services: Carbon RX, a subsidiary, focuses on carbon credits. It originates, validates, and streams these credits. The company is expanding from agriculture to many industries that capture and reduce carbon.

Strategic Initiatives and Partnership

4. Mitsubishi Corporation (TYO: 8058): Advancing Global Carbon Capture Initiatives

Mitsubishi Corporation is working on big carbon capture and storage projects around the world. The company has set a target of achieving net-zero emissions across its global operations by 2050, with CCS playing a key role in this strategy.

Strategic Partnerships and Initiatives:

In January 2023, MC signed a Memorandum of Understanding with Nippon Steel Corporation and ExxonMobil Asia Pacific to study and establish CCS value chains in the Asia-Pacific region. This collaboration aims to capture CO₂ emissions from Nippon Steel’s steelworks in Japan. It also evaluates the infrastructure needed for storage in Malaysia, Indonesia, and Australia.

In March 2024, MC teamed up with ENEOS Corporation, JX Nippon Oil & Gas Exploration, and PETRONAS CCS Solutions. They will explore the feasibility of a CCS value chain from Tokyo Bay to Malaysia.

The project plans to capture around 3 million tonnes of CO₂ each year from industries in Tokyo Bay. It could expand to 6 million tonnes annually, with the goal of starting operations by 2030.

Carbon Credit Initiatives:

-

NextGen CDR AG: MC teamed up with South Pole to create NextGen CDR AG. This company buys and sells carbon credits from carbon removal technologies, such as CCUS. This initiative will help implement these technologies on a large scale. It does this by creating new revenue streams through credit sales.

-

Australian Integrated Carbon Investment: MC and Nippon Yusen Kabushiki Kaisha (NYK) bought a 40% stake in Australian Integrated Carbon (AIC). AIC aims to capture CO₂ by regenerating Australia’s native forests. The goal is to sequester up to 5 million tonnes of CO₂ each year. By 2050, the total target is 100 million tonnes.

Through these strategic partnerships and investments, Mitsubishi Corporation shows a strong commitment to advancing carbon capture, storage, and removal technologies. All these help contribute to global decarbonization efforts and the realization of a low-carbon economy.

Conclusion

Investing in companies dedicated to carbon removal and capture, such as Net Power, Shell, Delta CleanTech, and Mitsubishi Corporation, offers potential for financial returns while supporting the transition to a low-carbon economy. These companies lead in creating and using key technologies to meet global climate goals.

What more, the carbon removal sector is expected to grow significantly in the coming decades. This growth is driven by increasing regulatory support, corporate net-zero commitments, and advances in technology.

As countries around the world tighten emissions rules, the need for carbon removal and direct air capture solutions will likely grow. This trend could set these carbon removal companies up for long-term success. Investors looking to join the clean energy shift will find these carbon removal stocks as great chances to be part of the next wave of climate innovation.

The post Top 4 Carbon Removal Stocks Set to Suck Up and Cash In appeared first on Carbon Credits.