Tesla Q1 2026 Hits $22.38B Revenue – But Do Weak Deliveries and Falling Credits Expose a Fragile Growth?

Tesla (TSLA) reported a mixed performance in the first quarter of 2026 (Q1 2026. The company beat earnings expectations and delivered stronger margins, but several underlying trends pointed to weakening demand signals and rising execution pressure across key segments.

Earnings Beat, But Growth Is Not Fully Organic

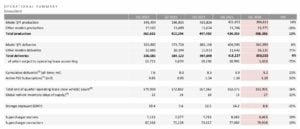

Tesla posted revenue of $22.38 billion, slightly ahead of Wall Street expectations of $22.3 billion. Earnings came in at $0.41 per share (non-GAAP), above the expected $0.37. This marked a clear improvement from Q1 2025, when the company reported weaker results. Revenue grew about 14% year over year, while earnings rose roughly 33%.

However, the quality of earnings raised questions. Tesla itself highlighted that part of the profit improvement came from one-time benefits tied to warranties and tariffs. These are not recurring revenue sources. As a result, the headline beat does not fully reflect the underlying operating strength.

Margins Improve, But Vehicle Demand Weakens

One of the strongest positives in the quarter was profitability. Tesla’s gross margin rose to 21.1%, compared to 16.3% a year ago and 20.1% in the previous quarter. This was one of the best margin performances in recent periods and showed better cost control and pricing stability.

But the demand picture told a different story.

Tesla delivered 358,023 vehicles, falling short of expectations by around 7,600 units. At the same time, production exceeded deliveries by more than 50,000 vehicles. This created a noticeable inventory buildup.

This gap matters because it suggests supply is running ahead of demand. If this continues, Tesla may face pricing pressure, higher discounts, or slower production adjustments in future quarters. In simple terms, the company is producing more cars than the market is absorbing right now.

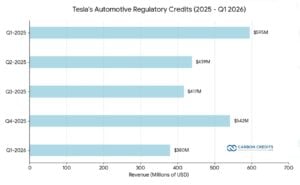

Regulatory Credit Revenue Slides 30%

Another weak point was the sharp decline in regulatory credit revenue. Tesla generated about $380 million in Q1 2026, down from $542 million in Q4 2025, a drop of nearly 30% in just one quarter.

These credits have historically been one of its highest-margin income streams. The company earns them by producing zero-emission vehicles and selling surplus credits to other automakers that fail to meet emissions requirements.

The decline in credit revenue reflects a structural change in the EV market. More automakers are now producing electric vehicles, and emissions rules are evolving. This reduces demand for Tesla’s credits over time. As a result, Tesla is becoming less dependent on this high-margin but unpredictable revenue stream.

Energy Storage Weakens Despite Long-Term Potential

Tesla’s energy business also showed softness in Q1. Energy storage deployments fell to 8.8 GWh, down 38% from the previous quarter. This was significantly below analyst expectations and marked a slowdown in momentum for a key growth area.

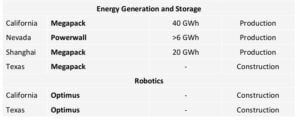

Even so, Tesla continues to invest heavily in energy. The company is expanding its Megafactory near Houston, which will produce next-generation Megapack systems. Production is expected to begin later this year, and the facility is central to Tesla’s long-term energy strategy.

The company also began rolling out its new in-house solar panels. These panels are designed to perform better in low-light conditions and offer faster installation. While early in deployment, Tesla sees energy products as a long-term growth engine that can complement its vehicle business.

Autonomy, AI, and Robotics Define the Long-Term Vision

Tesla continues to shift its focus toward advanced technologies, particularly autonomy, artificial intelligence, and robotics.

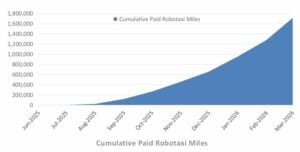

- In the Robotaxi program, paid miles nearly doubled compared to the previous quarter. It is expanding testing and regulatory groundwork across multiple U.S. cities, including Austin, Dallas, and Houston. The company is preparing for a broader rollout and expects its upcoming Cybercab to eventually become a core fleet vehicle.

- In robotics, Tesla is accelerating work on its Optimus humanoid robot. The company plans to build a dedicated large-scale production facility. The first phase targets a capacity of up to one million robots per year, with long-term expansion plans reaching significantly higher volumes.

- In artificial intelligence, the company is moving toward semiconductor development. It is working with SpaceX to develop chip manufacturing capabilities. The goal is to build a vertically integrated system covering chip design, fabrication, and packaging.

Tesla has already completed the design of its next-generation AI5 inference chip, which will support future autonomy and robotics workloads. This step is important because chip demand is expected to rise sharply as Robotaxi and Optimus scale.

FSD Numbers Remain Unclear

Tesla reported 1.28 million Full Self-Driving (FSD) users, but the figure includes both subscription users and customers who purchased the package outright. This makes it difficult to understand actual subscription growth.

The company has also pushed more customers toward subscription-based access in recent quarters. While this may improve recurring revenue over time, the current reporting structure makes trends harder to track clearly.

PG&E and Tesla’s Vehicle-to-Grid Push Expands Energy Role

A notable development this quarter came from Tesla’s partnership with Pacific Gas and Electric Company. Tesla’s Cybertruck and energy products are now part of PG&E’s Vehicle-to-Everything (V2X) program.

This system allows electric vehicles to send power back to homes or the grid. During outages, vehicles can act as backup power sources. During peak demand, they can export electricity to stabilize the grid and earn compensation.

Additionally,

- Customers participating in the program can receive up to $4,500 in incentives, along with additional payments for participating in grid events.

- The system uses AC-based bidirectional charging, which reduces complexity compared to traditional DC systems.

This development is important because it expands the role of electric vehicles beyond transportation. EVs are increasingly becoming distributed energy assets that support grid stability, especially in high-adoption markets like California.

Is Musk Balancing Two Futures?

Tesla’s Q1 2026 results show a company moving through a transition phase. On one side, profitability is improving, and margins are strong. On the other hand, demand signals are weakening in key areas such as vehicle deliveries, energy storage, and regulatory credit revenue.

At the same time, it is investing aggressively in long-term technologies like autonomy, robotics, and AI infrastructure. These areas could define the company’s future growth, but they remain early-stage and execution-heavy.

The key challenge ahead is balance. Tesla must manage short-term operational pressure while scaling long-term bets that are still under development. The direction is clear, but the path forward will depend heavily on execution in the coming quarters.

The post Tesla Q1 2026 Hits $22.38B Revenue – But Do Weak Deliveries and Falling Credits Expose a Fragile Growth? appeared first on Carbon Credits.