CATL Secures $5 Billion Hong Kong Capital Raise for EV Battery Production Expansion

Contemporary Amperex Technology Co. Limited (CATL), the world’s largest electric vehicle (EV) battery maker, has raised about $5 billion through a major share placement in Hong Kong. The deal strengthens the company’s global expansion plans and highlights growing investor confidence in clean energy and battery technologies.

CATL sold 62.385 million new H shares at HK$628.20 each, raising HK$39.2 billion ($5 billion). The placement is the largest equity offering in Hong Kong so far this year and one of the biggest globally in 2026.

Global demand for EV batteries, energy storage, and low-carbon tech is rapidly increasing. Governments are tightening emissions rules. Automakers are ramping up EV production. Energy companies are also investing heavily in battery storage. All these support renewable energy grids.

CATL Pulls Off One of 2026’s Biggest Global Fundraises

The offering drew great interest from institutional investors, even though it was priced at the lower end of CATL’s range. The shares were sold at a 7% discount to the company’s previous closing price of HK$675.50. Investors reportedly subscribed to the entire allocation within about an hour of launch.

More than 150 institutional investors joined the placement, including hedge funds and long-term asset managers. Analysts said the deal benefited from strong market interest in clean energy stocks as the Iran war drives up oil prices and ramps up the global shift away from fossil fuels.

CATL’s shares in Hong Kong have jumped about 137% to 157% since their secondary listing in May 2025. At that time, the company raised around $4.6 billion, making it the largest IPO in the world that year. Its Shenzhen-listed shares are also up more than 16% this year, giving the company a market value approaching $294 billion.

The latest fundraising also reflects broader momentum in Hong Kong’s capital markets. KPMG reports that Hong Kong IPOs raised nearly HK$110 billion in Q1 2026. PwC expects total fundraising this year to hit HK$320 billion to HK$350 billion.

Notably, CATL’s share price declined nearly 7% following the discounted equity placement announcement.

The Battery Giant Powering the Global EV Revolution

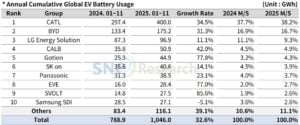

CATL remains the largest EV battery manufacturer in the world by market share. According to South Korean research firm SNE Research, the company controlled about 38% to 40% of the global EV battery market during 2025.

Global EV battery installations reached around 1,187 gigawatt-hours (GWh) in 2025, up 31.7% from 901.4 GWh the previous year. CATL alone accounted for roughly 464.7 GWh of installed battery capacity. That means nearly 4 out of every 10 EV batteries installed globally came from CATL.

The company provides batteries to major automakers worldwide. This includes Tesla, BMW, Mercedes-Benz, and Volkswagen. It also supplies Chinese EV makers like Li Auto, Xiaomi, and Geely Auto.

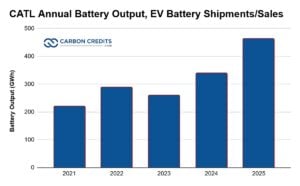

CATL’s battery output has grown rapidly from roughly ~220 GWh in 2021 to about 465 GWh in 2025, more than doubling in four years. This steady increase shows that global EV adoption is speeding up. Automakers are demanding more, and CATL is expanding its manufacturing capacity. This growth strengthens CATL’s leading role in the global EV battery market.

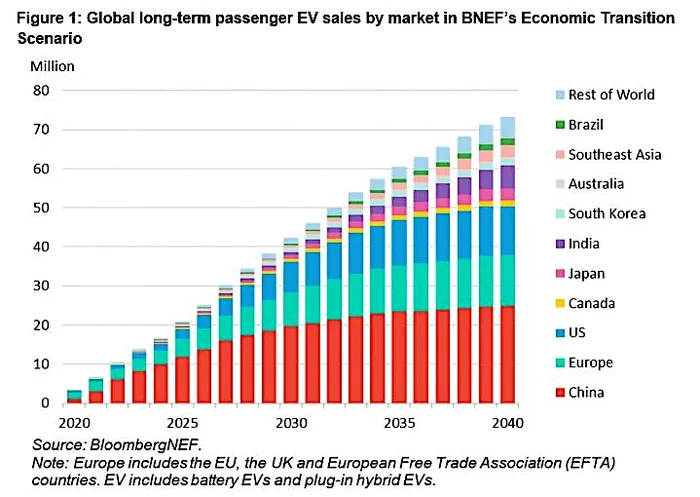

Demand for EV batteries is expected to remain strong over the next decade. The International Energy Agency (IEA) predicts that global EV sales may reach over 45 million vehicles each year by 2030 if current policies stay the same. This would more than double current levels. It would greatly boost the demand for battery manufacturing capacity.

This projection is echoed by BNEF’s estimates, as shown below.

At the same time, battery energy storage systems are becoming a major growth market. BloombergNEF expects global battery storage to grow over six times by 2035. Meanwhile, countries are focusing on renewable energy and upgrading their power grids.

CATL Expands Manufacturing Across Europe and Asia

CATL said the proceeds from the placement will support:

- overseas manufacturing expansion,

- supply chain development,

- research and development,

- zero-carbon initiatives, and

- general corporate operations.

Most of the funding will support the company’s €7.3 billion battery plant in Hungary. This plant is one of the largest battery projects in Europe. The facility is expected to supply major European automakers and strengthen CATL’s position in the region.

The company is also expanding operations in Germany, Indonesia, and Spain. CATL and Stellantis are jointly building a battery factory in Spain that is expected to begin production by the end of 2026.

These investments reflect a broader industry trend toward regionalized battery production. Automakers want local supply chains. This helps cut logistics costs, boosts energy security, and meets tougher carbon reporting rules.

China still dominates the global battery supply chain. China makes over 75% of the world’s lithium-ion batteries, according to the IEA. It also processes a significant amount of key minerals like lithium, cobalt, and graphite.

Zero-Carbon Factories and Recycling Become Strategic Priorities

CATL is investing a lot in lower-carbon manufacturing and battery recycling. This comes as global sustainability standards get stricter.

The company is pushing for “zero-carbon factories.” These factories will use more renewable electricity, improve energy efficiency, and reduce emissions. These efforts align with China’s broader carbon neutrality goal of reaching net-zero emissions by 2060.

Battery production can generate significant emissions because it requires large amounts of energy and raw materials. Research from the International Council on Clean Transportation (ICCT) shows that battery manufacturing can make up over 40% of an EV’s total production emissions. This depends on the electricity mix used during manufacturing.

To address this issue, CATL is expanding battery recycling operations and investing in cleaner production systems. Recycling recovers key minerals like lithium, nickel, and cobalt. It also cuts down on the need for new mining.

The company has also developed sodium-ion battery technology, which could reduce long-term dependence on lithium and improve supply chain resilience. CATL has formed a strategic partnership with Beijing HyperStrong Technology. This deal involves 60 GWh of sodium-ion battery cooperation over the next three years.

Why CATL Is Becoming Critical to the Global Energy Transition

CATL’s rapid expansion reflects the growing role batteries play in the global energy transition. Batteries are critical for:

- electric transportation,

- renewable energy storage,

- grid stability, and

- emissions reduction.

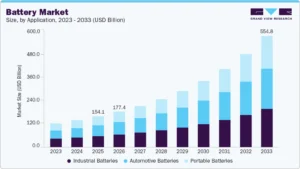

As countries work toward climate targets, demand for large-scale battery manufacturing is expected to rise sharply. The global battery market might surpass $400 billion each year by the early 2030s, based on several industry forecasts.

Governments in Europe, the United States, and Asia are now enforcing stricter rules. These rules focus on battery emissions, recycling, and supply chain transparency. Companies that can make batteries at scale and reduce carbon intensity might gain a big edge.

CATL’s new fundraising boosts its resources. This helps the company expand capacity, invest in cleaner technologies, and grow its global presence. All this comes during a time of fast market growth.

Batteries Are Now the Backbone of the Clean Energy Economy

CATL’s $5 billion share placement in Hong Kong shows that investors believe in the future of EVs, battery storage, and clean energy.

The company already controls more than 40% of the global EV battery market and continues to expand across Europe and Asia. Its investments in zero-carbon factories, recycling systems, and next-gen batteries help it adapt to stricter environmental rules and the growing demand for lower-emission supply chains.

As the global shift toward electrification accelerates, CATL is emerging as one of the most influential companies shaping the future of transportation and energy storage worldwide.

- FURTHER READING: CATL’s Profit Surges 42% With Global Battery Demand and the Shift to a Zero-Carbon Future

The post CATL Secures $5 Billion Hong Kong Capital Raise for EV Battery Production Expansion appeared first on Carbon Credits.