Google, Meta and McKinsey Lead Carbon Removal Boom and Turn Appalachia Green

Google, Meta, and McKinsey & Company have made a major move in corporate climate action. They signed a long-term deal to remove carbon from the air in Appalachia. The project is run by Living Carbon and focuses on restoring forests on degraded lands. Under this deal, the companies will remove 131,240 tonnes of CO₂ over the next ten years.

A New Deal for Climate

The effort targets a much larger problem. Across the United States, about 1.6 million acres of abandoned mine land remain damaged by past mining. These lands often have poor soil, erosion, toxic metals, and invasive species that block natural regrowth.

In addition, around 30 million acres of degraded agricultural land could be restored through reforestation. Appalachia is one of the hardest-hit regions due to decades of coal mining.

The deal is backed by the Symbiosis Coalition, a group of buyers that funds high-quality carbon removal projects. The coalition is an advance market commitment (AMC) launched in 2024 by Google, Meta, Microsoft, and Salesforce.

The group has pledged to contract up to 20 million tonnes of carbon removal credits by 2030. This commitment aims to create strong market demand and support the growth of high-impact, science-based restoration projects that can help advance global climate goals.

The agreements they have give developers a steady demand. They also help unlock financing and allow projects to scale.

Symbiosis selected the Appalachian project after a strict review process. It looked at data, field conditions, and long-term risks. The group follows key standards such as durability, transparency, ecological integrity, and community impact. This helps ensure that every credit represents real and measurable carbon removal.

Julia Strong, Executive Director of the Symbiosis Coalition, remarked:

“Our support of Living Carbon reflects our belief that effective nature-based carbon removal requires both strong science and solid execution. Their project stands out for its rigor and for its thoughtful and scalable approach shaped around the needs of local communities, ecosystems, and economies in Appalachia.”

Why Appalachia Matters: From Coal Hubs to Carbon Heroes

The Appalachia region, in the eastern United States, was once a center of coal mining. Today, many of these lands remain unused and degraded. Living Carbon is working to restore them by planting native hardwood and pine trees on former mine sites and damaged farmland.

The project uses a mix of careful site preparation, invasive species control, and strategic planting. This helps trees grow in areas where nature cannot easily recover on its own. The goal is not just to plant trees, but to rebuild entire ecosystems and support long-term carbon storage.

The benefits go beyond carbon removal. Restoring forests improves soil health, water quality, and biodiversity. Native trees help rebuild habitats for local plants and wildlife. These changes can also reduce erosion and improve land stability over time.

The project also creates real economic value. Landowners earn lease payments from land that was once unproductive. Local workers are hired for planting and land restoration.

-

In some cases, old mining equipment is reused to support ecological recovery. This helps turn former industrial sites into productive carbon sinks.

Community engagement is a key part of the project. Living Carbon works closely with landowners, local groups, and government agencies. This helps build long-term support and ensures the project fits local needs. Strong local partnerships also improve the chances that the forests will be maintained over time.

The project stands out for its strong science and clear execution plan. It uses careful monitoring and conservative estimates to ensure carbon removal is real. It also applies new methods for tracking results, including advanced baselines and lifecycle analysis.

This type of approach shows that high-quality nature-based carbon removal can deliver more than climate impact. It can restore ecosystems, support local economies, and scale across similar regions. In places like Appalachia, it offers a way to turn damaged land into a long-term climate solution.

Big Business Bets on Carbon Credits

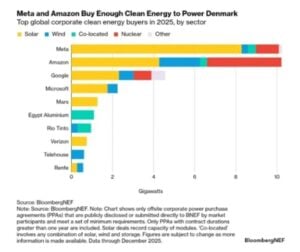

More corporations are now buying carbon removal credits to meet climate goals. For example, Microsoft bought 45 million tonnes of carbon removal in fiscal year 2025. This is nearly double the amount from 2024 and nine times what they bought in 2023.

These purchases are part of a broader climate strategy. Companies are combining emissions reductions with long-term removal commitments. Durable carbon removal credits, which permanently store CO₂, are becoming more important. Businesses feel pressure to deal with emissions that they cannot completely eliminate.

A major supporter of these deals is Frontier, launched in 2022 by Stripe, Alphabet (Google’s parent company), Meta, Shopify, and McKinsey Sustainability. Frontier wants to boost early demand and funding for promising carbon removal technologies.

The company does this through long-term purchase agreements. Its initial goal was $1 billion in purchases by 2030, sending a strong signal to the market about future demand.

By 2025, Frontier signed contracts for various technologies. These include bioenergy with carbon capture and storage (BECCS), direct air capture (DAC), and enhanced weathering. Several contracts are worth tens of millions of dollars. These agreements help developers survive the early “valley of death,” when financing is hardest to secure.

Market Trends: From Niche to Necessity

The carbon removal market is still small compared with global climate goals, but it is evolving quickly. Industry forecasts say that demand for durable carbon removal credits might hit 100 million tonnes of CO₂ each year by 2030.

This growth is fueled by corporate commitments and government purchases. This is roughly double the supply currently announced, showing a large gap between demand and delivery.

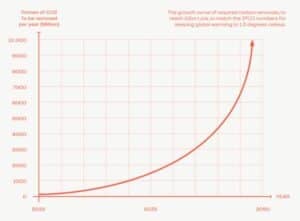

Globally, carbon removal is still a tiny fraction of what is needed. Scientific assessments show that to meet the Paris Agreement, carbon removal needs to increase. By 2050, it should reach 7–9 billion tonnes of CO₂ each year. This is about 4,000 times more than what we do now.

Market projections show strong growth in the next decade. A report by Oliver Wyman and the UK Carbon Markets Forum estimates that the global carbon removal market could grow from $2.7 billion in 2023 to $100 billion per year by 2030–2035, provided policies and standards evolve to support it.

Local and Global Wins

The Appalachia project highlights how carbon removal can benefit both the climate and communities. Restoring degraded lands improves water filtration, soil health, and wildlife habitats. Communities also gain jobs and income through forest management.

Nature-based projects, including reforestation and forest management, currently dominate removal activity. However, they do not offer the same permanence as engineered removals like BECCS or DAC, which store carbon for centuries or longer. Still, both approaches are necessary to scale the carbon removal market.

From Milestones to Market Momentum

The Google, Meta, and McKinsey deal is a milestone for corporate climate action. Long-term agreements help projects secure funding and expand. They also send strong signals to developers and investors. These deals can shift the market from short-term offsets to long-term, permanent carbon removal solutions.

The industry must grow significantly to meet global climate targets. Expanding beyond early adopter companies is essential. Continued policy support, strong standards, and wider sector participation will help scale removals.

In the next decade, how fast carbon removal technologies grow and the amount of credits produced will be key to achieving net-zero goals. Deals like the Appalachia reforestation project are early steps in building a foundational, long-term carbon removal industry.

The post Google, Meta and McKinsey Lead Carbon Removal Boom and Turn Appalachia Green appeared first on Carbon Credits.