China Joins Google, Amazon, and xAI in the Race to Build AI Supercomputers in Space!

In late 2025, space is emerging as a new frontier for artificial intelligence (AI) infrastructure. What was once a futuristic concept is now becoming a realistic goal. Global tech firms and Chinese aerospace companies are racing to deploy AI data centers in orbit. Their goal is to tackle the power, cooling, and data limits that challenge Earth-based systems.

Why Space — and Why Now

AI workloads are growing at an unprecedented pace. Training and running large models need a lot of computing power. They also use a lot of energy and need advanced cooling systems.

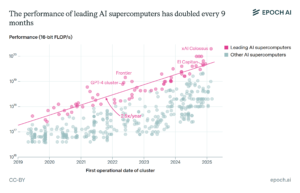

On Earth, these demands strain not only data centers but also power grids, water resources, and land availability. From 2019 to 2025, AI supercomputers saw their performance double every 9 months or 2.5x per year. In contrast, hardware costs and energy usage doubled about every year.

Space-based computing offers a promising alternative. Satellites in orbit get almost constant sunlight. This makes solar power generation more efficient than solar farms on the ground.

The vacuum of space also allows heat to dissipate naturally. This reduces the need for energy-intensive cooling systems.

Orbital “edge computing” allows engineers to process a lot of data right in space, including data from Earth observation satellites. This approach avoids the bandwidth limits and delays that occur when transferring vast amounts of raw data to Earth.

Experts view 2025–2027 as a key turning point. During this time, tech advances, costs, and goals will align.

Who’s Doing It: Rivals in Orbit

Chinese companies are taking the lead in deployment. Zhongke Tiansuan (Comospace), founded in 2024, has operated a space computer on a Jilin‑1 satellite for over 1,000 days. Their new system, “Aurora 5000,” uses a powerful domestic GPU. It will be tested in orbit soon.

Liu Yaoqi, CEO of Zhongke, said:

“Orbital edge computing moves AI directly to the source of data filtering petabytes of daily satellite imagery and traffic before the narrow downlink chokes.”

At Zhejiang Laboratory, engineers are developing a “mini computing constellation” called the Three-Body Computing Constellation. Its first batch of 12 satellites was launched in May 2025.

Each satellite carries an 8-billion-parameter AI model and can perform around 744 trillion operations per second. Together, they form the first stage of a network that could reach 1,000 peta-operations per second if fully scaled.

China plans a central space data center in dawn–dusk orbit (700–800 km altitude) with a power capacity exceeding 1 gigawatt. The plan is phased: test satellites from 2025 to 2027, followed by a full-scale megawatt-class orbital data center by 2035. If realized, it could surpass the total capacity of China’s current terrestrial data centers.

Key technologies include high-speed laser links between satellites. These links recently showed a 400 Gbps connection. They also use advanced cooling and error-correction systems to tackle radiation and thermal challenges.

If it works, the constellation can handle data for Earth observation, maritime tracking, environmental monitoring, and disaster response. It could also support global AI services. This would not depend entirely on ground-based infrastructure.

Global Tech Giants: Orbital AI as the Next Moonshot

International tech companies are pursuing similar goals. Google’s Project Suncatcher plans solar-powered AI data centers in low Earth orbit. Each satellite would carry Tensor Processing Units (TPUs) and operate in dawn–dusk orbits for continuous sunlight.

Google anticipates launching the first test satellites by 2027. These small racks of hardware will test whether TPUs can operate reliably in orbit.

Other tech companies, including those running satellite internet constellations, are exploring space-based computing. Amazon’s “Leo” project, for example, may one day link satellites to cloud and AI infrastructure.

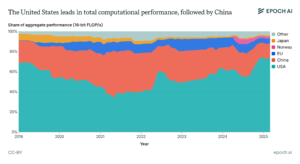

According to Epoch AI’s 2025 report on AI supercomputers, the United States accounts for about three‑quarters of total global AI supercomputer compute capacity. This dominance reflects how U.S.-based companies deploy the largest and most powerful GPU clusters.

Why the Market Is Moving to Space-Based Compute

- The shift to space-based AI reflects broader trends: increasing compute demand, rising energy costs, and sustainability concerns.

The global AI supercomputer sector is expected to grow dramatically. By 2030, top supercomputers might handle about 2 × 10²² 16-bit operations each second. They will use millions of AI chips and need gigawatts of power.

Space-based computing could ease pressure on terrestrial grids, lower carbon footprints, and reduce reliance on water for cooling. This is appealing to both technology companies and governments seeking sustainable infrastructure.

Orbital data centers are much more energy-efficient than those on Earth. They capture nearly constant solar power, being up to 10 times more effective than ground panels because there’s no atmosphere to interfere. They also use radiative cooling in space’s vacuum. This cuts cooling needs, which usually consume 40% of Earth’s data center energy, with average PUEs of 1.5 to 1.7.

- As such, it could reduce emissions by 50-80% by operating without fossil fuels. It would also ease pressure on the grid.

Currently, data centers use 4-12% of U.S. electricity, mainly from carbon-heavy sources. By 2028, this shift can make a big difference. Projects like Google’s Suncatcher target this for scalable AI without water or land impacts.

As launch costs drop, thanks to reusable rockets and mass-produced satellites, orbital data centers could compete with ground options by the mid-2030s.

A full-scale orbital network, like China’s gigawatt-class constellation, could match or exceed Earth’s mega data centers. It could offer worldwide low-latency coverage. This may change industries like Earth observation, environmental monitoring, global connectivity, autonomous logistics, and disaster response.

What’s Next: The Road to 2035 Orbital Megacenters

Key milestones to watch include:

- 2027: First test satellites from Google and other firms. Early results will show if solar-powered TPUs can operate reliably.

- 2025–2030: AI compute demand continues to rise, and electricity and water costs increase on Earth. Launch costs may drop, making space deployment more viable.

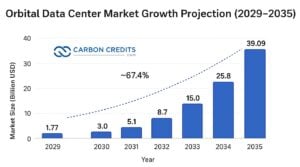

- 2030–2035: Large constellations, such as China’s gigawatt-class network, may start operating fully. This will provide global coverage and high computing power. The market could grow up to $39 billion in value.

- Governance and regulation: Nations and companies will need new rules for orbital infrastructure, data rights, and collision avoidance.

Overall, the move to space represents a major evolution in cloud computing. AI infrastructure could shift from Earth to orbit, which could provide high performance and nearly universal coverage. It also offers a more sustainable path for AI growth.

The post China Joins Google, Amazon, and xAI in the Race to Build AI Supercomputers in Space! appeared first on Carbon Credits.