China’s Grip on Lithium Tightens as Global Supply Struggles to Keep Up

China has strengthened its hold on the world’s lithium supply chain. The Ministry of Commerce (MOFCOM) updated China’s catalogue of technologies prohibited or restricted from export. They added important battery and lithium processing technologies. This includes lithium carbonate and hydroxide preparation, along with cathode material manufacturing.

The metal is essential for electric vehicles (EVs) and battery storage. With control over lithium mining, processing, and manufacturing, China now dominates nearly every part of this fast-growing sector.

The move lets Beijing control what technical know-how leaves China. It also strengthens its grip on the clean energy supply chain. This control affects global lithium prices, investment, and clean energy goals across Europe, the U.S., and Asia.

China’s Expanding Role in Lithium Production

Lithium demand has soared as countries push for cleaner transport and renewable energy. The International Energy Agency (IEA) says global lithium demand jumped almost 30% in 2024. This rise came mainly from EV production and big battery storage needs.

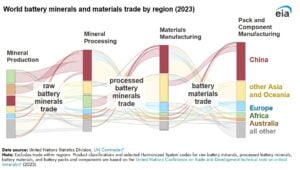

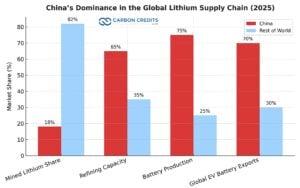

China produces about 18% of the world’s mined lithium, but its real strength lies in refining. Chinese companies hold about 65% of the world’s lithium chemical processing. They also account for over 75% of global battery cell production. These numbers show that even if lithium ore is mined in Chile, Argentina, or Australia, most of it ends up in Chinese refineries, which process it into battery-grade material.

China also leads in midstream and downstream battery manufacturing. In 2024, China made more than 1,200 gigawatt-hours (GWh) of lithium-ion batteries. That’s around three-quarters of the world’s total, as reported by BloombergNEF.

Major producers like CATL and BYD supplied both domestic and foreign automakers, including Tesla, BMW, and Toyota.

The country’s major players, such as Ganfeng Lithium and Tianqi Lithium, have spent years investing in foreign mines. They invest in lithium projects in South America, Africa, and Australia. This helps them secure long-term access to raw materials. This strategy ensures China’s industry gets the feedstock it needs, supports local gigafactories, and boosts global exports.

How Beijing’s Moves Sway Global Lithium Markets

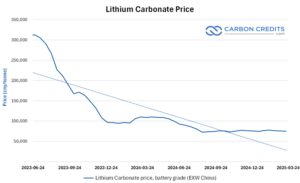

Lithium prices have been on a roller coaster. After record highs in 2022, prices dropped sharply in 2023 and early 2024 due to oversupply. But by mid-2025, prices in China began to rebound. Lithium carbonate traded between CNY 59,000 and 69,000 per metric ton (roughly US$8,500–9,000).

Industry analysts say Chinese producers used this price flexibility to outcompete foreign suppliers. When prices drop, many non-Chinese mining firms, especially in Australia and Africa, struggle to stay profitable.

Some market experts think China oversupplied the market on purpose. They believe this was to keep global influence and slow down rival producers.

Despite recent rebounds, volatility remains high. The IEA warns that lithium demand may double by 2030. It could reach over 1.3 million tonnes of lithium carbonate equivalent (LCE) each year. Without new mines and processing capacity, global shortages might return. This could lead to price spikes that impact battery and EV production worldwide.

- SEE LITHIUM PRICES here…

Technology and Export Controls

China’s advantage goes beyond production scale. It now leads in processing technology, equipment, and battery chemistry. Beijing is now limiting exports of lithium-processing machines and technology. This move aims to protect local industries and manage intellectual property.

In 2025, several Chinese equipment suppliers limited shipments abroad. This makes it harder for competitors in the U.S. and Europe to build their own refining systems. These export limits are part of a broader strategy to keep the high-value stages of the supply chain inside China.

Meanwhile, the U.S. IRA provides up to $369 billion for climate and energy. It includes strong incentives for local battery and mineral production. Europe’s Critical Raw Materials Act aims for 40% of critical minerals used in the EU to come from local or allied sources by 2030. But industry analysts say it could take up to a decade for these efforts to significantly reduce dependence on China.

The Global Response: Diversifying Supply Chains

Governments and companies are now racing to reduce dependence on China. The United States, Canada, and Australia are expanding domestic mining and refining. Chile and Argentina, along with other South American nations, are building local industries. They aim to process lithium instead of just exporting raw materials.

- RELATED: U.S. Lithium Push: How Washington’s Bet on Lithium Americas Could Reshape the Global Market

The IEA warns that global lithium supply must increase sevenfold by 2035 to meet climate goals. That means bringing new mines and refineries online faster while maintaining environmental standards.

In 2024, the World Bank estimated that over €680 billion (US$730 billion) was invested in renewable power and storage. However, only a small part funded the raw material supply. If supply growth lags, battery shortages could slow EV production by the late 2020s.

However, challenges persist. Lithium extraction can strain water resources and ecosystems. Building new facilities also requires stable regulation and financing, which can take years to secure.

Surge Battery Metals: Strengthening North American Supply

In North America, one of the emerging players helping to diversify lithium supply is Surge Battery Metals (CSE: NILI). The company is developing the Nevada North Lithium Project. This project is in one of the U.S.’s most promising lithium-rich areas.

Surge aims to produce battery-grade lithium for the growing North American EV market. Its exploration results have shown strong potential for large-scale, high-grade lithium clay deposits. Projects like Surge’s align with U.S. efforts to build a secure domestic supply chain and reduce reliance on imports from China.

Surge helps ensure supply security and meet environmental goals by creating cleaner extraction and processing methods. Its work supports the U.S. Department of Energy’s plan to create a domestic battery materials supply chain. It seeks to meet 90% of the country’s lithium demand by 2035.

What’s Ahead: Competition, Cooperation, and Climate Goals

The global lithium race is about more than profits. It shapes the pace of the clean energy transition. China’s dominance gives it both economic power and geopolitical influence. Western economies are investing a lot to find new supplies and to lower strategic risks.

The market outlook suggests demand will remain strong throughout the decade. Analysts expect lithium prices to stabilize as new supply enters the market, but competition will remain intense.

For the world to meet its climate goals, cooperation will be as important as competition. Shared technology, recycling, and sustainability standards could help reduce emissions and stabilize supply chains.

Surge Battery Metals and other new miners are working to localize production. They aim to boost transparency and ensure lithium supply helps the clean energy transition, not hinders it.

China now controls the heart of the global lithium industry, from mining and refining to battery exports. This dominance brings both opportunity and risk. The rest of the world is responding, but catching up will take time, investment, and innovation.

The post China’s Grip on Lithium Tightens as Global Supply Struggles to Keep Up appeared first on Carbon Credits.