Google Expands SAF Strategy with Amex GBT and Shell Aviation to Cut Aviation Emissions

Google is stepping up its climate strategy with a deeper commitment to sustainable aviation fuel (SAF). In a new long-term agreement with American Express Global Business Travel and Shell Aviation, the tech giant will source SAF environmental attribute data through the Avelia registry.

This move highlights a bigger trend. Corporations are no longer just offsetting emissions—they are actively shaping clean fuel markets. For Google, SAF is becoming a critical tool to cut emissions from business travel, one of the hardest sectors to decarbonize.

Vrushali Gaud, Global Director of Climate Operations, Google, said:

“Sustainable aviation fuel represents a critical unlock for decarbonizing the hard-to-abate aviation sector and we recognize the importance of long-term agreements to increase demand and expand its availability. We view this as a key opportunity to support the broader ecosystem through this book and claim effort, while making progress towards reducing our own aviation emissions.”

How “Book and Claim” Is Changing the Future of Aviation Fuel

SAF offers a clear advantage. It can reduce lifecycle greenhouse gas emissions by up to 80% compared to traditional jet fuel. That makes it one of the most promising solutions for aviation, a sector with limited low-carbon alternatives.

Google’s participation in the Avelia platform shows how corporate demand can drive supply. Avelia uses a “book and claim” system, allowing companies to claim emissions reductions even if SAF is not physically used on their specific flight. Instead, SAF is added elsewhere in the fuel network, and the environmental benefits are tracked digitally using blockchain.

This system solves a major problem—limited fuel availability. SAF supply is still concentrated in a few locations, while demand is global. By separating physical fuel use from emissions accounting, Avelia expands access and encourages broader adoption.

The platform has already made measurable progress:

- Over 64 million gallons of SAF have been supplied globally

- More than 590,000 tonnes of CO₂ emissions avoided

- Participation from 66 companies and airlines

These numbers signal growing momentum. More importantly, they show how digital infrastructure can accelerate climate solutions in traditional industries.

Beyond Flights: Google’s Broader Transport Strategy to Achieve Carbon-Neutral by 2030

Google’s SAF investment is only one part of a larger plan to cut transport emissions. The company is actively reducing the carbon footprint of both employee commuting and logistics.

Low-Carbon Commutes with EVs

It promotes low-carbon commuting by offering shuttle services, encouraging carpooling, and supporting public transit, cycling, and walking. At its campuses, Google is also investing heavily in electric mobility. By 2024, it had installed over 6,000 EV charging ports across the U.S. and Canada. In India, electric vehicles already make up nearly a quarter of its internal commuter fleet.

At the same time, Google is investing directly in SAF production. In 2024, it joined the United Airlines Ventures Sustainable Flight Fund, a $200+ million initiative supporting next-generation fuel technologies. The fund backs companies like Viridos and Svante, which are working on advanced fuel and carbon capture solutions.

Google is also a member of the Sustainable Aviation Buyers Alliance, further strengthening its role in shaping demand for cleaner aviation fuels.

The Reality Check: SAF Growth Faces Real Barriers

Despite strong corporate interest, SAF still faces significant challenges. Global production is rising fast, but not fast enough.

Production increased 24 times since 2021 and is expected to reach around 713 million gallons by the end of 2025. However, this still represents less than 1% of total jet fuel demand.

Even more concerning, growth may slow in 2026. According to the International Air Transport Association (IATA), production is expected to rise only modestly, reaching about 2.4 million metric tons. At the same time, costs remain high—SAF can be two to five times more expensive than conventional fuel.

This price gap creates a major burden for airlines. In 2025 alone, SAF-related costs could reach $3.6 billion globally. Without stronger policy support, scaling production will remain difficult.

Policy and Market Shifts: A Fragmented Landscape

Policy support plays a crucial role in SAF growth, but global approaches remain uneven.

In the U.S., incentives are weakening. The Clean Fuel Production Tax Credit (45Z) will drop significantly in 2026, reducing financial support for SAF producers. This could slow investment and limit supply growth.

In contrast, Europe is pushing ahead. The ReFuelEU Aviation mandate requires a 2% SAF blend, while countries in Asia, including Singapore and Thailand, are introducing their own mandates starting in 2026.

This divergence creates uncertainty. Companies and producers must navigate different regulations across regions, making long-term planning more complex.

The Feedstock Challenge: The Biggest Bottleneck

Analysts say technology is not the main constraint for SAF—feedstock is.

SAF relies on low-carbon raw materials such as waste oils, agricultural residues, and synthetic fuels. These resources are limited and already in demand from other sectors like renewable diesel and bioenergy.

As competition intensifies, sustainability standards are also becoming stricter. Producers must prove that their feedstocks are traceable and truly low-carbon. This means rapid expansion is unlikely in the short term. Instead, companies are expected to focus on gradual capacity growth and flexible production strategies.

Considering all the above factors, 2026 will not deliver a breakthrough but it will test the foundation of the SAF market. Three factors will define progress:

- Policy credibility: Governments must provide stable, long-term incentives

- Feedstock strategy: Companies need reliable and sustainable supply chains

- Procurement innovation: Airlines and corporations must adopt smarter purchasing models

Momentum is building, but it remains selective. Only companies that align these elements will succeed as the market evolves.

Looking Ahead: Strong Demand Signals for 2030 and Beyond

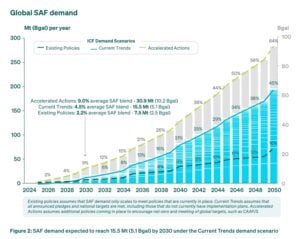

Despite the challenges, SkyNRG’s SAF Market Outlook gives optimistic long-term projections. It highlights that the demand could reach 15.5 million metric tons by 2030 under current trends.

These numbers highlight one key point: demand is not the problem. The challenge lies in scaling supply efficiently and affordably. Nonetheless, sustainable aviation fuel holds real promise. It offers one of the few viable paths to reduce emissions in aviation without redesigning aircraft.

Google’s latest move shows how large corporations can accelerate this transition. But the road ahead remains complex. High costs, limited supply, and policy uncertainty continue to slow progress.

The bottom line is clear: SAF is not scaling overnight. But with the right mix of corporate demand, policy support, and innovation, it could become a cornerstone of clean aviation in the decades ahead.

- ALSO READ: Greening the Aviation: Lufthansa and Airbus Team Up to Cut Business Travel Emissions Using SAF

The post Google Expands SAF Strategy with Amex GBT and Shell Aviation to Cut Aviation Emissions appeared first on Carbon Credits.