Samsung SDI has signed a multi-year battery supply agreement with Mercedes-Benz worth more than 10 trillion won, or about $6.8 billion. The deal marks the South Korean battery maker’s first direct supply contract with the German luxury automaker.

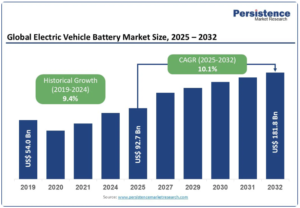

It comes at a time of fast growth in the electric vehicle (EV) battery market. Industry forecasts predict growth from around $92.7 billion in 2025 to $181.8 billion by 2032. This rise is fueled by increasing EV adoption in Europe, China, and the United States.

The agreement strengthens Samsung SDI’s position in the premium EV supply chain. It also shows how automakers are reshaping their sourcing strategies to reduce risk, improve supply stability, and meet long-term carbon goals.

Mercedes-Benz Secures Long-Term Battery Supply for Next-Gen EVs

Mercedes-Benz will use Samsung SDI’s batteries in upcoming compact and mid-size electric SUVs and coupe models. These vehicles are expected to form part of the company’s next wave of electrification plans.

The batteries will use high-nickel NCM (nickel, cobalt, manganese) chemistry. This design improves energy density and driving range. It also supports longer battery life and higher output, which are important for premium EV performance.

The agreement also includes cooperation beyond supply. Both companies plan joint development work on next-generation battery technologies. This signals a deeper strategic partnership rather than a short-term contract.

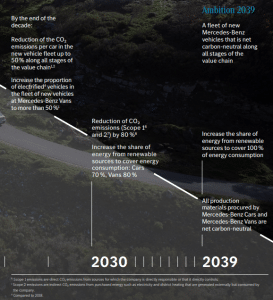

Industry reports suggest the batteries will likely be used in Mercedes-Benz EV platforms from around 2028. This matches the company’s broader shift toward electric-first vehicle architecture, aligning with its Ambition 2039.

Source: Mercedes-Benz

Samsung SDI Expands Its European EV Footprint

The deal significantly strengthens Samsung SDI’s position in Europe’s premium automotive market. The company supplies batteries to major global automakers. This includes BMW, Volvo-linked platforms, and Stellantis joint ventures.

“This partnership brings together the innovative DNA of both companies. It is meaningful in that SAMSUNG SDI has secured a battery order aimed at strengthening its position in the global EV market.”

Europe is becoming a key battleground for battery suppliers. Automakers are moving away from single-source supply chains. They are also reducing dependence on China-based production networks due to geopolitical and logistics risks.

Samsung SDI’s entry into Mercedes-Benz’s supply chain adds scale and visibility. It also improves its exposure to high-margin luxury EV segments.

At the same time, the partnership supports Mercedes-Benz’s supplier diversification strategy. The company already works with LG Energy Solution and SK On for EV batteries, reflecting a multi-supplier model now common in the industry.

The $180B Battery Boom: Why EV Demand Is Still Accelerating

The global EV battery market continues to expand rapidly. Persistence Market Research says the market will grow at a compound annual growth rate (CAGR) of 10.1%. It should hit around $181.8 billion by 2032.

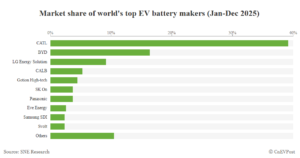

Other industry data shows strong near-term concentration. In 2025, the top two battery producers accounted for 55.6% of global installations, equal to 659.5 GWh out of a total 1,187 GWh, according to SNE Research.

This concentration highlights two trends:

A small number of leaders dominate large-scale production.

Mid-tier players compete for premium contracts and long-term OEM deals.

At the same time, EV battery demand is projected to rise by over 25% each year until 2030. This growth is driven by increased EV adoption in key markets and tougher emissions regulations.

Source: World Economic Forum

This growth is also linked to broader energy transition trends. EV batteries are now central to national decarbonization plans, especially in Europe and North America.

Net-Zero Pressure Shapes Both Automakers and Battery Makers

The Mercedes–Samsung SDI deal is also shaped by climate targets and ESG pressure across the automotive value chain.

Mercedes-Benz has set a goal for its new vehicle fleet to become net carbon-neutral by 2039 across the full lifecycle, including supply chains and production. The company also aims to reduce CO₂ emissions per passenger car by up to 50% compared to 2020 levels.

To support this, Mercedes-Benz is expanding renewable energy use in production. It is also pushing suppliers to reduce emissions in materials such as steel, aluminum, and battery cells.

Samsung SDI is also increasing its focus on low-carbon manufacturing. The company has been expanding efforts in sustainable sourcing and battery efficiency improvements. It is part of a wider Korean battery industry push toward cleaner production and circular battery systems.

Mercedes-Benz has already introduced net carbon-neutral battery cell production requirements for suppliers in its EV programs. This means battery partners must reduce emissions across raw materials and production processes.

These policies are reshaping competition. Battery performance is no longer the only factor. Carbon intensity is becoming a key procurement metric.

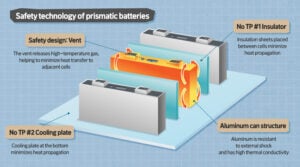

Technology Focus: High-Nickel and Prismatic Battery Design

Samsung SDI’s batteries for Mercedes-Benz will use high-nickel NCM chemistry. This type of battery increases energy density while reducing reliance on cobalt over time.

Higher nickel content generally improves driving range. This is critical for luxury EVs competing on performance and long-distance capability.

The batteries will also use a prismatic format. This rectangular design improves space efficiency inside the vehicle. It also helps with thermal control, which improves safety and performance stability.

Source: Samsung

Key advantages include:

Higher energy density for longer range,

Better space utilization in vehicle design,

Improved thermal management for safety, and

Strong fit for compact and mid-size EV platforms.

These features are important as automakers move toward more compact EV architectures while maintaining premium performance standards.

Market Impact: Strategic Shift in EV Supply Chains

The Samsung SDI–Mercedes-Benz agreement reflects a wider transformation in the EV industry. Automakers are now prioritizing:

Supply chain diversification,

Long-term battery partnerships,

Access to advanced chemistry technologies, and

Lower carbon production systems.

For Samsung SDI, the deal strengthens its position in the global battery race. It adds a major European luxury OEM to its customer base and increases visibility in the premium EV segment.

For Mercedes-Benz, the agreement supports its electrification roadmap while reducing reliance on single suppliers and improving supply chain resilience.

The financial scale of the deal also signals confidence in long-term EV demand, despite short-term market volatility in the sector. As EV adoption continues to grow and battery demand rises sharply toward 2030, partnerships like this are likely to become more common across the industry.

The agreement highlights a key shift. Battery supply is no longer just a procurement decision. It is now a strategic pillar of global automotive competition and decarbonization.

As FIFA prepares for its upcoming World Cup tournaments from June 11 to July 19, 2026, its climate strategy is facing closer attention, too. The organization has set a goal to reach net zero emissions by 2040. It also aims to cut emissions by 50% by 2030.

These targets are part of FIFA’s long-term sustainability plan, which aligns with the UN Sports for Climate Action Framework and the Paris Agreement. FIFA first announced its climate strategy in 2021 and has since applied it across major tournaments.

However, the challenge is not setting targets. The real challenge is reducing emissions in a global event that depends on international travel. The World Cup is one of the most complex events to decarbonize because most emissions come from sources outside direct control.

FIFA’s Climate Commitments and Official Emissions Targets

FIFA’s climate strategy follows a structured pathway based on global climate standards. It includes measuring emissions, reducing them where possible, and offsetting what remains.

The organization has committed to three main actions:

Reduce greenhouse gas emissions by 50% by 2030.

Achieve net zero emissions by 2040.

Align operations with international climate frameworks.

FIFA reports emissions using standard greenhouse gas accounting. This includes tracking emissions across tournaments, host cities, and operational activities.

Source: FIFA

In past tournaments, FIFA has introduced sustainability measures such as energy-efficient stadiums, waste reduction programs, and public transport planning. For example, several recent World Cup venues have used renewable electricity and modern cooling systems to reduce energy demand.

FIFA also works with host countries to improve infrastructure planning. This includes encouraging the use of existing stadiums and limiting new construction where possible. These steps aim to reduce emissions linked to building materials and long-term infrastructure.

Still, these efforts mainly affect operational emissions. The larger challenge lies beyond stadiums and facilities.

How Emissions Are Measured in the World Cup

FIFA measures emissions using the widely accepted Scope 1, Scope 2, and Scope 3 framework.

Scope 1 emissions come from direct sources such as fuel use in vehicles and on-site operations. Scope 2 emissions come from purchased electricity used in stadiums and facilities. These emissions can be reduced through renewable energy and efficiency improvements.

Scope 3 emissions include all indirect emissions linked to the event. These are the most complex and the largest category.

In the World Cup, Scope 3 emissions come from these sources:

International and domestic travel by fans,

Team and staff transportation,

Accommodation and hospitality services,

Supply chains and merchandise production, and

Broadcasting and logistics operations.

In large global events, Scope 3 emissions often account for more than half of total emissions. The share is even higher due to the scale of international travel in football tournaments.

This structure shows that most emissions do not come from FIFA’s direct operations. They come from the wider system that supports the event.

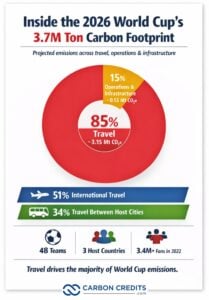

By the Numbers: Inside the 3.7M Ton Carbon Footprint of 2026 World Cup

The FIFA World Cup is one of the largest global sporting events. The 2022 tournament in Qatar drew over 3.4 million spectators, according to FIFA, and reached billions of viewers worldwide. This level of participation creates a large environmental footprint.

For the 2026 FIFA World Cup, hosted by the United States, Canada, and Mexico, total emissions are projected at around 3.7 million tonnes of CO₂ equivalent (CO₂e). This estimate comes from the United 2026 bid’s environmental impact assessment. It reflects the full lifecycle footprint of the event, including travel, operations, and infrastructure.

Transportation is the main driver of these emissions. About 85% of total emissions are linked to travel, especially air travel. This includes both international flights and travel between host cities.

The scale of the 2026 tournament adds to this challenge. It will feature 48 teams, up from 32 in previous editions, and will span multiple countries and cities. This increases travel demand, distances between matches, and overall logistics complexity.

The structure of emissions can be summarized as follows:

~85% from travel-related activities (~3.15 million tonnes CO₂e)

~15% from operations, energy use, and infrastructure (~0.55 million tonnes CO₂e)

Travel emissions alone include:

51% from international journeys

34% from travel between host cities

Compared with more compact tournaments, this format leads to higher emissions due to increased reliance on long-distance flights.

Scope 3 Emissions: The Core Climate Challenge

The emissions profile of the World Cup highlights a clear imbalance. Most emissions fall under Scope 3, which includes indirect sources such as travel, logistics, and supply chains.

Scope 1 and Scope 2 emissions, which cover direct operations and energy use, represent only a small share of the total footprint. These can be reduced through renewable energy and efficient design.

Scope 3 emissions are different. They come from activities outside FIFA’s direct control. These include fan travel, team transport, global logistics, and services linked to the event. This creates a structural challenge. Even if FIFA reduces emissions from stadiums and operations, total emissions can remain high due to travel demand.

In simple terms, the World Cup’s carbon footprint is driven more by movement than by infrastructure.

Scope 3 is also the hardest category to reduce. It depends on global travel patterns, geography, and individual choices. FIFA cannot fully control how fans travel or how often they move between cities.

This is why Scope 3 emissions are central to the climate challenge. They account for the largest share of emissions and the biggest barrier to reducing the World Cup’s overall footprint.

Cuts vs. Credits: The Ongoing Offset Debate

To meet its climate targets, FIFA uses both emissions reduction and carbon offsetting. Reduction focuses on lowering emissions at source. This includes improving energy efficiency, using renewable electricity, and optimizing event operations.

Offsetting is used to balance emissions that cannot be eliminated. This involves investing in projects that reduce or remove carbon emissions elsewhere.

Carbon offsets can include projects such as reforestation, renewable energy development, and carbon capture. However, their effectiveness depends on project quality, verification, and long-term impact.

This has led to debate in climate policy. Some experts argue that offsets should not replace real emissions reduction. Others point out that offsets can support the transition when used carefully.

The key issue is transparency. Clear reporting and verified data are needed to ensure that net-zero claims reflect real outcomes.

Why Net Zero Is Difficult for Mega Sports Events

Mega sporting events like the World Cup have unique challenges. They are temporary, global, and highly mobile. Their emissions come from:

International travel,

Temporary infrastructure,

Large-scale logistics, and

Global audience participation.

Even with strong sustainability measures, these factors create a high baseline of emissions.

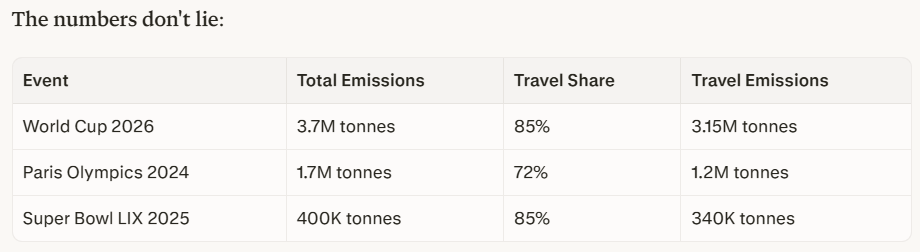

Take for example, the Paris 2024 Olympics. The event’s total footprint hit 1.7 million tonnes CO₂e. Travel caused 72%, that’s 1.2 million tonnes, from 720,000+ international visitors. Stadiums run on 100% renewables, but aviation emissions? Untouched.

Super Bowl LIX in 2025 told the same story. The event generated 400,000 tonnes CO₂e, with 85% coming from 150,000+ out-of-state fans flying to New Orleans. The NFL bought 400,000 offsets for carbon-neutral claims. Still, travel cuts? Zero.

This pattern is industry-wide. Organizers control stadium power. Fans control flights. These mega-events lean on offsets, not aviation reductions. FIFA faces the same problem that other organizers couldn’t easily resolve.

Thus, decarbonization becomes more complex. It also means progress may be slower compared to sectors with more direct control over emissions.

What a Credible Net Zero World Cup Requires

For FIFA’s net-zero goals to be credible, several conditions need to be met.

Emissions must be clearly measured and reported across all scopes. This includes full disclosure of total emissions before offsets are applied. Transparency is essential for trust.

There must also be a stronger focus on reducing emissions at source. While offsets can play a role, long-term progress depends on real reductions.

Independent verification of emissions data can improve credibility. Better coordination of travel and logistics can also help reduce unnecessary emissions.

In the long term, advances in low-carbon transport, including sustainable aviation fuels, may help reduce travel-related emissions.

Final Whistle: Can FIFA Turn Climate Targets Into Reality?

FIFA has set clear climate targets, including net zero emissions by 2040. These targets reflect growing pressure on global organizations to reduce their environmental impact.

However, the data shows a clear challenge. Most emissions from the World Cup come from indirect sources, especially global travel. Scope 3 emissions dominate the total footprint and remain difficult to control. This makes them the key factor in any net-zero strategy.

As the World Cup continues to grow in scale, emissions challenges will also increase. Operational improvements can reduce part of the impact, but they cannot fully address the larger system.

The future of football’s climate strategy will depend on how this gap is managed. The goal is not only to set targets, but also to achieve measurable and transparent progress in a global, complex system.

In this field, will FIFA lead or lag? We will watch this space closely.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-04-21 10:15:232026-04-21 10:15:23FIFA World Cup and the 3.7 Million-Tonne Problem: Can Football’s Biggest Event Reduce Its Climate Impact?

American EV maker Rivian and battery recycling leader Redwood Materials are showing how retired EV batteries can do more than power cars. Their new partnership at Rivian’s Illinois manufacturing plant uses second-life batteries as stationary energy storage, creating a model that could support factories, strengthen the grid, and lower electricity costs.

The project starts with more than 100 used Rivian battery packs. Together, they will deliver 10 megawatt-hours of dispatchable energy at Rivian’s Normal, Illinois facility. That stored energy will help the plant reduce electricity use during peak-demand periods, cut costs, and ease stress on the power system.

The numbers behind the opportunity are much larger. The press release reveals that by 2030, the U.S. is expected to need more than 600 gigawatt-hours of energy storage to support rising electricity demand, stabilize peak loads, and power expanding digital infrastructure. Simply put, it is equivalent to the total energy output of the Hoover Dam running continuously for two months.

Rivian Founder and CEO RJ Scaringe said,

“EVs represent a massive, distributed and highly competitive energy resource. As energy needs grow, our grid needs to be flexible, secure, and affordable. Our partnership with Redwood enables us to utilize our vehicle’s batteries beyond the life of a vehicle and contribute to grid health and American competitiveness.”

Second-Life Batteries Move Beyond Recycling

The Rivian-Redwood system gives retired EV batteries a second job before recycling. Redwood will integrate the battery packs into a stationary storage system using its Redwood Pack Manager software. The technology allows batteries with different levels of degradation and chemistries to work together safely.

This is important because EV batteries often remain healthy long after vehicles retire. Many can still serve for years as stationary storage assets. This creates a powerful circular economy model. Instead of going straight to recycling, batteries can generate added value while supporting energy needs.

Source: Redwood Materials

The supply potential is significant. Redwood already receives more than 20 GWh of batteries each year, equal to roughly 250,000 EVs. The company says that by 2030, end-of-life batteries could supply more than 50% of the entire energy storage market.

And this could make second-life batteries a major domestic energy resource.

JB Straubel, Redwood Materials Founder and CEO, also commented on this development. He said,

“Electricity demand is accelerating faster than the grid can expand, posing a constraint on industrial growth. At the same time, the massive amount of domestic battery assets already in the U.S. market represents a strategic energy resource. Our partnership with Rivian shows how EV battery packs can be turned into dispatchable energy resources, bringing new capacity online quickly, supporting critical manufacturing, and reducing strain on the grid without waiting years for new infrastructure. This is a scalable model for how we add meaningful energy capacity in the near term.”

The timing is critical because electricity demand is accelerating.

Artificial intelligence, cloud computing, and hyperscale data centers are pushing power demand sharply higher. Research from the Belfer Center cited,

The Lawrence Berkeley National Laboratory predicts that data center demand will grow from 176 terawatt hours (TWh) in 2023 (or, about 4.4% of total U.S. electricity consumption) to between 325-580 TWh (6.7-12.0%) by 2028.

Secondly, according to the Battery Council International, data center demand is expected to quadruple by 2030, again driven by AI and cloud computing. This surge is one reason stationary battery systems are becoming essential.

Battery Energy Storage Systems, or BESS, help store electricity and release it when demand spikes. They support peak shaving, frequency regulation, microgrids, and backup power.

Uninterruptible Power Supply (UPS) systems play a different role. They provide immediate short-term power support for critical systems such as data centers, telecom networks, and emergency infrastructure, where even brief outages can cause major disruption.

Together, UPS and BESS are becoming critical to keeping digital infrastructure running.

Market Size

Speaking about market size, the global commercial and industrial battery energy storage market is forecast to reach $21 billion in value by 2036, driven by AI-fueled data center construction, according to research from Globe Newswire.

This is where the Rivian-Redwood model becomes useful. It connects second-life batteries to one of the fastest-growing needs in the energy system. The modular structure of repurposed battery systems may also allow faster deployment than traditional infrastructure, which can take years to build.

Circular Economy Meets Energy Security

The project also supports energy security. Using domestic battery assets for storage can reduce dependence on imported energy storage systems. It may also help defer billions of dollars in grid infrastructure upgrades. This is vital when the U.S. is looking for ways to expand electricity capacity faster.

Second-life batteries can also help during high-stress events. During heat waves or peak demand events, stored energy can be discharged instantly to reduce strain on the grid and avoid buying higher-cost electricity.

It creates economic and reliability benefits at the same time.

The partnership also shows how batteries are evolving from transportation assets into broader infrastructure assets. And this shift can have wide implications for manufacturing, utilities, defense facilities, and digital infrastructure.

Market Competition and Technology

Redwood faces competition from established players in the energy storage market. Tesla has been running Megapack as a first-life business, while Redwood is building a parallel market in second-life batteries.

The Redwood Pack Manager technology acts as specialized software that enables battery packs with different degradation levels and chemistries to work together safely. This capability is crucial for second-life applications where batteries have varying performance characteristics.

Second-life batteries are gaining traction in industrial applications. Battery costs have fallen to historic lows, making these projects increasingly viable economically.

A Blueprint for the Next Phase of Clean Energy

Rivian and Redwood’s 10 MWh deployment represents a practical solution to two major challenges: managing retired EV batteries and meeting surging industrial energy demand. The project demonstrates how automakers can extract additional value from their battery investments while supporting grid stability.

As AI-driven electricity demand continues climbing and EV adoption accelerates, second-life battery projects could become standard practice across the automotive industry. The success of this Illinois pilot may influence how other manufacturers approach end-of-life battery management, creating a new revenue stream while supporting America’s clean energy transition

This project suggests one answer is to connect those two problems. Old EV batteries can become new energy infrastructure.

Europe’s climate transition is entering a new phase. In the space of a few weeks, three major developments have emerged across the continent: the launch of the first commercial robotaxi service, a historic surge in electric vehicle (EV) sales, and another drop in carbon emissions under the EU’s flagship trading system.

Each story is different, but together, they point in the same direction. Europe is rapidly reshaping how people move, how energy is consumed, and how emissions are controlled. At the same time, the pace and stability of this transition remain uneven.

Robotaxis Arrive: Europe’s First Commercial Deployment

Europe has officially entered the autonomous mobility era. In Zagreb, the Croatian company Verne launched the first robotaxi service in Europe. This service uses the seventh-generation system from the Chinese firm Pony.ai. The service allows the public to book and pay for fully autonomous rides using the Verne app.

The launch marks a shift from testing to real-world deployment. The service operates in a defined zone of around 90 square kilometers across central Zagreb, including the airport. It runs daily from 7:00 a.m. to 9:00 p.m., according to company disclosures.

The fleet uses Arcfox Alpha T5 electric vehicles, built by BAIC and equipped with Pony.ai’s Gen-7 autonomous driving technology. For safety, trained operators stay in the front seat during this early rollout. The system is fully autonomous for passengers in the back.

Each vehicle carries up to two passengers per trip, reflecting the controlled nature of this early deployment stage.

Verne, a spin-off from Rimac Group, operates the fleet. The company was originally planning a custom-built robotaxi but has now launched using existing vehicle platforms. It has already tested dozens of prototype vehicles and is preparing for scale-up.

This launch is significant for Europe. Until now, autonomous ride-hailing has been largely concentrated in the United States and China. Europe has been slower due to stricter safety rules and regulatory frameworks.

But the commercial rollout changes that narrative. As Verne’s leadership noted, Europe now needs autonomous systems that move beyond pilots into real services.

Expansion is already planned. Partners plan to expand to thousands of robotaxis in over 20 cities worldwide. Uber will also help with future deployments and investment talks. This suggests Zagreb is not the endpoint, but the starting point.

EV Sales Break Records as Fuel Prices Surge

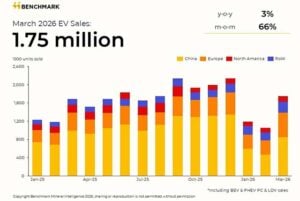

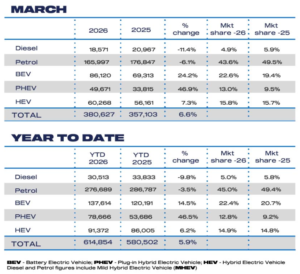

At the same time, Europe’s electric vehicle market is accelerating at an unexpected pace.

In March, the region hit over 500,000 monthly EV sales for the first time. Registrations jumped about 37% from last year, reaching nearly 540,000 units, based on data from Benchmark Mineral Intelligence. The region’s EV sales reached 1.2 million units in the first quarter, up 27% year-on-year.

This surge is not happening in isolation. Rising fuel costs are tied to geopolitical disruptions that have increased global oil prices. As petrol and diesel became more expensive, consumers increasingly shifted toward electric alternatives.

In Germany, the biggest car market in Europe, battery electric vehicle registrations soared 66.2% from last year. In March alone, over 70,000 units were registered, as reported by the Federal Motor Transport Authority (KBA). EVs now account for roughly 24% of all new car registrations in the country, overtaking petrol in monthly sales for the first time.

This is a major shift for a market that struggled just a year earlier. Germany cut subsidies in 2024, leading to a sharp drop in demand. Then, in 2026, it reversed the policy and reintroduced incentives of up to €6,000 for each electric vehicle. At the same time, fuel prices surged. Diesel crossed €2.50 per litre, one of the highest levels on record.

Elsewhere in Europe, similar trends are visible.

The UK saw 86,120 new battery electric vehicle registrations in March. This is a 24.2% increase compared to last year, according to the Society of Motor Manufacturers and Traders. EVs now represent over 22% of the UK market, although still below mandated targets for 2026.

Source: whicheve.net

Across the continent, fuel prices have become a key driver of change. Gasoline prices jumped about 17% in key EU countries. Diesel surged up to 30% in some areas. This followed supply issues tied to geopolitical tensions and unstable oil routes.

Even after oil prices eased from earlier peaks near $120 per barrel, they remain significantly above pre-crisis levels, keeping pressure on consumers.

Online car platforms show how quickly sentiment is shifting. EV searches and inquiries have surged in Germany, the UK, and Spain. This shows a rising consumer urgency, not just slow adoption.

But questions remain about durability. Previous fuel-driven EV surges have faded once prices stabilized. This time, however, structural forces are stronger: tighter EU emissions rules, more affordable EV models, and expanding charging infrastructure are reinforcing demand.

A key economic factor is running cost. In markets like Belgium, driving an EV now costs 45–56% less per kilometre than petrol or diesel vehicles when charged at home.

Emissions Continue to Fall—but Progress Is Uneven

While transport electrification accelerates, Europe’s emissions trend continues downward.

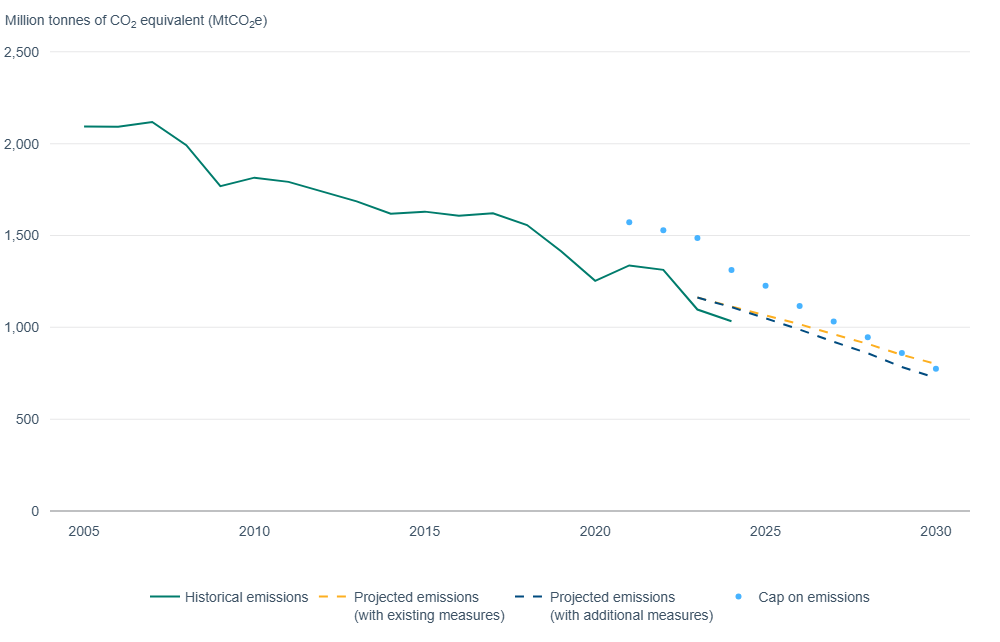

The European Commission reports that emissions under the EU Emissions Trading System (EU ETS) dropped by 1.3% in 2025. This decline continues a long-term trend in the bloc’s industrial and energy sectors.

The EU ETS covers around 45% of total EU greenhouse gas emissions, including power generation, heavy industry, aviation, and maritime transport. It operates under a declining cap system designed to force emissions reductions over time.

Since 2005, emissions in covered sectors have fallen by roughly 50%, placing the EU broadly on track toward its 2030 target of a 62% reduction.

Source: EU

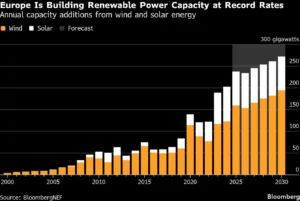

A major driver of recent progress is the power sector. Renewables continue to expand rapidly. Solar generation rose over 20% in 2025. Together, wind and solar made up about 30% of EU electricity. This marked the first time they surpassed fossil fuels in total share.

Overall, renewables supplied roughly 48% of Europe’s electricity in 2025, compared with declining fossil fuel contributions. Coal has seen the sharpest decline, falling to just 9.2% of electricity generation, down from nearly 25% a decade ago.

However, the transition is not linear.

Natural gas usage has remained volatile, and in some cases increased, as it continues to play a balancing role in the energy system. Aviation emissions have also risen as travel demand recovered after the pandemic, highlighting one of the hardest sectors to decarbonize.

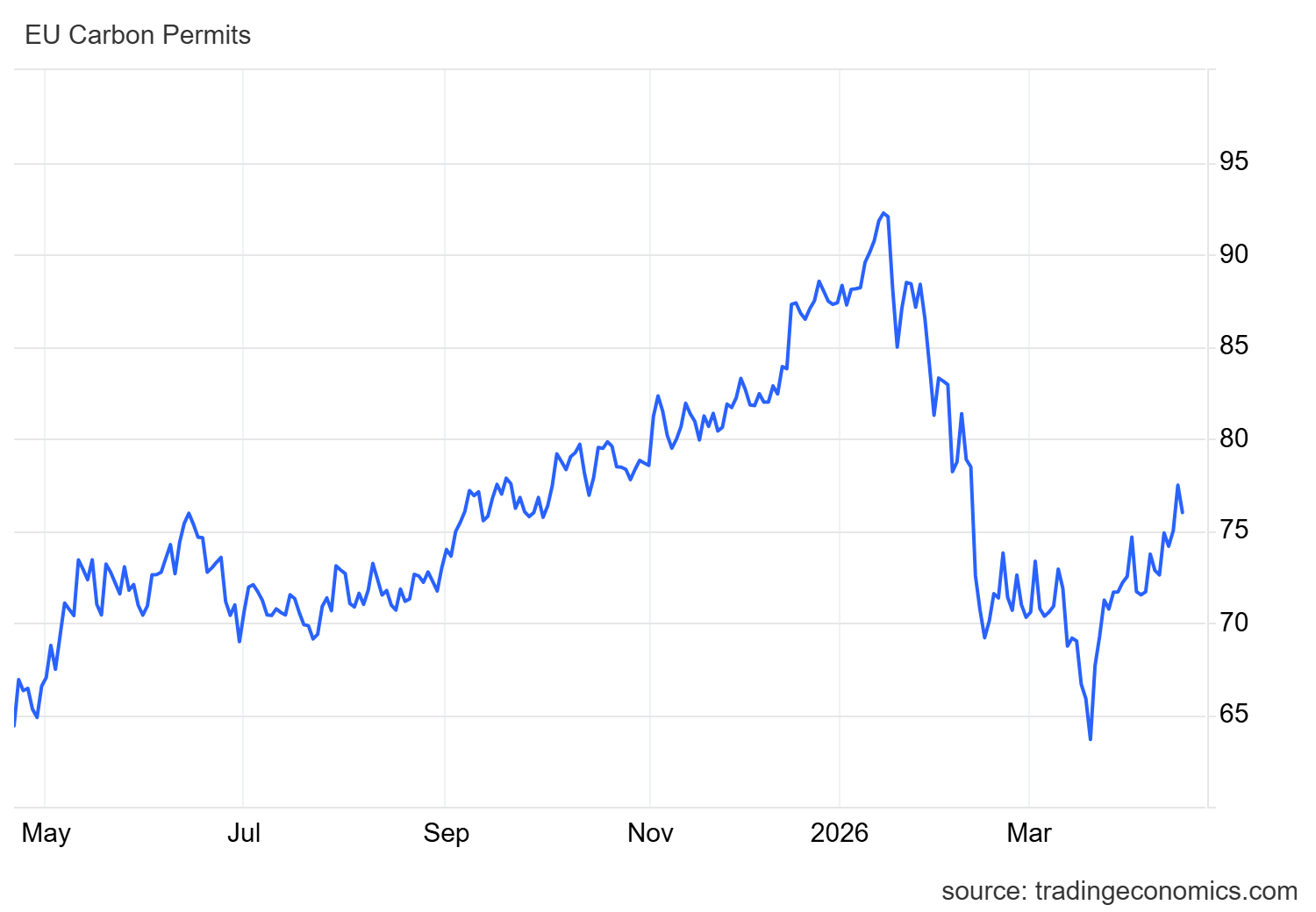

Carbon markets reflect this mixed picture. EU carbon allowance prices have remained around €70–75 per tonne, supported by steady demand but influenced by shifting energy dynamics.

A Transition Moving at Uneven Speeds

Taken together, these three developments reveal a Europe that is transforming quickly—but not evenly. Robotaxis in Zagreb show how fast mobility innovation is moving when regulation, technology, and investment align.

Record EV sales show how sensitive consumer behaviour is to energy prices, incentives, and infrastructure. And falling emissions show that policy frameworks like the EU ETS are still effective in driving long-term reductions.

But they also show limitations. Electrification is rising, but unevenly across countries. Emissions are falling, but not fast enough in harder sectors like aviation and gas-heavy power systems. And innovation is advancing, but still constrained by regulation and scale.

Europe’s climate transition is no longer theoretical. It is visible in cities, car markets, and industrial emissions data. The path forward may be complex, and there are constraints; still, progress is real.

Europe is not just decarbonizing but is redesigning how mobility, energy, and industry interact. And that process is only just beginning.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-04-21 09:15:192026-04-21 09:15:19Europe’s Green Shift Hits Overdrive: Robotaxis Launch, EV Sales Surge, Emissions Fall

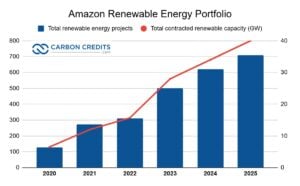

Amazon has expanded its renewable energy portfolio in Australia to 990 MW across 20 projects. This marks a major jump from about 430 megawatts (MW) previously, driven by new agreements with multiple solar, wind, and battery projects. These include large-scale developments such as the Golden Plains wind farm and hybrid solar-battery installations built on former coal sites.

This expansion is not just about energy supply. It is closely tied to the growing demand from data centers that power cloud computing and artificial intelligence (AI). As Amazon Web Services (AWS) expands, energy demand continues to rise.

AI Data Centers Are Driving Amazon’s Energy Surge

The scale of energy required for digital infrastructure is increasing fast. Data centers already consume large amounts of electricity, and that demand is expected to grow sharply.

According to the International Energy Agency, global data center electricity use reached about 415 terawatt-hours (TWh) in 2024. This could rise to over 1,000 TWh by 2026, largely due to AI workloads.

Australia is also seeing this trend. Estimates suggest that data centers in the country now consume electricity comparable to all shopping centers combined. This is particularly according to Matt O’Rourke, AWS’s head of infrastructure and energy policy in Australia and New Zealand. He said:

“If you think about it from an economy-wide perspective, all of the datacentres in Australia collectively consume the same amount of electricity as all of the shopping centres, but the datacentres are … facilitating new renewable energy coming into the grid.”

This puts pressure on grids and increases the need for stable, clean power sources. As a result, companies like Amazon are investing directly in renewable energy rather than relying only on grid supply.

How Amazon Locks in Clean Power for Growth

Amazon’s clean energy strategy is built around long-term power purchase agreements (PPAs). These contracts allow Amazon to buy electricity from new wind and solar projects over 10 to 20 years.

This approach gives Amazon more control over its energy future. It also supports its growing demand from AWS data centers, which require a large and stable power supply 24/7.

By 2025, Amazon is among the world’s largest corporate buyers of renewable energy. It has invested in more than 500 wind and solar projects around the globe. These projects will create enough clean electricity to power millions of homes each year, according to company reports.

PPAs also help in three key ways:

They secure a long-term energy supply for fast-growing cloud infrastructure.

They reduce exposure to short-term electricity price swings.

They help finance new renewable projects by guaranteeing future revenue.

Battery storage is becoming a key part of this system. Amazon is supporting grid-scale storage projects that store excess solar and wind power during peak production and release it when demand is high. This helps smooth out renewable energy variability and improves grid reliability.

Amazon also highlights that many of its renewable projects are designed to add new clean capacity to the grid, not just buy existing power. However, independent analysts have pointed out that climate impact can change based on where a project is located and how the grid is set up. So, results aren’t always the same across different markets.

Climate Pledge in Action: Amazon’s Race to Net Zero

Amazon aims for net-zero carbon emissions by 2040. This goal is part of its Climate Pledge and is ten years earlier than the Paris Agreement timeline.

Source: Amazon

The company reports strong progress in renewable energy deployment. It says it has already reached 100% renewable energy matching for its global operations on a “procured energy basis” by 2023, ahead of its original 2030 target. This is based on contracted renewable energy capacity rather than hourly matching.

Amazon has put money into hundreds of wind and solar projects in North America, Europe, and Asia. This makes it one of the biggest companies boosting new renewable energy worldwide.

Beyond electricity, Amazon is expanding into broader decarbonization areas. This includes electric delivery vehicles, with a target of deploying 100,000 electric delivery vans by 2030 as part of its logistics transition. It is also investing in sustainable aviation fuel (SAF) partnerships and low-carbon fuels to reduce transport emissions.

The company is also scaling energy efficiency in its operations. This includes better warehouse design, smarter AI logistics routing, and improved cooling systems for AWS data centers.

However, emissions remain a structural challenge. Amazon reported 68.25 million metric tons of CO₂e emissions in 2024, up from 64.38 million metric tons in 2023.

Source: Amazon

While the company has expanded its renewable energy use and lowered emissions intensity in some areas, total emissions rose as its logistics, e-commerce, and data center businesses continued to grow.

This highlights a key tension. Amazon is investing in clean energy, but demand from AI, cloud services, and global logistics can raise overall energy use. This makes decarbonization a moving target rather than a fixed endpoint.

Australia’s Renewable Energy Market Is Scaling Fast

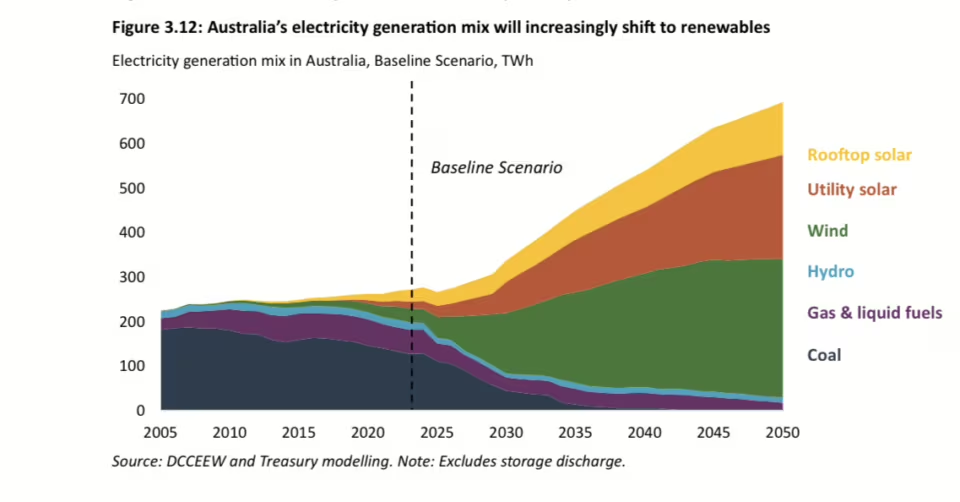

Amazon’s expansion comes at a time of rapid growth in Australia’s clean energy sector. According to the Australian Energy Market Operator, renewables are expected to supply over 80% of Australia’s electricity by 2030 under current plans.

Chart from The Energy.com

Solar and wind are leading this transition. Australia already has one of the highest rates of rooftop solar adoption globally, and large-scale projects continue to expand. Battery storage is also scaling quickly. This is critical for managing variability and supporting grid stability.

Corporate demand is playing a growing role in this clean power landscape. Companies are increasingly signing PPAs to secure clean energy. This helps finance new projects and accelerate the transition.

Amazon is part of a broader trend. Other tech firms, including Microsoft and Google, are also major buyers of renewable energy worldwide.

AI vs Climate Goals: The Growing Energy Dilemma

Despite progress, challenges remain. Data centers require not only electricity but also water for cooling and large physical infrastructure.

Some local governments in Australia have raised concerns about the impact of new data centers on power supply and community resources. This reflects a global issue. AI demand is growing faster than the clean energy supply in many regions.

Companies are responding with multiple strategies:

Improving the energy efficiency of hardware,

Using advanced cooling systems, and

Building data centers in regions with strong renewable supply.

Still, total energy use continues to rise. This creates a gap between emissions targets and actual demand.

Tech Companies Become Energy Players, Not Just Users

Amazon’s move to reach nearly 1GW of renewable capacity in Australia signals a broader shift. Energy is becoming a core part of digital infrastructure strategy.

Companies are no longer just technology providers. They are also major energy buyers and investors. This shift is reshaping both industries.

Renewable energy projects now depend more on corporate demand. At the same time, tech companies depend on stable, low-carbon power to support growth. The result is a tighter link between the energy transition and the digital economy.

A Defining Moment for Big Tech’s Energy Strategy

Amazon’s expansion highlights a key turning point. The growth of AI and cloud computing is driving a new wave of energy demand. At the same time, companies are under pressure to meet climate targets. This creates both risk and opportunity.

The move to 1GW in Australia shows how companies are responding. They are investing directly in clean energy to secure supply and reduce emissions.

But the challenge is far from over. As demand continues to grow, the balance between expansion and sustainability will become even more important. For now, one thing is clear: the future of AI will depend as much on energy systems as on technology itself.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-04-20 11:15:072026-04-20 11:15:07Amazon Nears 1GW Clean Energy in Australia, with AI Data Centers Triggering Power Boom

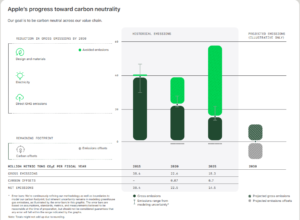

Apple’s latest Environmental Progress Report shows a clear shift in how the company is approaching sustainability. It shows that 30 percent of materials across all products shipped in 2025 came from recycled content, up from the previous year. This represents a steady year-on-year increase of around 6% points, showing consistent progress rather than one-time gains.

The company now uses 100% recycled cobalt in all its batteries. It also uses 100% recycled rare earth elements in all magnets. All of these show how circular manufacturing is becoming a core part of the way Apple designs, builds, and scales its products.

The shift reflects a broader strategy. The tech giant is working to reduce reliance on virgin mining and move toward a more circular supply chain. This is central to its long-term goal of reaching carbon neutrality across its entire value chain by 2030.

Recycled Materials Move Into Core Product Architecture

The most important change is not just how much recycled material Apple uses, but where it is being used. In its newest product line, including the MacBook Neo, Apple has significantly increased recycled content in critical components. According to the company’s 2026 Environmental Progress Report:

Around 90% of the aluminum in the MacBook Neo enclosure is recycled

100% of cobalt in Apple-designed batteries is recycled

The device overall reaches around 60% recycled content across key materials

These figures matter because aluminum and cobalt are among the most carbon-intensive materials in electronics manufacturing. Primary aluminum production uses a lot of energy. Cobalt extraction causes high emissions and comes with supply chain risks.

By shifting toward recycled inputs, Apple reduces emissions at the earliest stage of production. And that’s before devices are even assembled. This approach is part of a broader design philosophy.

The iPhone maker is increasingly engineering products around material recovery, not just performance or cost. That shift is central to its decarbonization strategy.

Emissions Avoidance Becomes a Key Climate Lever

Apple’s report highlights a clear link between recycled materials and emissions reduction.

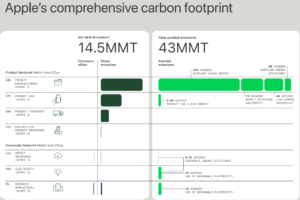

In 2024, the company says that its use of recycled and lower-carbon materials helped avoid 6.2 million metric tons of greenhouse gas emissions. Over the same period, Apple’s total carbon footprint was 15.1 million metric tons. This means that material strategy alone accounted for a meaningful portion of the emissions reduction impact.

The logic is straightforward. When recycled materials replace virgin mining and refining, emissions fall sharply. This is especially important for metals like aluminum, copper, and cobalt, which carry high embedded carbon.

Source: Apple

Apple is effectively shifting emissions reductions upstream — reducing impact before manufacturing even begins.

Meet Daisy, Dave & Cora: The Robots Powering Apple’s Recycling Revolution

A key part of Apple’s system is automation in recycling. The company has developed a set of specialized robotics platforms designed to recover materials from used devices at scale.

The first system, Daisy, can disassemble up to 36 different iPhone models and process as many as 1.2 million devices per year. Engineers designed it to efficiently recover high-value components that traditional recycling systems often miss.

Another system, Dave, focuses on dismantling the taptic engine, a component rich in rare earth magnets, tungsten, and steel. These materials are critical for electronics production but difficult to recover without precision engineering.

The newest system, Cora, expands Apple’s recycling capability further. It uses smart shredding and sensor sorting to boost recovery rates for more types of materials.

Together, these systems form a structured recovery pipeline. Devices returned through Apple’s trade-in and recycling programs are not simply dismantled. They are processed with the goal of reintroducing materials back into future product cycles.

This is a key shift. Instead of linear production — mine, build, dispose — Apple is moving toward closed-loop manufacturing.

Why Materials Are Now the Heart of Apple’s Net-Zero Plan

Apple’s recycled materials strategy is directly tied to its climate target.

The company aims to be carbon neutral by 2030. This commitment includes its business, supply chain, and product lifecycle. It also includes not just its own operations but also supplier emissions and product use emissions.

Source: Apple

Within this framework, materials and manufacturing are the largest drivers of Apple’s emissions. The company’s lifecycle analysis reveals that most of its carbon footprint comes from product manufacturing. This mainly happens in Scope 3 supply chain activities like raw material extraction, component production, and assembly.

Apple also sees materials, electricity, and transportation as the top three sources of product emissions. Materials are key because metals like aluminum, cobalt, and rare earth elements have high carbon intensity.

This is why recycled content is central to Apple’s decarbonization roadmap. It reduces emissions in Scope 3 categories, which are typically the hardest to control.

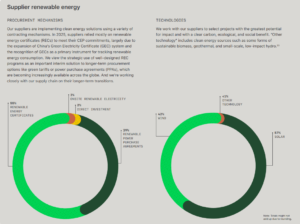

Apple has also pushed suppliers to adopt renewable energy and lower-carbon production methods, particularly in high-impact manufacturing regions. This creates two ways to reduce emissions: cleaner energy and cleaner inputs.

Emissions Profile Shows Progress, But Not a Straight Line

Apple’s emissions profile reflects both progress and complexity. The company’s total footprint is in the tens of millions of metric tons each year, reflecting the scale of its global operations.

In 2025, the company reported a total net carbon footprint of 14.5 million metric tons of CO₂e, down from 15.3 million metric tons of gross emissions before offsets.

Product manufacturing is still the main source of emissions, accounting for the largest share of emissions within Scope 3. In fact, manufacturing alone contributed about 8.15 million metric tons of CO₂e, or more than half of total product lifecycle emissions.

Source: Apple

However, Apple reports gradual reductions in emissions intensity per product over time. Emissions have dropped by over 60% since 2015, while revenue has risen sharply during this time.

This means each device is now easier to make with less carbon. Total emissions can still change based on product cycles and demand.

The increasing use of recycled materials is a key driver of this improvement. It reduces the need for mining, refining, and high-energy processing — all of which sit upstream in the supply chain.

However, Apple’s emissions trajectory is not linear. Like many hardware companies, its reach depends on global demand, new product launches, and supply chain limits. This makes structural changes like material redesign more important than incremental operational gains.

Apple’s Carbon Credit Portfolio

Moreover, Apple uses carbon credits in a targeted way to address a small portion of its remaining emissions as it works toward its 2030 net-zero goal. The 2026 Environmental Progress Report states that the company retired verified credits from nature-based projects in 2025.

The portfolio includes the Lumin/Eucapine reforestation project in Uruguay, which accounted for 422,395 metric tons CO₂e (vintage 2020). It also includes the Windrock Improved Forest Management project in the United States, covering 319,785 metric tons CO₂e (vintage 2022).

These projects focus on restoring degraded land, improving forest management, and increasing long-term carbon sequestration. Apple sees carbon credits as a complement, not as substitutes, to its main decarbonization strategy.

This strategy focuses on reducing emissions first. It emphasizes using recycled materials, renewable energy, and improving the supply chain. Only after these efforts does Apple use high-quality credits to tackle leftover emissions.

The Real Shift: Apple Is Redesigning How Electronics Are Made

Apple’s recent report shows a clear direction for tackling its environmental footprint. The company is no longer treating sustainability as an external offset mechanism. Instead, it is embedding it directly into product architecture.

The increase to 30% recycled materials in products shows a big change in how the tech giant makes things. Key parts, like cobalt and aluminum, are almost entirely made from recycled content. Robotics-driven recycling systems reinforce this direction, creating a closed-loop system where old devices feed directly into new production.

At the same time, Apple’s emissions profile shows both progress and constraint. Reductions are real, but scaling global hardware production means absolute emissions remain significant.

Still, the direction is clear. Apple is moving away from linear electronics manufacturing and toward a circular model where materials are continuously recovered, reused, and reintroduced into production.

In doing so, it is reshaping what sustainability looks like in the global tech industry — not as an add-on, but as a design principle built into the product itself.

Disseminated on behalf of Alaska Energy Metals Corporation.

The electric vehicle (EV) revolution is unfolding at full speed. EV sales, battery factories, and electrification plans are all increasing rapidly across the world. But behind this clean‑energy success story lies a growing risk that few people fully grasp: the supply of high‑purity nickel — known as Class 1 nickel — is under increasing strain.

While overall nickel output appears large, the specific kind of nickel that powers EV batteries is far harder to secure. Add in rising geopolitical tensions and energy price shocks, and the result is a supply chain that is both fragile and critical.

Nickel’s Role in the EV Revolution

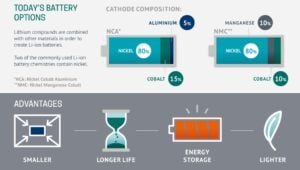

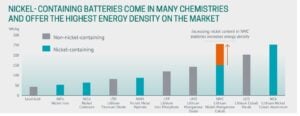

Nickel is a key ingredient in the lithium‑ion batteries that power most long‑range electric vehicles. Modern battery chemistries like NMC (Nickel‑Manganese‑Cobalt) and NCA (Nickel‑Cobalt‑Aluminum) use large amounts of nickel because it improves energy density, which helps EVs travel farther on a single charge.

As a result, demand for nickel from EV batteries is soaring. IRENA data suggested that global demand for nickel used in EV batteries could reach more than 1.09 million tonnes by 2030 under current trends, depending on battery technology and adoption rates.

As per analysts and industry pundits, as EV markets grow across the U.S., Europe, China, and other regions, this nickel demand is only expected to rise further. What makes this particularly challenging is that EV battery producers only accept Class 1 nickel — nickel that is at least 99.8% pure and suitable for conversion into nickel sulfate, which is essential for battery cathodes.

Why Class 1 Nickel Is Scarce

On the surface, the global nickel supply seems large. Countries like Indonesia have rapidly increased production, and numerous mines operate in Asia, Russia, and Latin America. But most of this nickel is Class 2, a lower‑purity type used mainly in stainless steel production, which cannot easily or cheaply be turned into battery‑grade material.

This means the world may have enough nickel in total, but the kind that matters most to the EV industry is limited. This structural imbalance between total output and battery‑grade supply is now one of the EV sector’s biggest supply challenges.

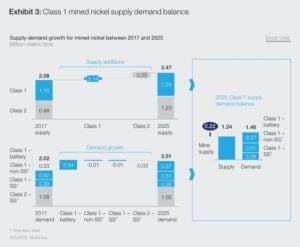

According to McKinsey, Class 1 supply growth is lagging demand growth. Some analysts project that even by 2025, primary Class 1 capacity may only supply around 1.2 million tonnes, compared with demand closer to 1.5 million tonnes, indicating a shortfall right when EV adoption accelerates.

Geopolitics is also heightening uncertainty. Russia, historically one of the largest producers of high‑grade nickel, saw its exports disrupted after the Ukraine war began. Sanctions and shifting trade relationships have forced automakers and battery makers to look for alternatives.

Meanwhile, an analysis from S&P Global explained how instability in the Middle East may not directly affect nickel mining, but it does influence everything from energy costs to shipping routes. Critical passages like the Strait of Hormuz handle significant volumes of global oil and gas. Any disruption there can increase fuel prices, which raises costs throughout the mining, refining, and logistics chain.

Since nickel production and refining are energy‑intensive, rising energy costs feed directly into higher production costs. In this way, even conflict far from nickel mines can tighten the Class 1 supply chain.

Processing Bottlenecks Drive Hidden Risk

Another often overlooked factor is processing. Much of the world’s nickel comes from lateritic ores, especially in Indonesia and the Philippines. To turn these ores into battery‑ready nickel sulfate requires a complex High‑Pressure Acid Leach (HPAL) process that depends heavily on sulfuric acid and stable energy inputs.

Disruptions to sulfur supply — linked closely to global energy markets — can slow down or increase the cost of HPAL operations. Analysts have highlighted that future price swings in battery‑grade nickel could be driven not just by ore availability but by these processing input risks tied to sulfur and acid supply.

So even if mines produce enough nickel ore, the ability to convert it into usable battery material can become the real bottleneck.

A Two‑Tier Nickel Market

As a result of these pressures, the nickel world is dividing into a clear two‑tier market:

A surplus of lower‑grade Class 2 nickel

A shortage of high‑purity Class 1 nickel demanded by EV makers

This gap is expected to grow as EV battery demand rises more sharply than Class 1 production capacity. Data from IEA shows that demand for nickel in cleantech applications, mainly EVs, could more than double from around 560 kilotonnes in the early 2020s to over 1,349 kilotonnes by 2030.

Source: IEA

Yet most new refining capacity is focused on processing laterite ores, and planned Class 1 expansions are relatively limited. This makes high‑purity nickel increasingly strategic.

Tight Battery Nickel Amid Shifting Market Trends

The same S&P report has emphasized this imbalance as a core structural challenge in the nickel market. While overall nickel supply may at times appear ample, the availability of battery‑grade nickel remains tight and vulnerable to both demand shifts and supply disruptions.

Furthermore, tracking the broader nickel market trends showed that industrial demand dynamics and tariff uncertainty have at times weighed on prices, even as battery‑grade demand continues to grow.

This mixed picture of soft prices amid growing strategic demand underscores how complicated the nickel supply story has become.

The Rising Value of Sulphide Nickel in North America

Not all nickel sources are equal. Sulphide nickel deposits — found in places like parts of Canada, Australia, and Alaska — are much easier to process into high‑purity Class 1 material than laterites. They also tend to have lower emissions and simpler refining paths.

Sulphide Nickel: Scarce but Strategic

Not all nickel sources are equal. Sulphide nickel deposits found in places like parts of Canada, Australia, and Alaska are much easier to process into high‑purity Class 1 material than laterites. They also tend to have lower emissions and simpler refining paths.

However, sulphide deposits are rare compared with laterite ores. Most of the easy‑to‑develop sulphide assets have already been mined. Discoveries are limited, making existing and new sulphide projects more strategically valuable.

This is why automakers and governments in Western countries are placing greater attention on domestic and North American projects as they seek to reduce reliance on geopolitically sensitive supply chains.

Alaska Energy Metals’ Nikolai Project and Cleaner Supply Chains

A high‑profile case is the Nikolai project in Alaska, developed by Alaska Energy Metals Corporation or AEMC. It contains not just nickel but also copper, cobalt, and platinum group metals — all important for EV batteries and broader clean energy technologies.

Projects like this offer several key advantages:

Cleaner processing pathways

Simpler conversion to battery‑grade nickel

Stronger environmental, social, and governance (ESG) transparency

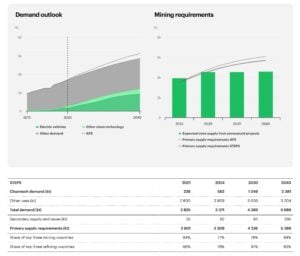

As of March 10, 2025, the nickel junior shows a major increase in contained metals. The resource estimate also confirms the presence of a treasure trove of energy transition metals: copper, cobalt, platinum, and palladium.

The Indicated category now includes 5.6 billion pounds of nickel and 1.77 billion pounds of copper, and along with the value of the other metals equal to 11.03 billion pounds of nickel equivalent metal. This marks a 46% increase from the previous estimate.

The Inferred category holds 9.38 billion pounds of nickel and 2.43 billion pounds of copper, and along with the value of the other metals equal to 17.98 billion pounds of nickel equivalent metal. This represents a sharp 122% increase, highlighting the scale of new resource growth.

Source: AEMC

As automakers push to decarbonize their supply chains, these attributes are becoming more valuable, not just economically but also in regulatory and brand terms.

Friendshoring and Supply Security

The concept of “friendshoring” — sourcing critical materials from politically stable and allied regions — is gaining traction. Governments in the U.S., Europe, and elsewhere are funding and incentivizing projects that can produce strategic minerals like nickel in safer jurisdictions.

This shift aligns with national security goals as well as corporate sustainability targets. Securing battery metals in friendly regions helps reduce exposure to conflicts and sanctions while supporting long‑term industrial planning.

Outlook: Quality Over Quantity

In the early days of the EV transition, the focus was simply on increasing battery production. Today, the conversation has shifted. It is no longer enough for the world to produce more nickel — it must produce the right kind of nickel.

High‑purity, battery‑grade nickel is becoming one of the most strategic materials in the energy transition. Its supply chain is deeply influenced by geopolitics, processing challenges, and shifting industrial priorities.

Conflicts like the Russia‑Ukraine war, energy price shocks, and sulfur supply vulnerabilities have all shown how fragile the nickel ecosystem can be. At the same time, demand projections through 2030 make it clear that EV adoption will continue pushing nickel demand higher.

DISCLAIMER New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Alaska Energy Metals Corp. (“Company”) made a one-time payment of $90,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: .

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-04-20 11:15:072026-04-20 11:15:07EV Batteries Need Nickel: Why Class 1 Supply Is Becoming Critical Amid Global Conflict

On April 18th, Reuters reported that the U.S. direct air capture (DAC) sector received a major boost after the Department of Energy (DOE) decided to retain funding for two flagship carbon removal hubs originally backed under the Biden administration.

The move removes months of uncertainty and protects more than $1 billion in federal support for the South Texas DAC Hub and Louisiana’s Project Cypress. The decision also reinforces that carbon removal remains part of the United States’ long-term climate and industrial strategy, even as policy priorities evolve.

From Funding Risk to Revival: DOE Keeps Landmark Direct Air Capture Hubs Moving Forward

The Department of Energy had previously placed several clean energy awards under review, including major carbon capture, hydrogen, and industrial decarbonization projects. Among the most closely watched were the two large DAC hubs in Texas and Louisiana, both of which risked losing federal backing.

South Texas DAC Hub, developed with Occidental’s carbon management arm 1PointFive, holds a $500 million federal award.

Project Cypress in Louisiana received $550 million in support.

Although both projects were awarded significant funding, only an initial $50 million tranche had been disbursed so far, leaving most capital still pending deployment.

Once fully operational, both facilities are expected to remove more than 2 million metric tons of CO₂ annually from the atmosphere. That scale places them among the most ambitious carbon removal projects globally and positions the United States as a leader in early DAC commercialization.

Energy Secretary Chris Wright noted that the agency retained projects with credible delivery pathways following extensive review discussions with applicants. The DOE’s Hydrocarbons Geothermal and Energy Office will now help guide next steps, including fund disbursement and project execution.

U.S. Direct Air Capture Market Gains Policy and Investment Support

The funding confirmation strengthens confidence across the growing U.S. DAC ecosystem, which depends heavily on long-term policy signals and federal incentives.

The country already leads global carbon removal development, supported by programs such as the $3.5 billion DAC Hubs initiative and the Section 45Q tax credit, which can provide up to $180 per ton for permanent carbon storage under current structures.

In parallel, corporate demand for high-quality carbon removals continues to expand. Technology firms, airlines, and industrial players are signing long-term agreements to secure carbon removal supply, reflecting a shift from low-cost avoidance credits toward durable carbon storage solutions.

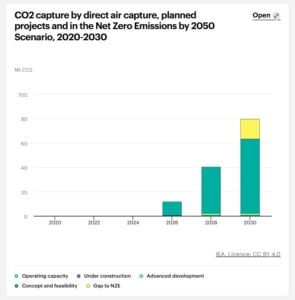

According to the International Energy Agency (IEA), more than 130 large-scale DAC facilities are now in development globally, with the United States holding a significant share of planned capacity. This pipeline highlights growing commercial interest even as the technology remains in its early deployment phase.

At the same time, regional DAC clusters are beginning to take shape. West Texas, for example, has emerged as a leading hub due to its combination of renewable energy access, subsurface storage potential, and industrial infrastructure. Projects like STRATOS, targeting 500,000 tons of annual CO₂ capture, illustrate how scaling could evolve through concentrated deployment.

Source: IEA

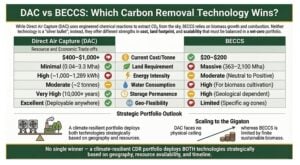

DAC Cost Challenges and Fuel Market Link Drive Long-Term Outlook

Despite strong policy backing, cost remains the most significant barrier for direct air capture expansion. Current estimates place DAC costs between $500 and $1,000 per ton of CO₂ removed, depending on technology type, energy sourcing, and storage logistics. While costs are expected to decline with scale and innovation, near-term economics remain challenging.

From Carbon Credits to SAF, DAC’s Business Case Is Getting Stronger

However, the value proposition is expanding beyond carbon credits. Captured CO₂ is increasingly viewed as a potential feedstock for synthetic fuels, including sustainable aviation fuel (SAF). This integration could improve project economics while also supporting fuel supply diversification.

Recent geopolitical tensions affecting global oil markets have added further urgency to alternative fuel development. In this context, DAC-linked synthetic fuel production could play a dual role by reducing emissions while supporting energy security.

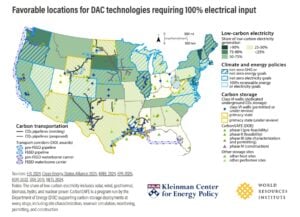

Texas and Louisiana Lead the Transition

Texas and Louisiana are particularly well-positioned for this transition. Both states offer strong industrial infrastructure, access to geologic storage formations, and proximity to energy and chemical industries. Texas also benefits from expanding renewable energy capacity, which is important for powering energy-intensive DAC systems.

Even so, scaling from today’s million-ton projects to gigaton-scale removal pathways will require sustained investment, policy support, and continued technological improvements. Some research suggests that large-scale DAC deployment may still require carbon prices or subsidies above $200 per ton for economic viability in the early phases.

Thus, the DOE’s decision to keep funding for the South Texas and Louisiana DAC hubs signals stability for a sector still shaping its commercial future. While cost and scale challenges remain, rising demand, broader policy support, and growing industrial interest suggest DAD is moving from experimental climate technology toward early-stage infrastructure development in the United States.

Australia’s reformed Safeguard Mechanism is reshaping how large industrial emitters manage carbon. The policy, updated in 2023, sets declining emissions limits for the country’s biggest facilities, including mining and energy operations. Companies that exceed their baselines must either cut emissions or purchase carbon credits.

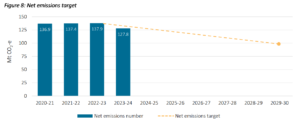

This has triggered a sharp rise in demand for Australian Carbon Credit Units (ACCUs). According to the Australian government, the Safeguard Mechanism covers about 215 facilities, responsible for roughly 28% of Australia’s total greenhouse gas emissions. These sites must collectively reduce emissions by 4.9% per year through 2030.

Instead of cutting emissions immediately, many companies are turning to carbon credits to stay compliant. This includes major players like Rio Tinto and Woodside Energy, which are among the largest emitters in the system.

Mining Giants are the Biggest Buyers of Australia’s Carbon Credits

The mining and energy sectors dominate Australia’s emissions profile. Together, they account for a large share of industrial output and carbon intensity.

Under the Safeguard Mechanism, companies can use ACCUs or Safeguard Mechanism Credits (SMCs) to offset emissions above their limits. This flexibility has led to a surge in credit purchases. Moreover, entities covered by this scheme must cut net emissions to 100 MtCO2-e by 2029–30.

Source: Australian Government Clean Energy Regulator

The ACCU Scheme supports projects that either reduce emissions or remove carbon from the atmosphere. These projects aim to:

Enhance vegetation for better carbon storage.

Adjust land practices to reduce emissions.

Upgrade equipment to lower energy use and methane output.

Project developers earn one ACCU for every tonne of CO₂-equivalent emissions avoided or stored. These credits can then be sold to companies or governments, creating a financial incentive for emissions reduction.

The scheme continues to expand. In November 2024, a new reforestation method was introduced. This new approach builds on past models. It supports projects that boost carbon storage through environmental or mallee plantings.

Activity in the market has been strong. In 2024–25, over 380 new project applications came in, and 1,183 crediting applications were processed.

Source: Australian Government Clean Energy Regulator

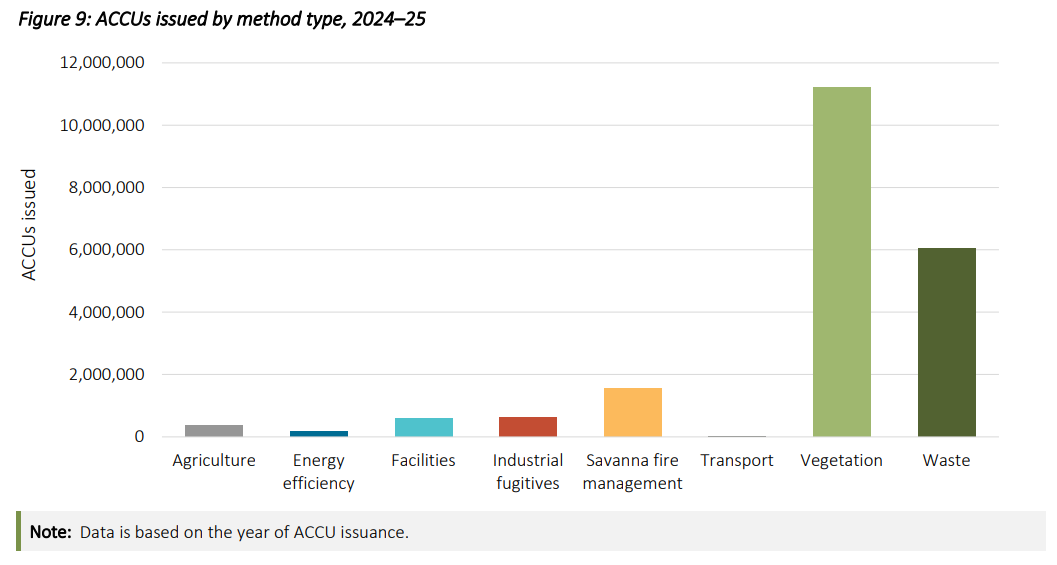

Credit supply has also reached new highs. A record 20.6 million ACCUs were issued in 2024–25, up from 18.7 million the year before. Over half of these credits—about 54%—came from vegetation projects. Meanwhile, 29% were from waste-related projects.

At the same time, spot prices are currently around AUD $30 to $35 per ton and are expected to stay relatively stable through 2028. However, the government’s cost containment price, used for companies facing higher emissions obligations, is much higher, set at $82.68 for 2025–26.

This imbalance reflects a broader trend. Companies are using credits as a short-term solution while longer-term decarbonization projects take time to develop.

Rio Tinto’s Tightrope: Balancing Cuts and Offsets

Rio Tinto is one of the world’s largest mining companies and a major emitter in Australia. The company has set a target to cut Scope 1 and 2 emissions by 50% by 2030, using a 2018 baseline. It also aims for net-zero emissions by 2050.

Source: Rio Tinto

To reach these goals, Rio Tinto is investing in renewable energy, electrification, and low-carbon technologies. For example, it is developing large-scale solar and battery projects to power its iron ore operations in Western Australia.

However, emissions reductions in mining are complex. Heavy equipment, remote locations, and energy-intensive processes limit how fast emissions can fall. As a result, Rio Tinto has also used carbon credits to manage near-term compliance under the Safeguard Mechanism.

The mining giant retired 1.1 million ACCUs in 2024 and plans to scale it to 3.5 million credits annually by 2030.

The use of credits reflects a broader strategy. The company combines direct emissions cuts with offset purchases to stay within regulatory limits while transitioning operations over time.

Woodside’s Climate Dilemma: Oil, Gas, and the Offset Dependence

Woodside Energy faces similar challenges. As Australia’s largest independent oil and gas company, it operates in a high-emission sector with limited short-term alternatives.

Woodside has set a target to reduce net equity Scope 1 and 2 emissions by 30% by 2030, based on a 2020 baseline. It also aims for net zero by 2050.

Source: Woodside Energy

The company plans to invest in carbon capture and storage (CCS), hydrogen, and renewable energy. However, these technologies are still scaling.

In the meantime, Woodside has relied on carbon credits to offset emissions. This includes purchasing ACCUs to meet compliance requirements and support its climate targets. This approach highlights a key issue. For sectors like oil and gas, offsets remain a major tool in the transition.

Carbon Markets Are Growing—But Trust Issues Are Growing Too

Australia’s carbon market is growing, but it faces ongoing scrutiny. The Clean Energy Regulator oversees ACCU issuance and compliance, aiming to ensure credit quality and transparency.

At the same time, independent reviews have raised concerns about the integrity of some nature-based credits. This has led to tighter rules and increased oversight.

Globally, similar trends are emerging. According to the World Bank, carbon pricing mechanisms now cover about 24% of global emissions, with carbon prices ranging widely across regions.

In voluntary markets, demand is shifting toward higher-quality credits. Buyers are prioritizing projects with clear, verified emissions reductions and long-term impact. However, supply remains limited. This creates price pressure and increases competition for high-integrity credits.

Offsets vs Real Cuts: The Debate Behind Net Zero Strategies

Offsets play a growing role in corporate climate strategies, especially for hard-to-abate sectors. But they are not a complete solution.

Most net-zero frameworks require companies to reduce emissions first, then use carbon offsets only for residual emissions. This principle is reflected in global standards such as the Science Based Targets initiative (SBTi).

Still, the reality is more complex. Large industrial companies often face technical and economic limits on how fast they can decarbonize. As a result, many firms use a mix of strategies: