SBTi Hits 10,000 Companies with Validated Targets in 2026: Asia Fuels the Net-Zero Momentum

Corporate climate action is no longer a niche effort. It is now a core business strategy. Fresh data from the Science Based Targets initiative (SBTi) confirms this shift. By January 2026, nearly 10,000 companies had validated science-based targets. Even more striking, over 12,000 firms had either set or committed to setting these goals by the end of 2025.

This momentum reflects a clear trend. Companies are aligning faster with climate science. They are also embedding net-zero goals into long-term planning. Despite economic uncertainty, the pace of adoption continues to rise. That signals a structural change in how businesses view emissions, risk, and growth.

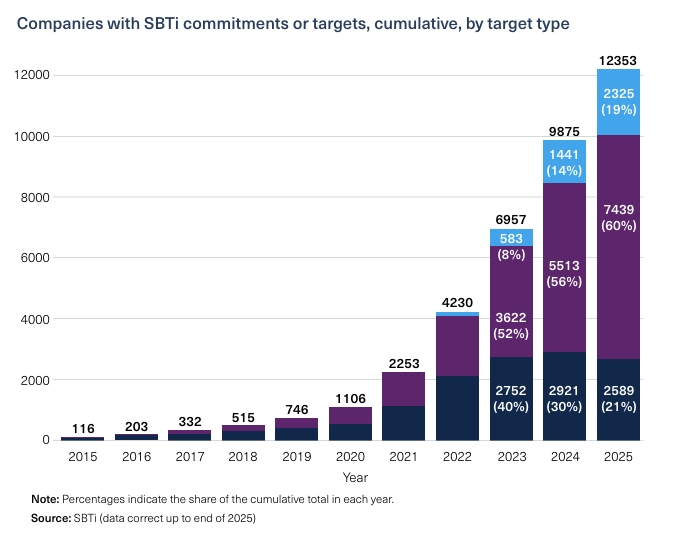

Rapid Rise: 2025 Marks a Breakout Year

The year 2025 stands out as a major growth phase. The number of companies with validated science-based targets increased by 40% year over year. At the same time, firms adopting both near-term and net-zero targets surged by 61%.

Target-Setting Critical Mass: Global Growth of Companies with Validated

Targets and Active Commitments

These numbers tell a simple story. Businesses are not just making promises. They are moving toward validated, science-backed action. Interestingly, the number of companies that only committed to targets remained stable. This suggests a shift away from pledges toward measurable progress.

As a result, the SBTi crossed a major milestone in early 2026. It surpassed 10,000 validated companies. That achievement highlights how quickly climate accountability is becoming mainstream.

Asia Takes the Lead: A New Growth Engine

While Europe still dominates in total numbers, Asia is now the fastest-growing region. In 2025 alone, the region recorded a 53% increase in companies with validated targets. This growth puts Asia on par with Europe in terms of expansion speed.

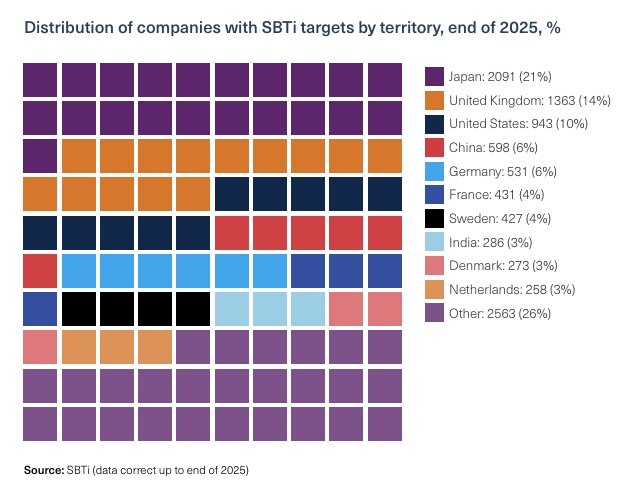

Countries like China, Japan, Taiwan, and India led among high-penetration markets. At the same time, emerging economies such as Indonesia, Pakistan, Singapore, Thailand, and South Korea showed strong gains. These markets are moving quickly from low adoption to rapid scaling.

Refer to the chart below to understand the current shift.

Asian Territories’ Target-Setting Cements: High Penetration Markets Continue

to Dominate, Lower Penetration Territories Become More Prominent

This shift matters. It shows that climate ambition is no longer concentrated in Western economies. Instead, it is spreading across emerging markets. As supply chains globalize, this broader participation strengthens overall impact.

Meanwhile, other regions are not far behind. Africa grew by 48%, while Latin America and the Caribbean saw a 42% rise. Europe still holds the largest share, accounting for 49% of all targets. Asia follows with 36%, and North America trails at 11%.

Market Leaders: Who Is Driving Adoption?

Some countries and markets stand out. Japan leads globally with over 2,000 companies holding validated targets. The United Kingdom and the United States follow behind.

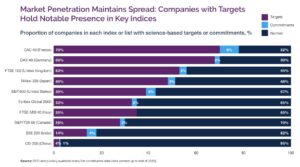

In financial markets, Europe shows the strongest penetration. Major indices such as France’s CAC 40, Germany’s DAX 40, and the UK’s FTSE 100 lead adoption. These benchmarks reflect how deeply climate goals are embedded in European corporate strategy.

However, global benchmarks like the Nikkei 225 and S&P 500 are catching up. The Forbes Global 2000 also shows rising participation. This indicates that the world’s largest companies are increasingly aligning with science-based frameworks.

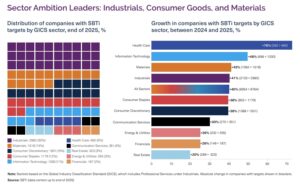

Sector Momentum: Healthcare, Tech, and Materials Step Up

Growth is not limited to regions. It is also spreading across industries. In 2025, healthcare led sectoral expansion. This is notable because the sector has traditionally been slower to decarbonize.

At the same time, information technology and materials sectors showed strong momentum. These industries play a key role in global supply chains. Their progress can drive wider emissions reductions across multiple sectors.

This trend highlights an important point. Climate action is no longer confined to energy or heavy industry. It now spans both service-based and industrial sectors. That broad participation increases the chances of meeting global climate goals.

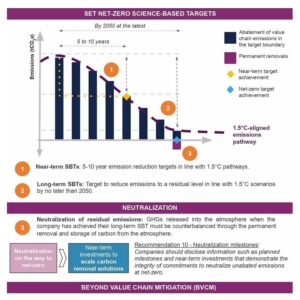

Understanding the Net-Zero Standard: A Clear Framework

The key pillar of this growth is the SBTi’s Corporate Net-Zero Standard. This framework gives companies a structured way to set and achieve net-zero targets.

The standard focuses on alignment with climate science. Specifically, it requires companies to follow pathways consistent with limiting global warming to 1.5°C. That ensures targets are not just ambitious, but also credible.

To reach net zero, companies must do two things. First, they must deeply reduce emissions across their operations and value chains. This includes Scope 1, 2, and 3 emissions. Second, they must address any remaining emissions through permanent neutralization.

In simple terms, net zero is not about offsetting everything. It is about cutting emissions as much as possible first. Only then can companies neutralize the small amount that remains.

Four Pillars of Corporate Net Zero

The SBTi framework is built on four key elements. Together, they define a complete net-zero strategy.

First, companies must set near-term targets. These drive immediate emissions reductions. Second, they need long-term targets that align with net-zero timelines. These ensure sustained progress.

Third, companies must neutralize residual emissions. This step addresses emissions that cannot be eliminated. Finally, firms are encouraged to go beyond their value chains. This is known as beyond value chain mitigation (BVCM).

BVCM includes actions like investing in climate solutions outside a company’s direct operations. While not mandatory, it plays a critical role in supporting global climate goals.

Why This Growth Matters Now

The rapid rise in science-based targets signals a deeper shift. Climate action is becoming a standard part of business strategy. It is no longer driven only by regulation or reputation.

Instead, companies see clear benefits. These include risk management, investor confidence, and long-term resilience. As a result, climate targets are now tied to financial and operational decisions.

Moreover, the growing alignment across regions and sectors increases impact. When more companies follow the same science-based approach, collective progress accelerates.

Challenges Ahead: Growth Meets Complexity

Despite strong momentum, challenges remain. Setting targets is only the first step. Delivering real emissions reductions is far more complex.

Companies must deal with supply chain emissions, technology gaps, and policy uncertainty. In addition, measuring and verifying progress can be difficult.

However, the structured approach of the SBTi helps address these issues. Providing clear guidance reduces confusion and improves consistency. That makes it easier for companies to move from ambition to action.

The Bottom Line: From Momentum to Mainstream

David Kennedy, Chief Executive Officer of the Science-Based Targets initiative, said:

“There is clear evidence about the business benefits of science-based target-setting—this is a key lever for companies to manage transition risk and strengthen business resilience, remaining competitive now and in the future. The data in this report shows that despite political headwinds, increasing numbers of companies in every region are setting science-based targets. In doing so they are part of a market transformation that is good for business while contributing to achieving global climate objectives.”

In conclusion, the latest data paints a clear picture. Corporate climate action is scaling rapidly. With nearly 10,000 validated companies, the SBTi milestone marks a new phase.

More importantly, growth is no longer limited to a few regions or sectors. It is global, diverse, and accelerating. Asia’s rise, sector-wide adoption, and strong frameworks all point in the same direction.

Looking ahead, the focus will shift from target-setting to execution. Companies will need to turn commitments into measurable results. If they succeed, the current momentum could drive real progress toward global net zero.

In short, the era of climate pledges is fading. The era of climate delivery has begun.

The post SBTi Hits 10,000 Companies with Validated Targets in 2026: Asia Fuels the Net-Zero Momentum appeared first on Carbon Credits.