Singapore and World Bank Launch New Carbon Markets Programme to Scale High-Integrity Climate Finance

The Singapore government and the World Bank Group have launched a new Singapore Carbon Markets Programme to help countries build stronger, more transparent carbon markets.

The initiative was launched at the Innovate4Climate conference in Singapore this week. This is a key step in Singapore’s goal to be a top global carbon trading hub. It also helps developing countries access climate finance through high-quality carbon credits.

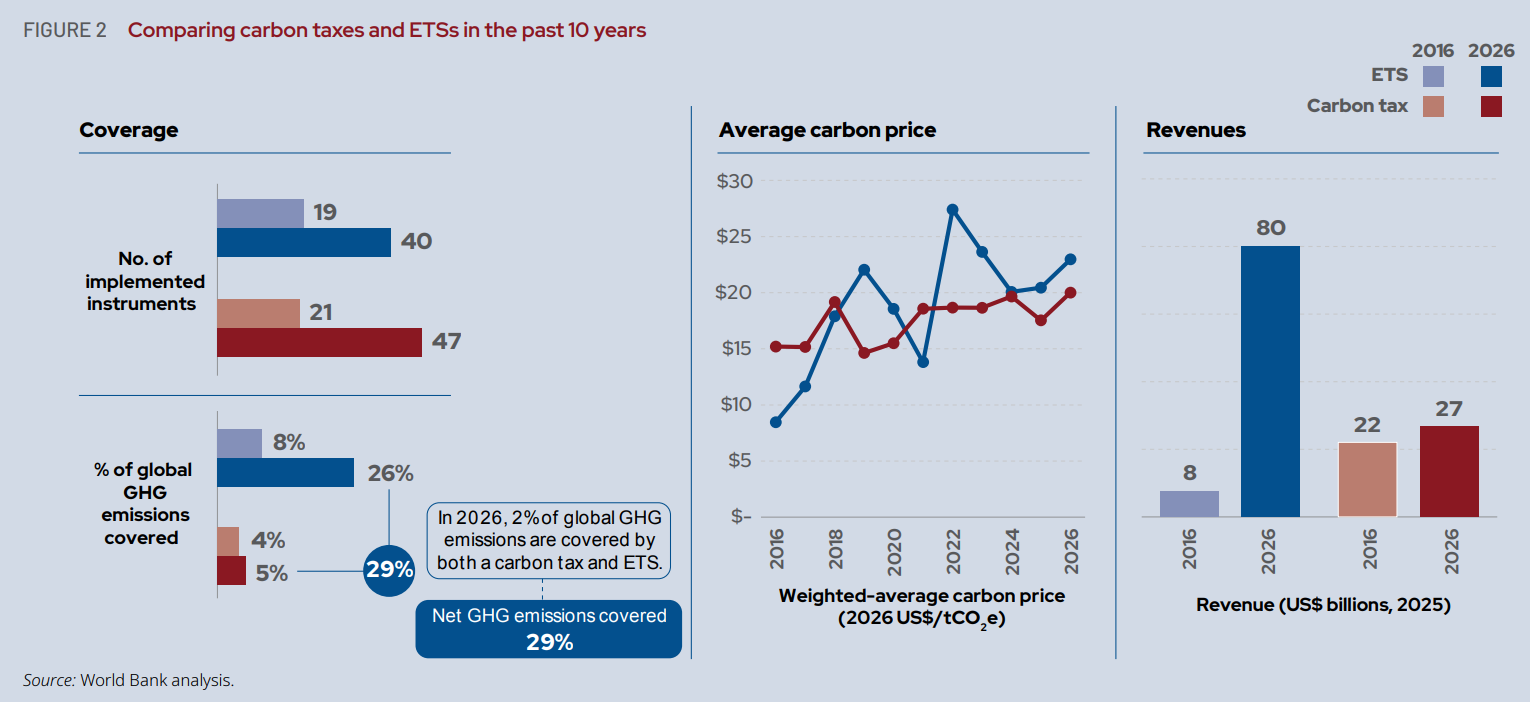

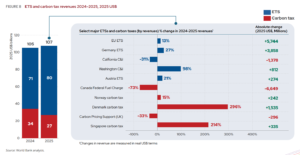

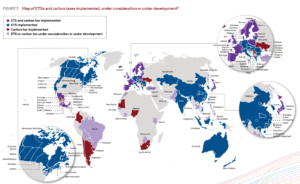

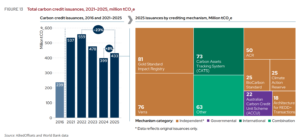

This program arrives as global carbon markets grow quickly. The World Bank’s latest report, State and Trends of Carbon Pricing 2026, shows that carbon pricing now covers nearly 30% of global greenhouse gas emissions. This includes 87 policies worldwide.

Carbon pricing revenues surpassed $107 billion in 2025, more than tripling what was recorded a decade ago.

Singapore Carbon Credit Market Size and Share Analysis – Growth Trends and Forecasts (2025-2032)

Singapore Wants to Build Trusted Carbon Markets

The program addresses key issues that slow down global carbon market growth. These issues are:

- weak infrastructure

- faulty registry systems,

- limited financing,

- doubts about carbon credit quality

Singapore and the World Bank will help countries improve their technical systems. They will boost institutional capacity and build the digital infrastructure needed for reliable carbon trading.

Kristina Svensson, East Asia and Pacific Regional Hub Manager, World Bank Group, said:

“This partnership reflects our commitment to deliver tangible development outcomes by providing meaningful access to climate finance to the countries that need it most. It reinforces our strategic alignment with the Government of Singapore to build high-integrity carbon markets.”

The programme has three main pillars.

1. Building Better Carbon Market Infrastructure

The first component aims to improve carbon market technology and infrastructure.

The program will create toolkits for countries. These toolkits will help build carbon registries that meet international standards. Registries are vital. They track the creation, ownership, and retirement of carbon credits, preventing double-counting.

- The initiative will support digital monitoring, reporting, and verification (MRV) systems.

- It will include new project types like regenerative agriculture and nature-based carbon removal.

Digital MRV systems are essential. Buyers want high-quality credits with clear transparency and traceability. Better systems can enhance data collection and lower costs for project developers.

Singapore has become a tech-driven carbon market hub. It is a founding partner of the Climate Action Data Trust (CAD Trust), a blockchain platform that links carbon registry data and boosts market transparency.

The country helped launch CAD Trust with the World Bank Group and the International Emissions Trading Association.

2. Helping Carbon Credit Buyers and Sellers Connect

The second part of the programme aims to improve access to financing and increase carbon credit transactions.

Many carbon projects in developing countries struggle to secure buyers because transaction costs remain high and market risks discourage investment.

The programme will also explore new ways to connect carbon credit buyers and sellers at both company and country levels. This could lower project risks, reduce transaction costs, and bring more private investment into carbon projects in developing markets.

The World Bank believes stronger carbon markets can help unlock billions of dollars in climate finance for emerging economies. Over the years, the institution has supported several carbon finance programs, emissions trading systems, and climate investment projects around the world.

3. Supporting Countries With Carbon Market Readiness

The third pillar focuses on helping governments build carbon market readiness.

The programme will assist countries in designing national carbon market strategies, policies, and institutions. It will also encourage cross-country learning and collaboration.

This is especially important as more developing nations prepare for international carbon trading under Article 6 of the Paris Agreement.

Countries are increasingly exploring carbon taxes and emissions trading systems to meet climate targets while generating public revenues. The World Bank reported that all major middle-income economies have now either implemented or are planning direct carbon pricing instruments.

Jamie Fergusson, Director for Climate, World Bank Group, further emphasized,

“Carbon markets can become a source of climate finance for developing countries, but only if countries have the infrastructure, market confidence, and technical capacity to participate with integrity.”

Singapore Expands Its Global Climate Role

Singapore has become one of Asia’s largest carbon market hubs. The country introduced Southeast Asia’s first national carbon tax in 2019.

- The tax applies to large facilities that produce at least 25,000 tonnes of greenhouse gas emissions each year.

- It has also attracted exchanges, project developers, verification firms, and financial institutions working in carbon markets.

Singapore is co-leading the Coalition to Grow Carbon Markets with the UK and Kenya. This initiative boosts demand for high-quality carbon credits in voluntary and Article 6 markets.

The city-state views carbon markets as a key economic opportunity while advancing its net-zero goals.

Its strategic location and robust financial sector make it ideal for global carbon trading. Strong regulations support this, too. Singapore Exchange (SGX) and Climate Impact X are building trading systems for carbon products in Asia.

Carbon Markets Continue to Grow Globally

Carbon markets are becoming a central tool in global climate policy despite ongoing concerns over credit quality and transparency.

- The World Bank estimates that nearly one-third of global emissions could soon be covered by carbon pricing if planned systems in countries like Brazil and Türkiye move forward.

- Meanwhile, global emissions trading systems generated a record $79 billion in revenues in 2025, according to the International Carbon Action Partnership (ICAP).

Experts say stronger infrastructure and trusted governance will be critical if carbon markets are to scale effectively and deliver real climate benefits.

High-Quality Carbon Credits Gain Momentum

At the same time, premium prices continue to emerge for higher-quality credits, especially nature-based removals and forestry projects with stronger verification standards.

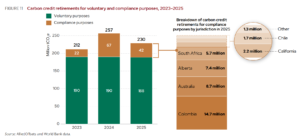

Supporting the above analysis, Sylvera has also revealed that the voluntary carbon market is evolving rapidly and is increasingly shifting from volume to quality. The key highlights of the report were:

- The company reported that 168 million carbon credits were retired in 2025. The total market value grew 6% to $1.04 billion, even with lower trading volumes.

- High-quality credits were scarce. Corporate buyers preferred trusted, high-integrity projects.

- By 2027, compliance-driven demand may surpass voluntary market demand. Programs like CORSIA and stricter global carbon rules are growing around the world.

The new Singapore Carbon Markets Programme aims to fill key gaps. It also places Singapore and the World Bank at the heart of the next phase of global carbon market growth.

On an end note, Benedict Chia, Director-General (Climate Change), National Climate Change Secretariat, said:

“Singapore is committed to advancing high-integrity carbon markets as a key pillar of both global climate action and sustainable development. Our collaboration with the World Bank Group on the Singapore Carbon Markets Programme reflects this commitment. We hope this programme will strengthen confidence in the global carbon market and help ensure that host countries can meaningfully participate in and benefit from it.”

The post Singapore and World Bank Launch New Carbon Markets Programme to Scale High-Integrity Climate Finance appeared first on Carbon Credits.