Meta Platforms and US-based D. E. Shaw Renewable Investments (DESRI) signed new renewable energy agreements totaling 850 megawatts (MW) in 2026. The deals include 500 MW in Oklahoma, 200 MW in Texas, and 150 MW in Mississippi. These agreements are part of Meta’s broader effort to power its growing data center and AI operations with clean electricity.

The latest contracts push the total renewable energy partnership between Meta and DESRI to around 2,575 MW across nine U.S. states. The projects include solar power and battery storage systems that aim to strengthen grid reliability while lowering emissions from electricity use.

Hy Martin, Chief Development Officer of DESRI, said:

“Our energy infrastructure partnership with Meta now spans nine states and more than two and a half gigawatts across the country. These projects support Meta’s energy commitments, and they will generate significant economic development for local rural economies across the country. Our relationship with large companies like Meta is a cornerstone of DESRI’s long-term strategy of delivering cost-effective, reliable energy projects to power the U.S. economy’s growth.“

DESRI Expands Renewable Footprint Across the U.S.

DESRI expects around 1,110 MW of these contracted projects to begin construction this year. Each project is likely to create hundreds of temporary construction jobs and generate long-term economic benefits for local communities through taxes, land lease payments, and operational spending.

The company has become one of the largest renewable energy developers in the United States.

Its portfolio now includes more than 80 solar, wind, and energy storage projects with a combined capacity exceeding 12 gigawatts. The company develops, finances, owns, and operates utility-scale renewable projects across the country.

Significantly, it also includes community programs in many of its agreements. DESRI regularly allocates funding for high school scholarships focused on clean energy careers. Similar education initiatives are expected in several states tied to the new Meta projects.

Amanda Yang, Head of Clean and Renewable Energy at Meta, noted:

“DESRI has been a valued partner as we work to bring new energy to grids across the United States. This expanded partnership — now spanning nine states — reflects our commitment to supporting the communities where we operate,” said

Big Tech Continues to Dominate Clean Energy Buying

The announcement reflects a larger trend shaping global energy markets. Large technology companies have become the biggest buyers of renewable electricity as artificial intelligence infrastructure expands rapidly.

According to BloombergNEF, companies such as Meta, Amazon, Google, and Microsoft accounted for nearly half of all global corporate clean energy purchase agreements in 2025.

The report showed that global corporate clean power purchase agreement volumes reached 55.9 GW in 2025. Although that represented a 10% decline from the previous year, it still marked the second-highest year ever recorded. The slowdown ended eight consecutive years of growth in corporate renewable energy contracting.

Meta Tops the List

Meta emerged as the world’s largest corporate clean energy buyer in 2025. The company signed contracts for 10.24 GW of clean electricity, narrowly surpassing Amazon’s 10.22 GW. Most of Meta’s activity remained concentrated in the United States, where demand for AI-ready data centers continues to grow quickly.

The report also revealed a major shift in energy procurement strategies. Instead of relying only on standalone solar or wind farms, large technology firms are increasingly moving toward “baseload-like” energy solutions. These systems combine multiple technologies to provide more stable electricity throughout the day and night

While large technology firms accelerated clean energy purchases, smaller companies slowed down significantly. BloombergNEF reported that the number of corporate clean energy buyers in the United States dropped sharply in 2025.

Despite U.S. clean energy agreement volumes reaching a record 29.5 GW, only 33 companies signed major contracts during the year. That number was nearly half the total recorded in the previous year.

Analysts linked the slowdown to policy uncertainty, changes in tax credit structures, and rising complexity in energy markets. Smaller businesses struggled to manage volatile electricity markets and long-term contract risks.

Nayel Brihi, lead author of BloombergNEF’s report, said corporate buyers are now operating at “two different speeds.” Large technology companies are signing bigger contracts and exploring advanced technologies, while smaller firms remain cautious about long-term commitments.

Hybrid Clean Energy Solutions Move into the Spotlight

Artificial intelligence has become one of the biggest drivers of electricity demand worldwide. Data centers require enormous amounts of constant power to support AI training models, cloud computing, and digital services.

As AI demand grows, companies are looking beyond traditional renewable projects toward systems capable of delivering electricity around the clock. This shift explains the rising interest in storage systems and hybrid renewable projects.

IRENA recently highlighted the growing role of firm renewable systems. It says hybrid projects can optimize grid connections, reduce exposure to price volatility, and deliver more stable electricity supplies.

Falling Battery Costs Make 24/7 Renewable Power More Viable

The economics of these systems are also improving rapidly. IRENA estimated the global average solar electricity cost at $0.043 per kilowatt-hour in 2024. Falling battery prices are making “anytime solar power” increasingly practical in regions with strong sunlight.

Studies now show that the levelized cost of electricity from hybrid solar-and-storage systems has dropped sharply over the past five years.

In strong solar and wind regions, costs fell from above $100 per megawatt-hour in 2020 to around $54–82 per megawatt-hour by 2025.

Analysts expect another major decline over the next decade. Under current technology trends, firm renewable electricity costs could fall by roughly 30% by 2030 and nearly 40% by 2035. In the best locations, costs may drop below $50 per megawatt-hour.

Source: IRENA

Meta Expands Its Renewable Energy Strategy

Meta has steadily increased investments in renewable electricity over the past several years. The company uses long-term power purchase agreements to match its electricity consumption with clean energy generation.

Under these agreements, developers build and operate renewable projects while Meta purchases the electricity produced. These long-term contracts help developers secure financing and move projects forward.

By the end of 2024, 89 of the 128 renewable projects in Meta’s portfolio were already online and supplying electricity to the grid.

The company often focuses on projects connected to the same electricity grids as its data centers. Meta also prioritizes projects that improve grid reliability and reduce emissions during periods of high electricity demand.

Reducing Operational Emissions

Meta reduced operational emissions by 6 million MT CO₂e in 2024. The company also uses Energy Attribute Certificates (EACs) to cut Scope 3 emissions linked to fuel use, consumer hardware, and remote work. This approach reduced value chain emissions by 1.4 million MT CO₂e in 2024.

To sum up, renewable energy procurement has helped Meta cut 23.8 million MT CO₂e emissions since 2021.

Some of Meta’s major solar and battery storage partnerships, including:

150 MW floating solar project in Singapore with Sembcorp Industries

Large solar power agreements in Ireland near Meta’s data center operations

Sky Ranch Solar Energy Center in New Mexico with NextEra Energy and PNM

AI Research Supports Energy Storage Innovation

Meta is also investing in advanced energy research using artificial intelligence tools. The company supports battery storage projects and scientific research focused on improving clean energy systems.

One major initiative is the Open Catalyst project, a collaboration between Meta’s Fundamental AI Research team and researchers at Carnegie Mellon University. The project aims to accelerate the discovery of new catalysts for clean energy production and storage.

Overall, Meta’s latest renewable agreements with DESRI show how quickly energy demand from AI infrastructure is reshaping electricity markets. Large technology firms are no longer simply buying renewable power to meet sustainability goals. They are increasingly driving the next phase of energy system development focused on reliability, storage, and round-the-clock clean electricity.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-05-15 09:15:122026-05-15 09:15:12Meta Platforms and D. E. Shaw Renewable Investments Expand 2.5 GW Renewable Partnership Across Nine U.S. States

Google’s parent, Alphabet Inc., is expanding its artificial intelligence (AI) infrastructure strategy on two fronts: securing massive renewable energy supplies on Earth and exploring future data centers in space.

The company just signed a 500-megawatt (MW) solar power deal in Texas with Linea Energy. This will help meet the rising electricity needs of its U.S. data centers.

Moreover, reports say Google is talking to SpaceX. They are discussing launching orbital data centers. This move comes as AI computing strains global energy systems.

The moves show how big tech companies are competing for long-term energy and computing power. This is happening as AI workloads grow quickly around the globe.

Google Signs 500 MW Solar Deal to Power AI Growth

Google’s new renewable energy deal includes 500 MW of solar power. This capacity comes from projects by Linea Energy in Texas. The electricity will power Google’s growing network of data centers and cloud infrastructure in the U.S.

Will Conkling, Director of Energy and Power, Google, noted:

“By collaborating with Linea Energy to bring new low-cost power to the grid, we are helping to ensure the Lone Star State’s energy system remains affordable for local families and businesses.”

The deal reflects a broader trend among hyperscale technology companies. AI systems require enormous amounts of electricity to train and run advanced models. This is creating growing pressure on power grids and increasing demand for renewable energy.

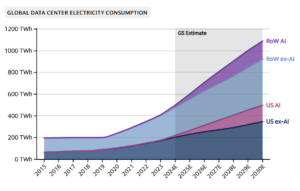

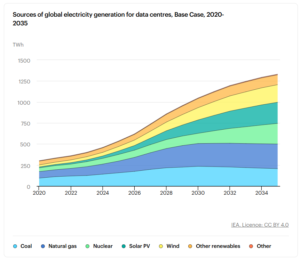

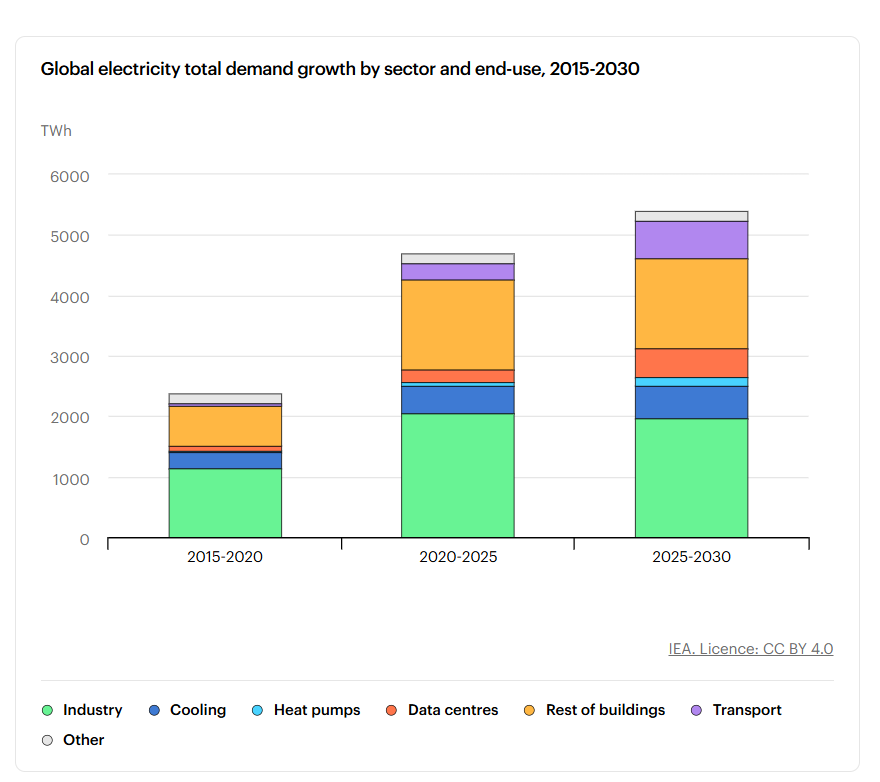

According to the International Energy Agency, global data center electricity consumption reached about 415 terawatt-hours (TWh) in 2024. The IEA expects this figure to more than double to roughly 945 TWh by 2030 as AI adoption accelerates.

Google has been one of the largest corporate buyers of renewable energy globally for several years. The company says it has signed more than 7 gigawatts of clean energy agreements worldwide since 2010.

The company also aims to operate on 24/7 carbon-free energy across all its global operations by 2030. Google’s goal is different from traditional renewable targets. Instead of matching yearly electricity use, it aims to provide clean electricity every hour of every day.

Texas is now a key area for this strategy. Its renewable energy capacity is growing fast, and the data center market is expanding. The state leads the U.S. in utility-scale solar additions and remains a major hub for AI infrastructure investment.

AI Is Driving a Massive Surge in Power Demand, Impacting Google’s Emissions

The rise of generative AI is reshaping global electricity markets. Training large AI models requires huge amounts of computing power. Running AI services continuously also increases electricity consumption across cloud platforms and data centers.

Goldman Sachs estimates global power demand from data centers could rise as much as 165% by 2030 due largely to AI growth. McKinsey & Company estimates that global demand for AI-ready data center capacity could require up to $8 trillion in infrastructure investment by 2030.

Source: Goldman Sachs

This has created a growing challenge for technology companies. Many regions already face delays in grid connections and shortages of reliable electricity supply.

As a result, companies such as Google, Microsoft, Amazon, and Meta Platforms are investing heavily in renewable energy, battery storage, nuclear power, and grid infrastructure.

The push for clean energy is also tied closely to corporate climate goals.

Google said its total greenhouse gas emissions increased by almost 48% from its 2019 baseline. This rise is mainly due to higher energy use from AI and data centers.

Source: Google

The company noted in its recent sustainability report that AI growth is making it harder to cut emissions. This explains why securing large-scale renewable electricity agreements has become a strategic priority.

Google has matched all its global electricity use with renewable energy every year since 2017–2018. It has also signed over 75 clean energy agreements worldwide. These support more than 10 GW of renewable capacity from wind, solar, and other sources.

The tech giant also aims to use 24/7 carbon-free energy by 2030. This plan goes beyond yearly matching. It needs to align electricity demand with clean energy in real time.

But Google has noted that the growing demand for AI is making it harder to reduce emissions in the short term. The company said that expanding data centers and increasing AI computing are raising electricity use. Still, efficiency gains and buying renewable energy are helping to lessen the effect.

A 2025 environmental update revealed that Google cut data center energy emissions by 12%. This happened even as electricity demand rose by 27%. The reduction came from new clean energy projects that were activated. The company also reported it has enabled 26 million tCO2e emissions reductions through five products.

Source: Google

Google Explores Orbital Data Centers With SpaceX

While Google expands renewable energy on Earth, it is also exploring a much more futuristic solution: moving part of AI computing into space.

Reports from The Wall Street Journal say that Google is talking to SpaceX. They are discussing possible launches for orbital data center infrastructure.

The talks involve Google’s internal research effort known as Project Suncatcher. The initiative centers on solar-powered satellites. These satellites have Google Tensor Processing Units (TPUs) and optical communication systems.

The idea is to put computing infrastructure in orbit. This way, satellites can gather constant solar energy above Earth’s atmosphere.

SpaceX plans to launch up to one million orbital data center satellites. These will orbit between 500 and 2,000 kilometers above Earth. Supporters say that orbital infrastructure might ease the load on land-based electricity grids. It could also provide a steady supply of solar power.

However, the technology remains highly experimental. Google’s research shows that launch costs must drop below about $200 per kilogram. Only then would orbital data centers be cheaper than Earth-based ones. Today, launch costs remain far higher.

Space-Based AI Infrastructure Faces Major Challenges

Despite growing interest, experts say orbital data centers still face huge technical and economic barriers. Most proposed systems rely on SpaceX’s Starship rocket. It needs to achieve fast, low-cost reusable launches. So far, this scale hasn’t been shown in commercial use.

Analysts at MoffettNathanson LLC estimate that thousands of Starship launches each year may be needed. This would support a large-scale orbital computing infrastructure.

Even SpaceX noted risks in its pre-IPO filings. It described orbital AI infrastructure as reliant on “unproven technologies.” Jensen Huang, CEO of NVIDIA, also called space-based AI infrastructure a “long-term engineering challenge.”

Still, interest across the technology sector is growing.

NVIDIA recently advertised positions focused on orbital computing systems. Startup Cowboy Space Corporation has also raised hundreds of millions to build rockets and infrastructure for space-based computing. These developments show how rapidly AI is pushing companies to rethink the future of digital infrastructure and energy supply.

Renewable Energy and AI Are Becoming Deeply Connected

The two Google stories, one focused on Texas solar power and the other on orbital data centers, reflect the same underlying issue.

AI growth is becoming closely tied to energy access. Technology companies now compete for more than just chips and software talent. They also seek electricity, grid access, renewable energy, and long-term power stability.

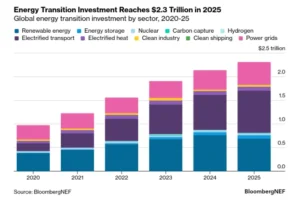

According to BloombergNEF, global investment in the energy transition reached $2.3 trillion in 2025. A large part of this growth came from electrification, AI infrastructure, battery storage, and renewable energy deployment.

At the same time, utilities and governments are increasingly concerned about whether power systems can keep up with AI demand growth. This is why companies are exploring multiple solutions simultaneously:

Google’s strategy reflects this broader shift. The 500 MW Texas solar agreement provides a near-term solution to rising electricity needs from AI data centers. Meanwhile, orbital computing research is a long-term effort. It aims to rethink where and how AI infrastructure works.

For now, Earth-based renewable energy remains the practical foundation of AI growth. But as power demand continues to rise, companies are increasingly exploring more unconventional solutions.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-05-15 09:15:122026-05-15 09:15:12Google’s Wild AI Strategy: 500 MW Solar Deal and Potential SpaceX Orbital Data Centers

Ford Motor Company ( has officially launched Ford Energy, a new business focused on manufacturing battery energy storage systems (BESS) for utilities, data centers, and industrial customers. The move is a big step for Ford. It goes beyond electric vehicles and puts the company in one of the fastest-growing energy markets in the world.

The company plans to produce 20 gigawatt-hours (GWh) of battery storage annually from its Kentucky battery facility by the end of 2027. That level of output would position Ford among the largest U.S.-based energy storage suppliers.

The launch also reflects a broader industry shift. Automakers are stepping into stationary energy storage. This shift comes as electricity demand grows due to AI, cloud computing, and renewable energy.

The U.S. government is also promoting domestic battery manufacturing. It offers clean energy tax credits and supply-chain incentives to encourage this effort.

Ford Energy stated:

“Utilities and developers need storage systems they can finance, insure and depend on for decades. They need suppliers who will be there in year 10 to honor a warranty claim. That is the gap Ford Energy is built to fill. Ford Motor Company has manufactured at industrial scale for more than a century, and we’re excited to bring this immense capability to energy storage.”

Ford’s Next Big Bet: Turning EV Batteries Into Grid Power

Ford’s new business will manufacture large lithium iron phosphate (LFP) battery systems designed for utilities and large commercial users. These storage systems stabilize electricity grids. They also store renewable energy from solar and wind farms.

The company expects to invest about $2 billion over the next two years to scale production.

Ford built much of its manufacturing setup with South Korean battery partner SK On for electric vehicles. However, slowing EV demand and extra battery capacity led the company to focus more on stationary energy storage.

Ford Energy’s flagship product is a 20-foot containerized battery unit similar to Tesla’s Megapack system. Each container stores about 5.45 megawatt-hours (MWh) of electricity using high-capacity LFP battery cells. The company plans to offer two versions:

First deliveries are expected in late 2027. Ford stock surged about 13% after investors responded positively to the company’s new energy storage business. This is its biggest one-day gain in nearly six years.

Analysts at Morgan Stanley said Ford’s partnership with Contemporary Amperex Technology Co. Limited gives the automaker a strong strategic advantage in the fast-growing battery storage market. Investors liked Ford’s plan to invest about $2 billion in U.S.-made battery storage systems.

Battery Energy Storage Demand Is Growing Rapidly Worldwide

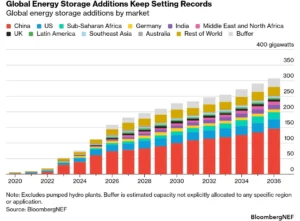

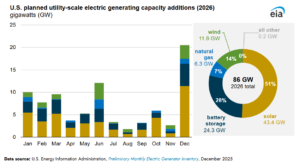

Ford is entering a market that is expanding at an extraordinary pace. According to BloombergNEF, global energy storage deployments reached about 307 GWh in 2025. The research firm forecasts worldwide deployments could rise to around 459 GWh in 2026 alone.

Meanwhile, the U.S. Energy Information Administration (EIA) expects the United States to add roughly 24 gigawatts (GW) of battery storage capacity in 2026. That would nearly double the record 15 GW added in 2025.

Industry forecasts also show total U.S. battery storage capacity could exceed 600 GWh by 2030. The growth is being driven by several major trends:

rising renewable energy installations,

surging electricity demand from AI,

grid modernization efforts, and

increasing electrification across industries.

Source: EIA

Battery storage is becoming essential because solar and wind power are intermittent. Electricity production changes depending on weather conditions and time of day.

Storage systems help solve this issue by saving electricity when supply is high and releasing it later during periods of peak demand. This flexibility is becoming increasingly valuable for utilities and large electricity users.

AI Data Centers Are Creating a Massive Storage Opportunity

One of the biggest growth drivers for battery storage is the rapid expansion of AI infrastructure. Large AI data centers consume enormous amounts of electricity and require an uninterrupted power supply. This is creating growing pressure on electricity grids globally.

According to the International Energy Agency, global data center electricity use could more than double, from 415 terawatt-hours (TWh) in 2024 to around 945 TWh by 2030.

AI workloads could become a major source of this growth. The IEA estimates electricity demand from AI-focused servers could rise by around 30% annually through the end of the decade.

Many data centers need faster power solutions and so, companies are now using battery storage systems. This helps them unlock power capacity without waiting years for new grid infrastructure. This trend is creating major opportunities for battery suppliers such as Ford Energy.

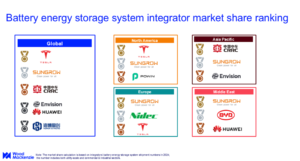

Tesla Still Leads the Market, But Rivals Are Closing In

Tesla currently dominates the global BESS market through its Megapack business. Research firm Wood Mackenzie estimates Tesla held about 15% of the global battery storage integrator market in 2024. In North America, Tesla controlled roughly 39% of the market.

Tesla’s energy business has also become increasingly important financially. The company reported energy generation and storage revenue of approximately $12.8 billion in 2025, up 27% year over year. Fourth-quarter storage deployments reached a record 14.2 GWh.

However, competition is increasing quickly.

Chinese energy storage supplier Sungrow Power Supply Co., Ltd. held roughly 14% of the global market in 2024, narrowing Tesla’s lead significantly. Other companies are also expanding aggressively into storage markets, including:

Several automakers are now exploring stationary battery systems using both new and repurposed EV batteries. This reflects growing recognition that energy storage could become a major long-term business opportunity beyond vehicle manufacturing.

U.S. Manufacturing Incentives Create New Opportunities

Ford may benefit from a growing policy push for domestic battery production. Recent U.S. clean energy policies push companies to get battery materials and make products at home. This shift reduces reliance on imports from countries seen as “foreign entities of concern.”

Ford’s battery plants in Kentucky and Michigan support this strategy while helping customers qualify for tax incentives. The company is also focusing on lithium iron phosphate batteries, which are cheaper, safer, and widely used in stationary storage systems.

Ford’s Energy Push Is Part of Its Climate Goals

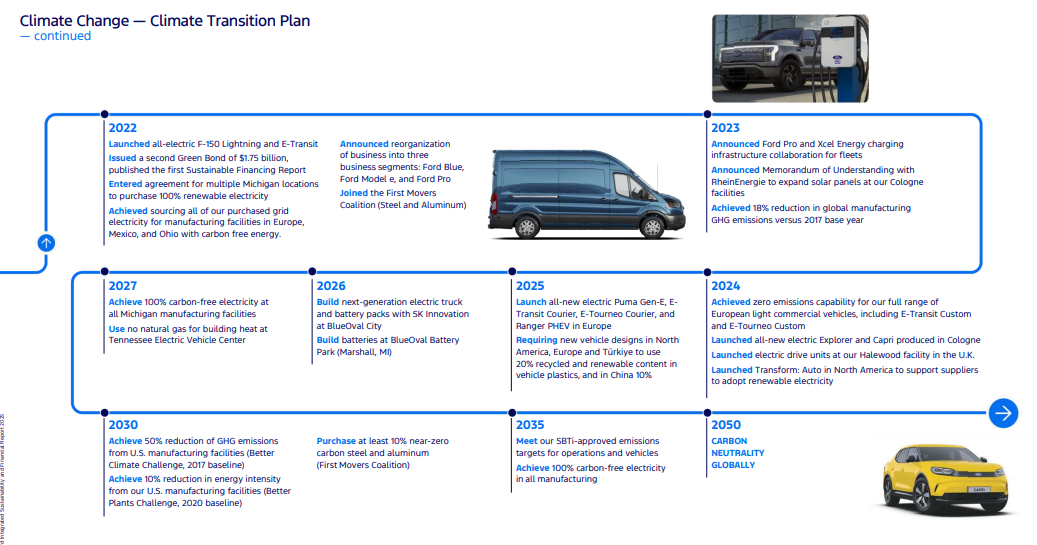

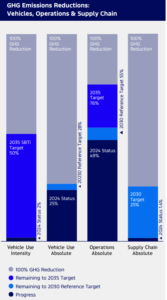

Ford says the expansion into energy storage supports its broader sustainability strategy. The company aims to achieve carbon neutrality across its global operations no later than 2050. The carmaker has also committed to using 100% carbon-free electricity for manufacturing globally by 2035.

Source: Ford; Road to Carbon Neutrality

Ford’s latest sustainability report shows it cut operational greenhouse gas emissions by about 40% from its 2017 baseline. The company is boosting its use of renewable electricity in manufacturing. It is also investing heavily in battery recycling and cleaner supply chains.

Source: Ford

Battery energy storage is becoming more important. It helps expand renewable energy use and keeps the grid stable. As renewable energy grows worldwide, big storage systems will be key. They help balance electricity supply and demand.

Entering a High-Stakes Battle for the Future of Energy Storage

Ford Energy represents one of the company’s biggest strategic expansions beyond traditional automotive manufacturing.

The energy storage market is expanding quickly. This growth comes from AI infrastructure, more investments in renewable energy, and increasing electricity demand.

As grids update and electricity needs grow, battery storage is key for the global energy shift. Ford’s entry into the sector shows how traditional carmakers are evolving into broader energy and technology companies.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-05-14 10:10:372026-05-14 10:10:37Ford’s New Energy Business Targets Tesla’s Storage Empire, Sending Stock (F) Upward

Oklo reported its first-quarter 2026 financial results along with several major business and regulatory updates. The company is still pre-revenue and posted wider losses during the quarter. However, investors focused more on Oklo’s growing reactor pipeline, faster regulatory progress, and new partnerships linked to artificial intelligence (AI) infrastructure.

Oklo is becoming part of two major global trends. One is the rapid growth of AI data centers. The other is the rising demand for reliable carbon-free electricity.

Oklo Strengthens Cash Position as AI-Nuclear Interest Grows

Oklo reported an adjusted earnings per share (EPS) loss of $0.18 for Q1 2026. This matched analyst expectations. The loss was bigger than last year during the same time. The company kept spending on reactor licensing, engineering, fuel research, and commercial projects.

Source: Oklo

Still, the company improved its financial position during the quarter. Total liquidity reached about $2.6 billion after Oklo completed a large at-the-market stock offering. The stronger balance sheet gives the company more flexibility to fund future reactor projects without immediate financing pressure.

Despite the quarterly loss, OKLO stock has gained momentum in recent months. Shares have climbed sharply in 2026 as investor interest grows around nuclear energy and AI infrastructure.

The rally also reflects stronger momentum across the advanced nuclear sector. Small modular reactor (SMR) and microreactor companies are attracting interest as governments and tech firms want stable, low-carbon power sources.

According to the International Energy Agency (IEA), electricity demand from global data centers could more than double by 2030, reaching nearly 945 terawatt-hours (TWh).

AI systems could become one of the biggest drivers of this increase. This trend is creating new interest in nuclear energy because reactors can provide constant electricity around the clock without direct carbon emissions.

Fast-Tracked NRC Approval Pushes Aurora Reactor Closer to Reality

One of the company’s biggest developments this quarter was a major regulatory milestone for its Aurora powerhouse project in Idaho. The U.S. Nuclear Regulatory Commission (NRC) approved Oklo’s Principal Design Criteria (PDC) topical report for the Aurora reactor. This document sets important safety and performance standards for future reactor licensing.

The approval process moved faster than normal NRC timelines. Oklo said the report was accepted within 15 days, compared with the usual 30- to 60-day period. The full review also finished in less than half the normal time. This is important because licensing delays remain one of the biggest challenges in the nuclear industry.

The Aurora reactor is a compact fast reactor. It provides clean electricity and industrial heat. This makes it suitable for data centers, military sites, industrial facilities, and remote locations.

Oklo’s design stands out from traditional nuclear plants. Its reactors are smaller and made for quicker deployment. The company already secured a site use permit with the U.S. Department of Energy (DOE) for its first commercial Aurora powerhouse at Idaho National Laboratory.

The advanced reactor market is expected to grow quickly over the next decade. The World Nuclear Association says more than 80 SMR designs are now being developed worldwide.

The DOE also believes advanced nuclear power could help the United States meet long-term net-zero emissions goals by 2050.

NVIDIA Partnership Ties AI Computing to Next-Generation Nuclear Power

Another major development this quarter was Oklo’s partnership with NVIDIA and Los Alamos National Laboratory. The partnership aims to enhance nuclear fuel research and reactor development. It uses AI modeling, digital twins, and advanced simulations.

Under the agreement, NVIDIA’s AI systems will help Oklo and Los Alamos researchers study and improve advanced nuclear fuels. The partnership reflects a larger shift happening across the energy and technology sectors.

Major AI companies like Microsoft, Amazon, Meta, and Google now need large amounts of reliable carbon-free electricity for data centers and AI computing systems.

Unlike solar and wind, nuclear reactors can provide steady electricity 24 hours a day, regardless of weather conditions. This makes advanced nuclear energy attractive for AI infrastructure. Oklo hopes its Aurora and future reactor designs can help supply power for these next-generation computing systems.

Customer Pipeline Expands as Tech Giants Hunt for Clean Power

Oklo’s commercial pipeline also grew during the quarter. The company said its customer pipeline now totals about 14 gigawatts (GW) of possible electricity demand.

Part of this pipeline includes an agreement involving Meta tied to as much as 1.2 GW of future power capacity in Ohio. This shows rising interest from tech companies seeking long-term clean electricity contracts.

Power access is becoming one of the biggest challenges for AI expansion. Industry analysts now see electricity supply, transmission systems, cooling infrastructure, and grid access as key limits for future data center growth.

Advanced nuclear companies are seizing this trend. They provide stable, low-carbon electricity. Their emissions are lower than those from fossil fuels.

Oklo’s business model also focuses on long-term electricity sales instead of only building reactors. The company plans to own and operate many of its future power plants directly. If deployment succeeds, this could provide recurring long-term revenue.

Nuclear Energy Gains Momentum in Climate Plans

The broader nuclear industry has gained momentum as countries search for ways to reduce emissions while keeping power grids stable. The IEA reports that nuclear energy generates around 9% of global electricity. It is still one of the biggest sources of low-carbon power in the world.

The agency further states that nuclear power meets about 15% of global data center electricity needs. Also, tech companies have announced over 20 gigawatts (GW) of planned small modular reactor agreements linked to upcoming AI and data center projects.

Source: IEA

The IEA predicts that nuclear generation will hit record levels soon and continue to grow in importance after 2030. This growth will happen as new reactors are built in the United States, China, India, and Europe.

Moreover, hyperscalers will need reliable, low-emission baseload energy to meet AI-related electricity demand. These tech companies are increasing investments in clean energy.

They aim for net-zero goals and need reliable electricity for their AI operations. This growing need for clean baseload power may boost long-term growth for advanced nuclear developers such as Oklo.

At the COP28 climate summit, more than 20 countries agreed to support efforts to triple global nuclear capacity by 2050.

OKLO Stock Reflects Rising Interest in AI and Nuclear Power

Oklo’s latest quarterly update shows how advanced nuclear companies are benefiting from the rapid growth of AI infrastructure and demand for carbon-free electricity. The company still faces major challenges. It remains pre-revenue, reactor deployment timelines are uncertain, and nuclear licensing remains difficult.

However, the quarter showed strong progress in several areas:

Faster NRC regulatory approvals,

New AI-focused partnerships,

Stronger liquidity and financing,

Growing commercial power demand, and

Rising interest from technology companies.

For investors watching OKLO stock, the company remains a high-risk but potentially high-growth play tied to AI infrastructure, advanced nuclear energy, and carbon-free electricity. As AI electricity demand continues rising, companies that can provide stable and scalable low-carbon power may become more important in the global energy transition.

TeraWulf Inc. (NASDAQ: WULF) has received a new $31 price target from Cantor Fitzgerald, reflecting rising investor interest in its low-carbon bitcoin mining strategy. The analyst note points out that TeraWulf uses low-emission energy, which includes nuclear and hydro power at its main facilities in the United States. These include the Lake Mariner site in New York and the Nautilus Cryptomine facility in Pennsylvania.

The update comes as investors pay closer attention to the environmental footprint of bitcoin mining. The sector remains highly energy-intensive.

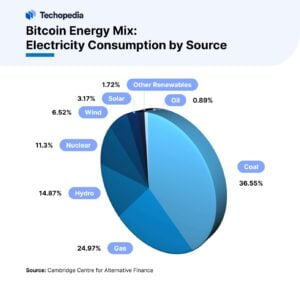

The Cambridge Centre for Alternative Finance reports that global bitcoin mining uses over 100–150 terawatt-hours (TWh) of electricity each year. This is comparable to the energy consumption of medium-sized countries.

TeraWulf stands out as one of the few public miners using low-carbon or carbon-free energy on a large scale. Cantor Fitzgerald said the company’s energy strategy and infrastructure model help it grow long-term. This is important in a sector under more ESG scrutiny.

WULF stock has gained momentum after the raise in price target to $31. Investor interest has also been supported by rising demand for nuclear-powered and energy-efficient digital infrastructure tied to AI and crypto growth.

The recent bitcoin price rally has also improved sentiment across the mining sector. Bitcoin has continued trading around $80,000 level after reaching an all-time high above $126,000 in late 2025.

Higher BTC prices generally improve mining profitability. This is because miners earn more value from each bitcoin produced while operating costs remain relatively stable.

This stronger market environment has supported renewed interest in crypto infrastructure stocks such as WULF stock. Investors are increasingly focusing on miners with lower energy costs and more stable power access.

A Low-Carbon Mining Model Built on Nuclear and Hydro Power

TeraWulf operates two main facilities that anchor its mining strategy. The first is Lake Mariner in New York, which draws power from a grid that is largely supported by nuclear and hydroelectric generation. The second is Nautilus Cryptomine in Pennsylvania. It gets its power directly from the Susquehanna nuclear plant through a behind-the-meter agreement.

Nautilus is the company’s most significant ESG asset. It runs entirely on nuclear power. This makes it one of the first large-scale bitcoin mining sites in the world to use nuclear energy directly.

However, the company’s portfolio isn’t always 100% carbon-free. Lake Mariner still uses a mix of grid electricity. TeraWulf says that a big part of its energy comes from carbon-free sources. This includes nuclear, hydro, and other low-emission options.

Source: TeraWulf

This distinction matters in ESG reporting. Many bitcoin mining firms still rely heavily on fossil fuels such as coal and natural gas. The International Energy Agency (IEA) says coal provides about one-third of global electricity. This still contributes significantly to emissions.

TeraWulf’s strategy, therefore, focuses on reducing exposure to fossil-heavy grids by anchoring operations in cleaner energy regions.

Bitcoin Mining Faces Rising Pressure Over Energy Use and Emissions

Bitcoin mining continues to face strong debate over its environmental impact. Mining requires large amounts of electricity to run high-performance computing systems. These systems validate transactions and secure the blockchain network. The result is a high and continuous energy demand.

Studies from Cambridge and other research groups say Bitcoin’s energy use can sometimes surpass that of entire countries, like Argentina or the Netherlands.

This has placed increasing pressure on miners to adopt cleaner energy sources. Institutional investors are also beginning to factor emissions intensity into their investment decisions.

At the same time, global electricity systems are gradually becoming cleaner. The International Renewable Energy Agency (IRENA) says that renewables made up about 30% of global electricity generation recently. They expect this to keep growing until 2030.

This shift is important for crypto mining. It creates a pathway for lower-carbon operations, especially for companies that can secure long-term access to nuclear, hydro, or renewable power. TeraWulf’s model fits into this transition by prioritizing energy contracts tied to low-emission generation.

AI and Data Center Boom Push Electricity Demand Into Overdrive

The demand for digital infrastructure is growing quickly. This includes AI computing, cloud services, and blockchain systems.

The International Energy Agency estimates that global data centers consumed about 415 TWh of electricity in 2024. Under high-growth scenarios, this could rise to nearly 950 TWh by 2030.

This growth is driven by AI workloads and large-scale computing systems. These systems require constant power and high-density computing environments. As demand rises, electricity access is becoming a key constraint. Companies are no longer competing only on hardware or software. They are also competing for energy availability.

TeraWulf benefits from this shift. Its facilities are in areas with stable grid access and large baseload energy sources like nuclear and hydro. Industry reports show the following energy mix used by bitcoin miners, with hydro and nuclear being the top two renewable sources.

This provides a competitive advantage. Unlike fossil fuel-heavy regions, nuclear and hydro systems offer more stable long-term pricing and lower carbon intensity. As a result, low-carbon mining infrastructure is increasingly seen as part of the broader “clean compute” economy.

Wall Street Turns to ESG-Backed Crypto Infrastructure Plays

The Cantor Fitzgerald price target reflects a broader trend in financial markets. Institutional investors are paying closer attention to ESG-linked digital infrastructure.

Bitcoin mining companies are now judged on more than just profits. They are also assessed based on their energy sources and emissions.

TeraWulf has an advantage on this shift because it can demonstrate measurable access to low-carbon energy. Its nuclear-powered Nautilus facility is especially important in this regard.

The company set up long-term agreements. These help ensure stable energy access and keep operating costs predictable. This is a key factor for institutional investors who prefer lower volatility infrastructure plays.

Other mining companies are also shifting toward cleaner energy strategies. CleanSpark says a large portion of its bitcoin mining operations uses low-carbon and renewable-heavy energy sources across the United States.

IREN Limited (formerly Iris Energy) operates data centers powered mainly by renewable electricity, particularly hydro energy in Canada. Meanwhile, MARA Holdings (formerly Marathon Digital Holdings) has expanded partnerships tied to renewable and flare-gas energy projects to reduce emissions intensity.

Clean Energy Mining as a Competitive Advantage

Energy sourcing is becoming one of the most important competitive factors in bitcoin mining. Companies that secure access to nuclear, hydro, or renewable power can operate with lower emissions and more stable energy pricing.

TeraWulf’s strategy focuses on this advantage. Its nuclear-backed Nautilus facility provides consistent baseload power. Its Lake Mariner site benefits from a relatively clean regional grid mix.

This structure helps the company reduce exposure to fossil fuel volatility. It also improves long-term operational predictability.

The International Energy Agency expects electricity demand from data centers, AI, and digital infrastructure to grow significantly through 2030. This will increase competition for clean power sources. In this setting, companies with low-carbon energy contracts might have a key advantage.

Source: IEA

Analysts also note that institutional demand for Bitcoin continues to rise through spot Bitcoin ETFs, corporate treasury adoption, and growing digital asset investment flows. This broader market momentum is helping support long-term demand for scalable and energy-efficient mining infrastructure.

WULF Stock and the Shift Toward Low-Carbon Mining

TeraWulf’s $31 price target highlights growing investor interest in low-carbon bitcoin mining infrastructure. The company has built a model based on nuclear and hydro energy access, with one of its key facilities operating on direct nuclear power. Its overall portfolio isn’t completely carbon-free, but it has much lower emissions than many industry peers.

Bitcoin mining remains one of the most energy-intensive computing industries in the world. Companies that secure clean, stable electricity can better adapt to market and regulatory changes.

For investors watching WULF stock, TeraWulf shows a shift. It blends digital computing with lower-carbon energy systems. This positioning places the company at the intersection of three major trends:

rising demand for digital infrastructure,

increasing pressure to reduce emissions, and

growing importance of clean baseload energy.

As these trends converge, low-carbon mining may become a standard rather than an exception in the global bitcoin industry.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-05-13 10:25:262026-05-13 10:25:26WULF Stock Climbs on $31 Target as TeraWulf Bets Big on Low-Carbon, Nuclear-Powered Bitcoin Mining

Disseminated on behalf of Alaska Energy Metals Corporation

The global race for critical minerals is entering a decisive phase. As countries accelerate clean energy adoption and strengthen defense readiness, the need for secure and domestic supply chains has become urgent. The United States, in particular, is working to reduce its dependence on foreign sources for essential materials. Against this backdrop, AEMC’s Nikolai project is emerging as a high-impact asset with the potential to transform the country’s critical minerals landscape.

With its updated 2025 Mineral Resource Estimate (MRE), Nikolai demonstrates not only exceptional scale but also a diverse metals portfolio. This combination positions it as a strategic solution to growing supply challenges across energy, industrial, and national security sectors.

Massive Scale Sets Nikolai Apart

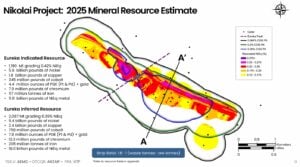

Scale is the defining feature of the Nikolai project. The latest resource estimate confirms:

5.6 billion pounds of nickel (Indicated)

9.4 billion pounds of nickel (Inferred)

With further drilling, a portion of the current Inferred resource may be upgraded to the higher-confidence Indicated category. If the full Inferred resource were successfully converted, Nikolai’s Indicated nickel resource could increase from 5.6 billion pounds to more than 15 billion pounds. This potential upgrade is not guaranteed, but it highlights the scale of the deposit and the opportunity for additional drilling to strengthen the project’s resource confidence.

Here’s a detailed, updated resource estimate from the company.

Source: Alaska Energy Metals

This scale gives Nikolai a clear advantage over many domestic peers. Several U.S. nickel projects remain smaller in scope or are still in early exploration phases. In contrast, Nikolai already shows a well-defined and expansive mineral system, with strong potential for further growth through additional drilling and exploration.

Another critical strength lies in its oxide and sulphide composition. This dual mineralization could provide flexibility in how the resource is developed and processed over time. Such adaptability is especially valuable for large-scale projects, where long-term operational efficiency and cost management are key factors.

Ultimately, Nikolai’s size is not just a headline number. It represents long-term supply potential, making it capable of supporting sustained production over decades rather than short-term output cycles.

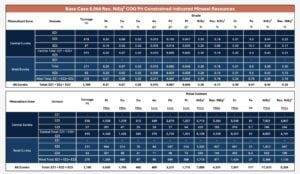

A Multi-Metal Resource with Strong Market Alignment

Beyond its nickel resources, Nikolai stands out for its diversified metal content. The project hosts a broad mix of critical materials that enhance both its economic value and strategic importance.

The resource model includes:

1.7–2.4 billion pounds of copper

0.4–0.76 billion pounds of cobalt

Several million ounces of platinum group metals (platinum, palladium, and gold)

Additionally, the presence of chromium and iron further strengthens its industrial relevance.

Here’s a detailed breakdown of the Nikolai Eureka Project: 2025 Indicated Mineral Resource Estimate:

Source: AEMC

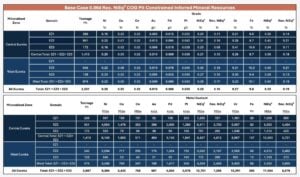

For more details of the 2025 Inferred Category Resource Estimate of the Nikolai Eureka Project, check the table below:

Source: AEMC

This multi-metal profile is a major advantage. It reduces dependence on a single commodity and allows the project to benefit from multiple demand drivers. As global markets evolve, such diversification helps balance price volatility and ensures more stable long-term returns.

More importantly, the combination of metals aligns closely with future demand trends. Instead of serving a niche market, Nikolai supports a wide range of high-growth sectors tied to electrification, advanced manufacturing, and infrastructure development.

This alignment increases the project’s resilience and enhances its appeal to investors and policymakers alike.

Nikolai’s value extends well beyond its resource size. It directly addresses one of the biggest challenges facing the United States: supply chain vulnerability.

A significant portion of the metals found at Nikolai is currently sourced from overseas. This reliance exposes the U.S. to risks such as trade restrictions, geopolitical tensions, and supply disruptions.

Importantly, seven metals hosted at the project are included in the U.S. Department of Defense’s Critical and Strategic Materials list. This underscores their importance for national security and long-term strategic planning.

Projects like Nikolai offer a path toward greater independence. By developing domestic resources, the U.S. can reduce exposure to external shocks and build a more stable supply base.

The scale of Nikolai further strengthens its strategic value. Large, long-life assets are essential for ensuring a consistent supply, particularly for industries that require steady and predictable material flows. Smaller or fragmented projects often cannot meet this need.

In this context, Nikolai is not just a mining project. It is a potential cornerstone for strengthening U.S. resilience across multiple sectors.

Strengthening North American Industrial Ecosystems

The shift toward localized supply chains is gaining momentum across North America. Companies are increasingly prioritizing regional sourcing to improve reliability, reduce risk, and meet evolving regulatory requirements.

Nikolai fits seamlessly into this transition. Its resource base supports both emerging industries and established sectors, creating a bridge between new energy systems and traditional manufacturing.

Reinforcing supply chains for heavy industry and infrastructure

This cross-sector relevance makes Nikolai particularly valuable. Instead of depending on a single market, it integrates into a broader industrial framework.

Additionally, localized sourcing is becoming a key requirement for companies aiming to qualify for government incentives and sustainability targets. Projects like Nikolai can help meet these criteria while also improving transparency and traceability within supply chains.

As North America continues to build its industrial base, assets like Nikolai will play a crucial role in supporting long-term growth.

Policy Tailwinds Accelerate Momentum

Government support is becoming a major driver of critical minerals development in the United States. Policymakers are increasingly focused on strengthening domestic capabilities and reducing reliance on imports.

Under the Trump administration, the U.S. critical minerals strategies are promoting:

Increased funding for exploration and development

Stronger coordination between the public and private sectors

Expansion of domestic processing and refining capacity

These policy tailwinds create a supportive environment for large-scale projects like Nikolai. They not only improve the economic outlook but also reduce regulatory uncertainty, which is often a key barrier in mining development.

Most significantly, the Nikolai Nickel Project in Alaska received FAST-41 permitting transparency status in November 2025 under EO 14241, reducing uncertainty for such strategically aligned projects.

As a result, projects with strong fundamentals and strategic alignment are likely to gain momentum in the coming years.

Analysis: A High-Impact Asset in a Tightening Market

The global nickel and critical minerals market is entering a complex phase. While short-term price movements remain volatile, long-term demand continues to strengthen due to electrification and industrial growth.

At the same time, supply growth faces challenges, including permitting delays and geopolitical constraints. This creates a gap between future demand and reliable supply sources.

Nikolai stands out as a project capable of addressing this gap. Its scale, diversified resource base, and U.S. location give it a strong competitive edge.

Importantly, its value lies not just in the volume of resources but in its ability to support multiple sectors simultaneously. This makes it more resilient and strategically important compared to single-commodity projects.

In the broader context, Nikolai represents more than a mining opportunity. It reflects a shift toward resource security, domestic capability, and long-term planning.

As global competition for critical minerals intensifies, assets like Nikolai are becoming essential. If developed successfully, it could play a defining role in shaping the future of U.S. energy, industry, and supply chain resilience.

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Alaska Energy Metals. (“Company”) made a one-time payment of $75,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-05-13 10:25:262026-05-13 10:25:2615 Billion Pounds of Nickel: Nikolai Emerges as a Strategic U.S. Critical Minerals Giant

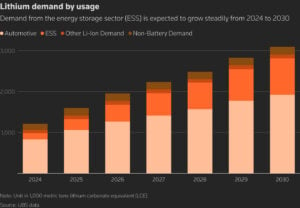

The story of lithium demand is changing. For many years, electric vehicles (EVs) were the main driver of demand for lithium. Today, that is no longer the full picture.

Battery storage is growing quickly. In 2025, global battery energy storage system (BESS) installations exceeded about 315 gigawatt‑hours (GWh), nearly 50% more than in 2024, according to Benchmark Mineral Intelligence. Grid‑scale storage and behind‑the‑meter projects for industry and data centers are major contributors to that growth.

This shift matters. According to industry analysis cited by Lithium Americas CEO John Evans, every one GWh of grid storage capacity requires about 900 tonnes of lithium. That is a large amount of material, and it adds a new layer to how lithium demand is understood.

As a result, lithium demand is now coming from three main forces in parallel: EVs, grid storage, and data center power resilience. This expanded demand picture is changing market forecasts and investment strategies.

EVs, Grid Storage, and Data Centers: The Three Forces Driving Demand

Electric vehicles are still an important part of lithium demand. EV sales and battery build‑outs continue to grow worldwide. However, they are not the only force driving lithium consumption.

Battery storage for the grid and for industrial power systems is becoming a major demand driver. Utilities around the world are installing lithium‑ion batteries to balance renewable energy, improve reliability, and cut peak power costs.

Source: Benchmark Mineral Intelligence/SEIA

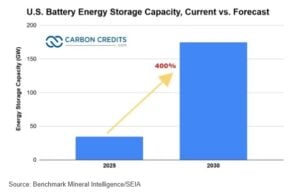

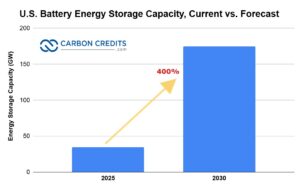

In the United States, the battery energy storage capacity is projected to grow 400% from 2025 to 2030. Data from Benchmark Mineral Intelligence and the SEIA project this rapid growth in five years.

At the same time, technology companies are deploying large lithium battery systems behind the meter to support reliable power for AI and cloud computing.

This broadening of lithium demand reflects developments in energy and technology infrastructure planning. For many regions, battery storage is no longer a side project; it is part of the core energy strategy.

Lithium-Ion Batteries Powering the Grid and Industry

Lithium‑ion technology is now the dominant choice for BESS. It accounted for a large majority of storage systems installed in 2024, and that share remained high into 2025.

Industry reports project that the global BESS market could be worth tens of billions of U.S. dollars by 2030, with steady growth as storage systems scale up to support renewables and grid flexibility.

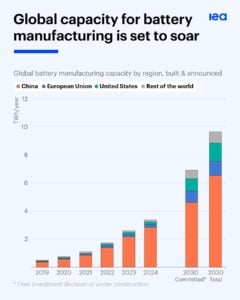

Meanwhile, battery manufacturing capacity is expanding rapidly. The International Energy Agency reported that global battery production exceeded 3 terawatt‑hours (TWh) per year in 2024, nearly three times what was needed for EV and storage demand that year. And it could soar to almost 10 TWh a year.

Source: IEA

These developments show that demand for lithium in storage applications is becoming structural, not temporary.

From Transport to Infrastructure: Lithium’s Expanding Role

The rapid growth of grid storage affects how lithium demand is forecasted. In the past, most forecasts focused on EV batteries. Today, models are being adjusted to include storage applications that are tied to national energy planning and corporate resilience strategies.

As BESS installations grow, demand becomes more predictable and less tied to consumer EV purchase cycles. This stability matters for investors, suppliers, and policymakers alike. It means that supply projects need to plan for longer-term demand horizons, with stable output for multiple industry uses.

Nevada North Lithium Project: Built for the Multi-Driver Lithium Market

This expanded demand picture highlights the importance of long‑lived lithium resources. Projects that can supply lithium steadily, for many years, are becoming more important as demand widens beyond EVs.

One example that aligns with this shift is the Nevada North Lithium Project (NNLP) by Surge Battery Metals (TSX-V: NILI | OTCQX: NILIF), a high‑grade, domestic resource with characteristics that match the evolving market needs.

Here are key attributes of NNLP that align with expanding lithium demand:

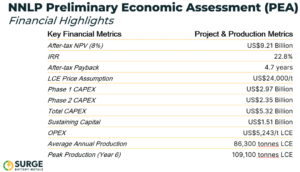

Long Duration Supply: NNLP has a projected 42‑year mine life, according to the 2025 Preliminary Economic Assessment (PEA). This long horizon supports the extended demand profiles needed for grid storage build‑outs and infrastructure projects, not just EV batteries.

High Annual Output: The project’s average production of approximately 86,300 tonnes per year of lithium carbonate equivalent (LCE) places it in the range needed for large‑scale storage supply frameworks.

Domestic Resource Position: Located in Nevada, NNLP contributes to U.S. goals for domestic critical mineral supply. This is increasingly important for utilities, policy makers, and corporate partners who want secure, high‑quality sources closer to end markets.

Development Framework: NNLP’s planning and partnerships position it to meet commercial expectations tied to long‑term supply, offtake, and investment strategies.

These features are meaningful as the market looks for lithium that can serve EVs, grid‑scale storage, and data center power resilience together, not in isolation.

Battery storage is becoming a focus of public policy and business planning. In regions where grid reliability is a concern, storage systems help prevent blackouts and manage peak demand. For utilities, storage offers a way to integrate more renewable energy without compromising stability.

At the same time, commercial and industrial users, especially data centers supporting AI workloads, are investing in battery systems that protect operations from interruptions. This is especially true for data centers that support AI workloads.

Companies like Amazon Web Services, Microsoft, and Google are deploying large-scale battery storage at their data centers to prevent outages. These systems provide instant backup power, helping avoid costly downtime. They also reduce the need for diesel generators, which are expensive and produce emissions. As AI demand grows, more companies are expected to follow this approach.

As a result, storage applications are increasingly planned alongside utility infrastructure and technology investments. This trend has elevated battery storage from a supporting data point to a lead story in lithium demand.

Numbers Speak: BESS Installations and Market Growth

To put the storage boom in perspective:

Global BESS installations exceeded 315 GWh in 2025, up about 50 percent from 2024.

Lithium‑ion batteries remain the dominant technology in utility and industrial storage systems.

Global battery manufacturing capacity surpassed 3 TWh per year in 2024, expanding supply frameworks for EVs and storage alike.

The global BESS market is projected to grow strongly through 2030, supported by energy policy and grid modernization plans.

These figures show that lithium demand is no longer defined by a single industry application, but by multiple, overlapping infrastructure and technology drivers.

As battery storage continues to grow alongside EV adoption, the narrative around lithium demand will continue to evolve. Lithium’s role is expanding from a material tied mainly to transportation to a foundational input in energy systems and technology infrastructure.

In this new landscape, projects with deep resources, stable mine lives, and strong production profiles like NNLP are positioned to meet diversified demand over decades. Their potential to supply lithium for multiple demand drivers reflects how the market is reshaping itself.

The battery storage boom is more than a trend; it is redefining how lithium is used and valued in the global economy.

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Surge Battery Metals Inc. (“Company”) made a one-time payment of $75,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

Disclosure: Owners, members, directors, and employees of carboncredits.com have/may have stock or option positions in any of the companies mentioned: None.

Carboncredits.com receives compensation for this publication and has a business relationship with any company whose stock(s) is/are mentioned in this article.

Additional disclosure: This communication serves the sole purpose of adding value to the research process and is for information only. Please do your own due diligence. Every investment in securities mentioned in publications of carboncredits.com involves risks that could lead to a total loss of the invested capital.

China and the European Union have formed a new alliance aimed at strengthening cooperation on carbon pricing systems, according to Bloomberg reporting. The move shows a widening gap in global climate policy. China and Europe are aligning their carbon markets, while the United States continues to back fossil fuel expansion.

The coalition was announced in Florence. It aims to improve coordination between major emissions trading systems. It aims to strengthen carbon pricing rules, emissions reporting, and market transparency across regions.

Kurt Vandenberghe, director general for climate at the European Commission, stated during the announcement:

“[There is a need] to make sure that these emissions trading systems talk to each other so that it becomes much easier for trading these carbon credits, and that also companies are facilitated in working in different jurisdictions.”

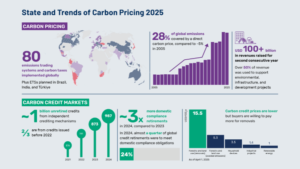

Carbon pricing is already widely used globally. Over 40 countries and more than 35 regional or local systems now have carbon taxes or emissions trading schemes, based on global climate policy data.

This growing network remains fragmented. Prices, rules, and market coverage vary widely between regions. The new China–EU partnership aims to reduce some of this fragmentation and improve compatibility between systems.

Carbon Pricing Becomes a Central Climate Policy Tool

Carbon pricing has become one of the most widely used tools for reducing greenhouse gas emissions. The system places a cost on every ton of CO₂ emitted, pushing companies to lower emissions or invest in cleaner technologies.

There are two main approaches:

Carbon taxes

Emissions trading systems (ETS), where companies buy and sell emission allowances

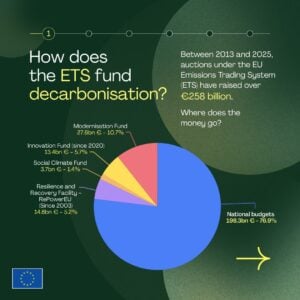

The European Union operates the world’s most advanced carbon market through its EU Emissions Trading System (EU ETS). The program covers power generation, heavy industry, and aviation within Europe.

Source: EC

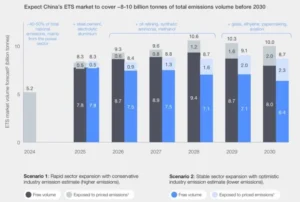

China launched its national ETS in 2021. It is now the largest carbon market in the world based on emissions covered. It primarily targets the power sector, which accounts for about 40% of China’s CO₂ emissions.

The system covers over 5 billion tonnes of CO₂ each year from the power industry alone. Analysts estimate that once the additional sectors are fully included, China’s ETS could cover between 8.7 and 10.6 billion tonnes of CO₂ by the late 2020s, representing a substantial share of the country’s total emissions.

Source: WEF Asia’s Carbon Markets Strategic Imperatives for Corporations, 2025.

Carbon prices between the two systems remain far apart. In China, prices started at around 48 yuan per ton of CO₂, equal to roughly $7 per ton at launch. European carbon prices have ranged from €70 to €90 per ton in recent years. This makes the EU system one of the priciest carbon markets in the world.

This large pricing gap is one of the main reasons China and Europe are now seeking closer coordination.

Inside the New China–EU Carbon Alliance

The new carbon alliance between China and the European Union is not designed to merge the two carbon markets. Instead, the partnership focuses on improving compatibility and cooperation between systems.

The initiative centers on:

Aligning emissions measurement standards,

Improving monitoring, reporting, and verification (MRV) systems,

The partnership builds on climate cooperation from the COP30 summit. The countries agreed to better coordinate their carbon pricing systems.

Today, more than 110 carbon pricing instruments operate globally at national and regional levels. However, many of these systems still use different accounting methods, reporting standards, and pricing mechanisms.

Source: World Bank Group

The China–EU partnership seeks to close these gaps. It aims to improve how emissions data and carbon credits are recognized across borders. This could eventually influence international carbon credit trading and future climate-linked trade rules.

US Climate Policy Direction Moves on a Different Path

While China and Europe deepen carbon pricing cooperation, the United States is moving in another direction. Recent policy trends show stronger support for fossil fuel production and slower progress toward a nationwide carbon pricing system. Many US states have regional carbon markets, but there is no national carbon pricing framework.

This has created three broad climate policy approaches globally. Europe and China are growing their carbon pricing systems. They are also linking these systems more closely to industrial policy.

The United States remains focused on energy production growth with limited carbon pricing adoption. Many emerging economies are building mixed systems. They combine carbon markets with traditional energy policies.

The divide is becoming increasingly important for global trade. The European Union has launched its Carbon Border Adjustment Mechanism (CBAM). This mechanism adds carbon costs to imported goods, depending on their emissions intensity.

This policy pushes exporting countries to adopt clear emissions reporting and better carbon accounting. They need to do this to stay competitive in global markets.

Carbon Markets Expand, But Global Rules Remain Fragmented

Despite political and regional differences, global carbon markets continue to grow. More than 55 countries now operate some form of carbon pricing system, covering over 28% of global greenhouse gas emissions.

The EU ETS covers about 40% of emissions in the European Union. In contrast, China’s ETS is the largest in terms of total emissions volume.

However, carbon pricing remains highly uneven across regions. Prices range from less than $10 per ton in some systems to more than $80 per ton in others. This creates uncertainty for multinational companies operating across different markets.

China’s ETS provides broad emissions coverage but still operates at relatively low prices compared with Europe. The EU ETS, by contrast, has become a high-price system that sends stronger decarbonization signals to industry.

These differences affect investment decisions, carbon credit trading, and long-term corporate decarbonization planning. Companies with global supply chains now face various carbon pricing systems. Each one has its own rules and compliance needs.

Impact on Carbon Credits and Global Trade Systems

The China–EU carbon alliance could significantly reshape global carbon credit markets over time.

If carbon pricing systems align better, the market may gain stronger trust in international carbon credits. This could lead to better liquidity in compliance markets and lower risks of double-counting emissions reductions.

Improved coordination may also strengthen demand for high-integrity carbon credits that meet stricter reporting standards. At the same time, the expansion of carbon pricing could increase trade complexity if systems are not fully recognized across borders.

Carbon pricing is becoming more closely tied to international trade policy. The EU CBAM adds carbon costs to imported goods. This change reshapes global supply chains and affects production choices.

Will Global Carbon Markets Eventually Align?

The formation of a China–Europe carbon pricing coalition highlights both progress and fragmentation in global climate policy.

Carbon markets are expanding rapidly and becoming a central climate policy tool in many economies. However, major differences remain in pricing levels, enforcement rules, and market structures.

The global carbon economy is changing due to three main trends:

More carbon pricing systems in China and Europe.

Ongoing fossil fuel policies in the United States.

Mixed or developing carbon frameworks in emerging markets.