Copper prices hit new multi-year highs in 2026. This rise is due to supply disruptions, increased industrial demand, and structural shortages in global mining markets.

On the London Metal Exchange (LME), copper rose to $14,153 per metric ton on May 13, 2026. This marks its first time over $14,000 since January. It’s now approaching its all-time high, which is above $14,500 per ton.

In the United States, COMEX copper futures also hit a record near $6.64 per pound on May 13, 2026, marking one of the strongest rallies in recent years.

Copper futures declined 1.19% today, trading at $6.25/lb globally and ¥93,730/Ton in China. The pullback is primarily driven by a hawkish shift in US Federal Reserve monetary policy, with rising rate hike expectations heavily weighing on industrial metals. Simultaneously, weak downstream demand in China and the accumulation of finished product inventories have prompted local processors to schedule furnace maintenance. This suppressed buying overshadowed lingering supply-side concerns regarding Chile’s reduced output forecasts.

Copper Price

Unit: USD/lb

—

—

Loading Chart…

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-05-20 12:15:102026-05-20 12:15:10Copper Prices Rise Past $14,000 as AI Demand, Peru Supply Shock, and Global Deficit Concerns Tighten Market

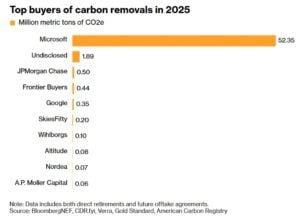

BioCirc has signed a major agreement with Microsoft (MSFT stock) to deliver 650,000 high-durability carbon removal units (CRUs) over seven years. The deal will support Microsoft’s goal of becoming carbon negative by 2030 while helping expand the market for durable carbon removal solutions in Europe.

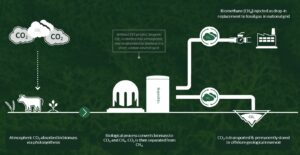

The agreement focuses on BioCirc’s bioenergy with carbon capture and storage (BECCS) platform in Denmark. Under the deal, BioCirc will supply around 100,000 CRUs every year between 2026 and 2032. Deliveries will begin in the second half of 2026 as the project gradually ramps up.

Each CRU represents one metric ton of carbon dioxide permanently removed from the atmosphere and stored underground. The captured carbon will come from biogenic CO2 generated at BioCirc’s biogas plants and then stored deep beneath the Danish North Sea.

Deal Comes After Questions Around Microsoft’s Carbon Removal Strategy

The agreement is important because it comes shortly after reports suggested Microsoft had slowed some carbon removal purchases. Earlier reports claimed the company had informed some suppliers that it was pausing parts of its procurement activity.

However, as per reports, Microsoft later clarified that its carbon removal program remains active. The company’s Chief Sustainability Officer, Melanie Nakagawa, explained that carbon removal still plays a key role in Microsoft’s climate strategy. She also noted that the company may adjust the pace and scale of future purchases depending on market conditions and project readiness.

This new agreement with BioCirc shows that Microsoft continues to invest in large-scale, durable carbon removal projects despite recent concerns. It has significantly emerged as one of the world’s largest buyers of high-quality carbon removal credits. Instead of depending on one technology, the company spreads its investments across several approaches.

Source: Microsoft

BioCirc Expands Its Circular Energy Vision

BioCirc operates in the circular bioeconomy sector and focuses on reducing emissions through biogas and renewable energy systems. The company develops energy solutions that use every part of the biogas value chain while lowering carbon emissions and supporting energy security.

The CCS project has become one of the company’s most important climate initiatives. BioCirc plans to connect biogas production with carbon capture and permanent underground storage. This approach allows the company to remove carbon dioxide from the atmosphere while continuing to generate renewable energy.

The project will capture biogenic CO2 from five Danish biogas plants. These facilities include Favrskov Biogas, Vesthimmerland Biogas, Haderslev Biogas, Grønhøj Biogas, and Vinkel Biogas.

Operations are expected to expand gradually between 2026 and 2032. During this period, BioCirc aims to capture and permanently store up to 1 million tonnes of CO2. According to the company, that amount equals the annual direct emissions of more than 130,000 people in Denmark.

The captured carbon dioxide will be transported to the Greensand Future storage site in the Danish North Sea.

There, the CO2 will be injected around 1,500 to 1,800 meters beneath the seabed into the Nini West reservoir.

This process creates a complete carbon capture and storage value chain. It starts from decentralized capture at biogas facilities and ends with permanent offshore geological storage.

Source: BioCirc

The project also receives support from the Danish Energy Agency through the NECCS fund. According to BioCirc, both the government subsidy and Microsoft’s carbon removal purchase agreement are necessary to make the project financially viable.

The company also emphasized that all lifecycle emissions linked to the process will be measured carefully. This includes emissions from biomass sourcing, plant operations, and transportation. BioCirc said the accounting process will ensure that the project delivers genuine net carbon removal.

In addition, the biomass used in the system must meet strict Danish sustainability standards. The company added that its facilities already meet or exceed Denmark’s methane detection and leak prevention requirements.

Microsoft Makes Carbon Removal the Key to Managing AI-Driven Emissions

Despite its ambitious climate commitments, Microsoft continues to face growing emissions challenges. The rapid expansion of artificial intelligence, cloud computing, and data center infrastructure has increased the company’s carbon footprint in recent years.

Its total emissions have risen by more than 30% compared to 2020 levels. The increase mainly comes from the growing energy demand linked to AI systems and large-scale digital infrastructure.

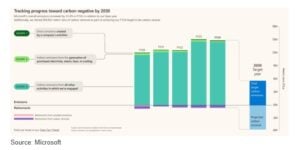

At the same time, the tech giant continues to pursue some of the corporate world’s most aggressive climate goals. The company plans to become carbon negative by 2030, meaning it intends to remove more carbon from the atmosphere than it emits each year.

Diversifying Carbon Removal Investments

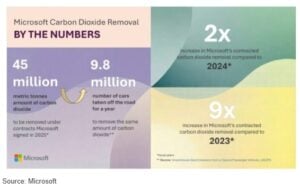

To support these goals, Microsoft has invested heavily in carbon removal projects worldwide. By 2025, the company had committed more than $750 million to carbon removal initiatives and contracted around 45 million tonnes of carbon removals.

These include BECCS, direct air capture, mineralization, and other engineered removal systems. This strategy allows the company to reduce risks while helping multiple carbon removal technologies scale commercially.

The BioCirc agreement strengthens Microsoft’s BECCS portfolio while supporting a project with relatively high technical readiness. BioCirc’s existing biogas operations and integrated infrastructure make the project more commercially practical compared to some earlier-stage carbon removal technologies.

The company also believes its model can expand beyond Denmark. BioCirc said the system could eventually be replicated across Europe’s more than 1,500 biomethane production sites.

Overall, the whole deal shows that BECCS projects could play a larger role in helping industries and governments meet long-term climate targets while building new low-carbon energy systems.

Canada has reached a new agreement with Alberta that reshapes the country’s industrial carbon pricing system. The deal involves a financial commitment of up to C$600 million from each party, the federal government and Alberta. This agreement is represented by Premier Danielle Smith and Prime Minister Mark Carney.

The funds will support carbon capture and storage (CCS) projects between 2030 and 2040. These projects aim to reduce emissions from heavy industry, especially oil and gas operations in Alberta.

At the center of the agreement is a broader policy shift. Alberta will raise its industrial carbon price. The goal is $130 per tonne by 2040. Interim increases will begin this decade.

The deal also connects carbon pricing with future energy infrastructure plans. This includes potential pipeline development, which remains politically sensitive across Canada.

Taken together, the agreement signals a new phase in Canada’s climate strategy. It links emissions pricing, industrial competitiveness, and large-scale infrastructure planning in one policy framework.

How Canada’s Industrial Carbon Pricing System Is Changing

Canada already has a national carbon pricing system, but provinces can design their own frameworks if they meet federal standards. This creates a mixed system that combines federal oversight with provincial flexibility.

Under the new Alberta–Ottawa agreement, the industrial carbon price will rise gradually over time. The goal is to increase predictability for companies while still pushing long-term emissions reductions.

Key elements of the plan include:

A rising carbon price path toward $130/t by 2040

Annual benchmark increases through the 2030s

Stronger compliance rules under Alberta’s TIER system

This structure reflects a shift away from short-term carbon pricing signals. Instead, Canada is moving toward long-term “price certainty” for industrial emitters.

Economists often argue that stable carbon prices are more effective than volatile systems. They allow companies to plan long-term investments in cleaner technology. However, critics say the pace of change is still too slow to meet climate targets.

CCS Becomes Canada’s Bridge Between Oil and Net Zero

A central feature of the agreement is the joint investment in carbon capture and storage. Under Friday’s agreement, Alberta and the federal government will jointly invest up to C$1.2 billion in carbon capture and storage projects, with the cost split equally between both parties.

This means each side will contribute up to C$600 million to support CCS deployment. Carbon capture is a technology that traps CO₂ emissions from industrial facilities. The gas is then stored underground in geological formations.

In Alberta, CCS is mainly focused on oil sands and heavy industry. These sectors are among the most carbon-intensive parts of Canada’s economy.

Supporters argue that CCS is necessary because emissions from these industries are difficult to eliminate quickly. They say it can reduce emissions while keeping industrial production active.

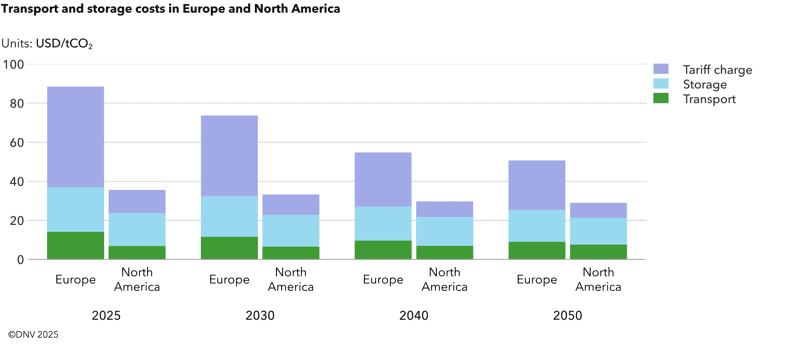

But CCS remains expensive. Global projects often depend on government support to remain viable. Costs can vary widely depending on location, technology, and storage conditions. The DNV report forecasts the CCS costs in North America and Europe as follows:

The Canadian government has also linked CCS investment to future industrial development. In some cases, it is seen as a condition for infrastructure approvals, including potential pipeline expansion.

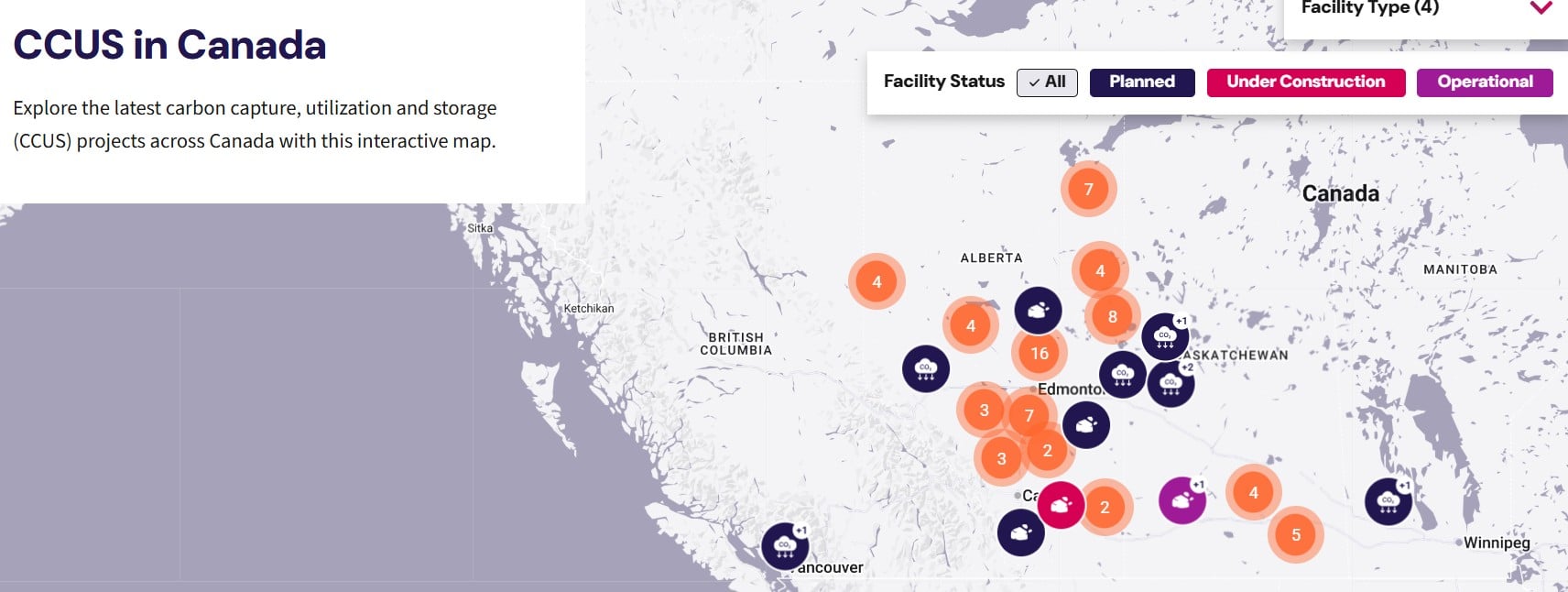

Canada already operates several large-scale CCUS facilities, mainly in Alberta and Saskatchewan. One of the largest is the Quest Carbon Capture and Storage Project in Alberta, which captures and stores about 1 million tonnes of CO₂ annually.

The North American country is also emerging as a major player in the global CCUS market. Canadian projects account for roughly 11.5% of planned global carbon capture storage capacity.

Source: Canadian Energy Centre

National CCUS capacity could grow from about 4.4 million tonnes of CO₂ per year today to around 16.3 million tonnes annually by 2030. The federal government is also supporting the sector through programs like the Energy Innovation Program, which funds CCUS research, clean energy technologies, and smart grid development to help support Canada’s 2050 net-zero target.

Industrial Climate Policy Moves From Short-Term to Long Horizon

Canada has long committed to reaching net-zero emissions by 2050. However, industrial emissions remain one of the hardest challenges.

Oil and gas production accounts for roughly a quarter of Canada’s total greenhouse gas emissions, according to federal climate data. This makes Alberta central to national climate policy.

At the same time, Canada is trying to expand energy exports. This creates a policy tension between climate goals and economic growth. The new agreement tries to balance both sides. It keeps the long-term net-zero target while allowing continued fossil fuel development under stricter carbon pricing rules.

Source: Government of Canada

Recent policy changes also show this balancing act. Canada has rolled back some emissions caps for the oil and gas sector while strengthening carbon pricing mechanisms.

Officials say this approach aims to maintain investment while still driving emissions reductions over time. Critics argue that delaying stricter limits could slow Canada’s progress toward its climate goals.

One of the biggest drivers of the deal is economic pressure on Alberta’s energy sector. High-emission industries face rising compliance costs under carbon pricing systems. As carbon prices increase, companies must either reduce emissions or pay higher fees.

Current provincial systems already impose costs on large emitters. The federal system also sets a minimum price that rises over time.

According to government data, Canada’s carbon price floor is scheduled to increase gradually toward higher levels by 2030 and beyond. For Alberta, this creates both risk and opportunity.

On one hand, higher carbon prices increase operating costs for oil and gas producers. On the other hand, they create incentives for cleaner technologies and efficiency upgrades.

Industry groups often warn that higher carbon costs could reduce competitiveness compared to countries with weaker climate rules. However, supporters of carbon pricing argue that it helps align Canada with global climate standards and reduces long-term transition risks.

Infrastructure, Pipelines, and Climate Policy Are Now Linked

The agreement also ties climate policy more closely to energy infrastructure development. Reports suggest the deal could help support future pipeline expansion tied to Canadian oil exports.

Canada remains one of the world’s largest oil producers, exporting roughly 4 million barrels per day to global markets. At the same time, the oil and gas sector accounts for about 31% of the country’s total greenhouse gas emissions.

The federal government has said future infrastructure growth must align with stricter carbon pricing and emissions reductions, including carbon capture deployment. This reflects a broader shift where climate policy is increasingly linked to industrial investment and export strategy.

Canada’s Carbon Market Is Entering a New Phase

Canada’s carbon pricing system is becoming more long-term and industry-focused, with Alberta now playing a central role through its Technology Innovation and Emissions Reduction (TIER) system.

Alberta’s TIER market is already one of Canada’s largest compliance carbon systems. Large industrial emitters that cut emissions below required levels can earn carbon credits.

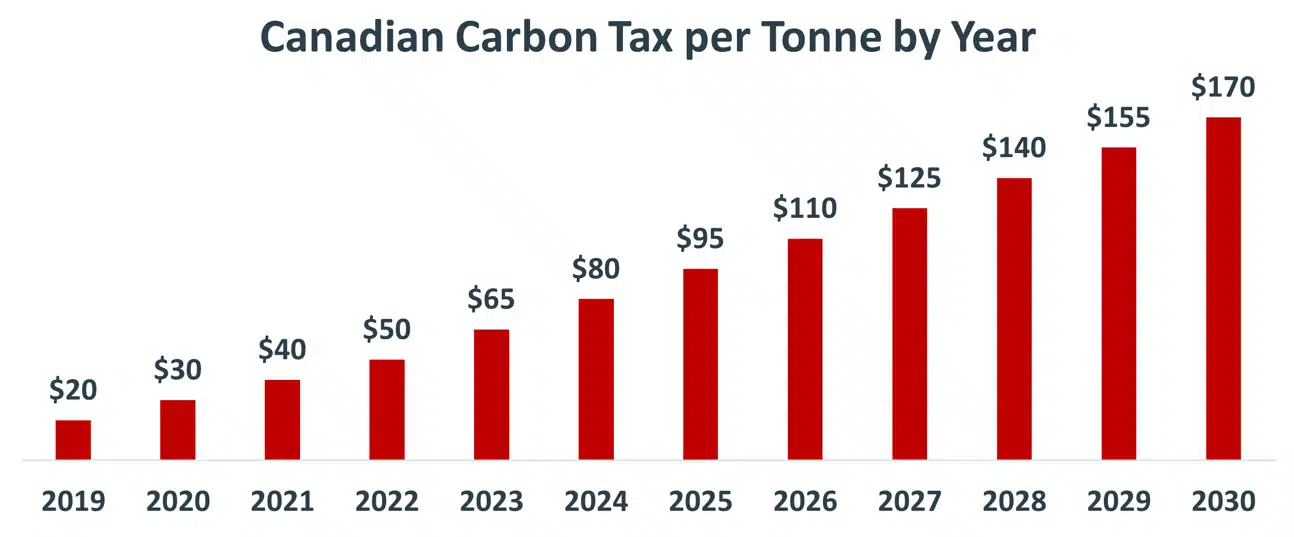

In contrast, those with higher emissions must buy credits or pay compliance costs. The federal carbon benchmark is also set to rise to C$170 per tonne by 2030.

Source: RBN Energy LLC website

The changes come as carbon pricing expands globally. According to the World Bank, carbon pricing systems now cover about 24% of global greenhouse gas emissions worldwide.

At the same time, Canada is increasingly linking carbon pricing, carbon credits, carbon capture, and energy infrastructure into one broader industrial strategy. The goal is to reduce emissions while giving companies more certainty for long-term investment and competitiveness.

The new Ottawa-Alberta carbon agreement reflects a political and economic compromise. It supports continued industrial activity while seeking to strengthen the credibility of climate policy.

The success of this approach will depend on how effectively carbon capture technologies scale, how industries respond to rising carbon prices, and whether long-term investments in clean infrastructure deliver real emissions reductions.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-05-20 10:15:112026-05-20 10:15:11Canada’s $600M Carbon Pricing Deal Signals a New Push for Carbon Capture

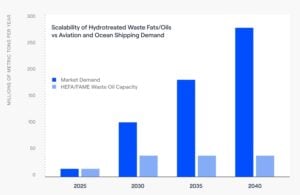

Singapore-based companies FlyORO Technologies Pte. Ltd. and Aether Fuels have signed a non-binding Memorandum of Understanding (MOU) to develop sustainable aviation fuel (SAF) infrastructure. Their focus includes blending, logistics, and supply chain development.

This agreement supports Aether’s SAF initiative, Project Beacon, and future projects. The partnership will explore advanced fuel production, blending systems, storage, certification, and delivery networks.

The aviation industry needs to cut carbon emissions. Airlines worldwide seek cleaner fuel options to meet climate goals and reduce fossil fuel use. However, SAF production is still limited. Better infrastructure and scalable technologies are essential to meet future demand.

And this partnership aims to tackle these challenges.

FlyORO and Aether believe that advanced fuel production and modular blending systems can improve SAF availability and efficiency. They also want to enhance Singapore’s role as a hub for aviation innovation and sustainable growth.

Jonathan Yeo, Chief Executive Officer, FlyORO Technologies Pte. Ltd. said:

“Singapore is one of the few markets where advanced fuel production, airport demand, logistics capability and policy momentum can come together at meaningful speed. Through this MOU, we want to explore how smarter downstream infrastructure can complement next-generation SAF production and help make supply more flexible, transparent and practical for the local market.”

Project Beacon: Southeast Asia’s First Next-Generation SAF Facility

At the heart of this collaboration is Project Beacon, Aether’s planned facility at the Aster Pulau Bukom refinery.

Aether claims this project could be the first commercial-scale SAF facility in Southeast Asia. It will use advanced fuel conversion technology, applying its Aurora technology to convert industrial waste gas and biomethane into SAF.

The facility aims to produce about 50 barrels of SAF daily, or nearly 2,000 tonnes annually. Aether estimates this fuel could reduce lifecycle greenhouse gas emissions by over 70% compared to traditional jet fuel.

Why It Stands Out

Project Beacon is unique because it uses a different production method than many existing SAF projects. Most current SAF production relies on the HEFA pathway, which mainly uses waste fats, oils, and greases. While this method has grown the market, feedstock availability is still a concern.

Aether believes its Aurora technology can address this challenge.

Instead of relying on a single feedstock, Aurora can use various waste carbon sources, such as industrial off-gases and biomethane. This flexibility may boost fuel yields, lower costs, and support larger SAF production in the future.

Source: Aether

The gap between SAF demand and supply is a growing concern for aviation. Governments, airlines, and corporate customers are increasing their sustainability commitments, leading to strong long-term demand for cleaner fuels.

Conor Madigan, Founder and Chief Executive Officer, Aether Fuels, noted:

“Project Beacon is intended to demonstrate Aether’s breakthrough Aurora technology in commercial operation and unlock new and more abundant waste carbon feedstocks for SAF production. Working with FlyORO on this project gives us an opportunity to evaluate how downstream blending and supply-chain innovation can support commercialization in Singapore and accelerate overall SAF industry development.”

Aether Fuels: Pioneering Flexible and Scalable SAF Growth

Aether Fuels emphasizes that the future of SAF relies on scalable, flexible, and cost-effective production.

The aviation and shipping sectors may need nearly one billion metric tonnes of sustainable fuel annually by 2050 to achieve global net-zero goals. Replacing high-energy fuels for long-distance travel with battery technology is challenging.

Source: Aether

Thus, sustainable liquid fuels will remain vital for reducing emissions in these industries.

However, the SAF industry faces a major hurdle. Demand is rising quickly, but supply is limited due to existing pathways that depend on restricted feedstock and costly infrastructure.

Aether believes next-generation technologies must leverage abundant waste-carbon sources to close this supply gap. Aurora was developed with this goal in mind.

Producing SAF is just one part of the process. The fuel must also flow efficiently through the supply chain to reach airports and airlines. That’s where FlyORO’s blending technology is crucial.

FlyORO: Innovating Blending Technology for the Partnership

FlyORO’s role in this collaboration focuses on blending and fuel logistics. The company will assess how its AlphaLite blending system can support Project Beacon and future Aether SAF initiatives.

AlphaLite is a modular SAF blending unit housed in a 40-foot container. It can integrate with existing fuel infrastructure and function at various points in the aviation fuel supply chain, including production sites, terminals, and airport fuel farms.

One key advantage of AlphaLite is its flexibility. Operators can choose where blending is most efficient based on logistics, costs, infrastructure, or regulations.

FlyORO also highlighted AlphaLite’s “last-mile blending” capability. This allows blending closer to airports or final delivery points instead of transporting pre-blended fuel over long distances.

This approach enhances traceability, transparency, and operational efficiency.

It can also help airlines and fuel suppliers manage sustainability reporting and book-and-claim systems better.

The company designed the AlphaLite platform to align with evolving global SAF standards and regulations. As international SAF policies change, the company expects its technology to adapt while maintaining fuel quality and safety.

FlyORO has already tested AlphaLite in a real airport setting. In 2025, the company deployed the system with Wagner Sustainable Fuels and Boeing at Toowoomba Wellcamp Airport.

Source: FlyORO

This project marked the world’s first SAF blending terminal at an airport. It showed that modular blending systems can operate effectively in live aviation conditions.

The deployment also helped AlphaLite achieve Technology Readiness Level 9 (TRL 9), confirming its success in commercial operations.

As of May 2026, FlyORO reported blending over 500,000 liters of SAF through AlphaLite deployments.

This experience could help assess how modular blending systems might support Project Beacon and future Aether projects.

Singapore Strengthens Its Role in Sustainable Aviation

The proposed partnership highlights Singapore’s rising role in clean energy and sustainable aviation.

Singapore is already a global hub for aviation, shipping, and fuel trading. Now, it aims to be a center for low-carbon fuel technologies and sustainable projects.

Aether and FlyORO are joining forces. By combining Aether’s waste-carbon tech with FlyORO’s blending skills, they aim to boost SAF use in aviation.

Both firms believe this partnership could increase SAF availability. It may also enhance supply chain flexibility and support long-term aviation decarbonization goals.

However, the MOU remains non-binding and non-exclusive. Future commercial partnerships will depend on technical studies, regulatory approvals, negotiations, and final agreements.

The agreement shows that the aviation industry is dedicated to scalable and practical SAF solutions. Airlines are working hard for lower-carbon operations.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-05-20 10:15:102026-05-20 10:15:10Singapore-Based FlyORO and Aether Fuels Team Up to Explore Smarter SAF Blending and Fuel Delivery Solutions

Europe’s two largest automakers, BMW and Volkswagen, are moving in very different directions on electric vehicles and emissions compliance. One is scaling EV production at speed. The other is facing rising regulatory costs linked to carbon targets.

Together, their latest results highlight a shifting global auto industry. Growth in electric vehicles is accelerating. But so are the financial risks tied to emissions rules.

Volkswagen’s Carbon Bill Keeps Growing Under Tougher EU Rules

Volkswagen Group is under growing pressure from Europe’s tightening emissions rules. During its Q1 2026 earnings call, the company said it expects to pay up to €1.5 billion ($1.75 billion) in CO₂ fines between 2025 and 2027. These penalties are linked to failure to meet EU fleet-wide emissions targets.

CFO Arno Antlitz said annual costs will likely range between €300 million and €500 million per year over the compliance period. Even with new EV models coming to market, Volkswagen said it will still fall short of EU requirements.

The financial impact comes at a weak earnings moment. Volkswagen’s operating profit fell 14.3% year-on-year to about €2.5 billion, while revenue came in at €75.66 billion, below expectations. Net profit also dropped 28% to €1.56 billion.

Image from Arno Antlitz’s LinkedIn post

CEO Oliver Blume pointed to several pressures, including geopolitical tensions, trade barriers, and strict regulations. He also confirmed that Volkswagen is cutting costs, including plans to eliminate 50,000 jobs in Germany by 2030.

Following these results, Volkswagen’s stock price went down but started to recover in May.

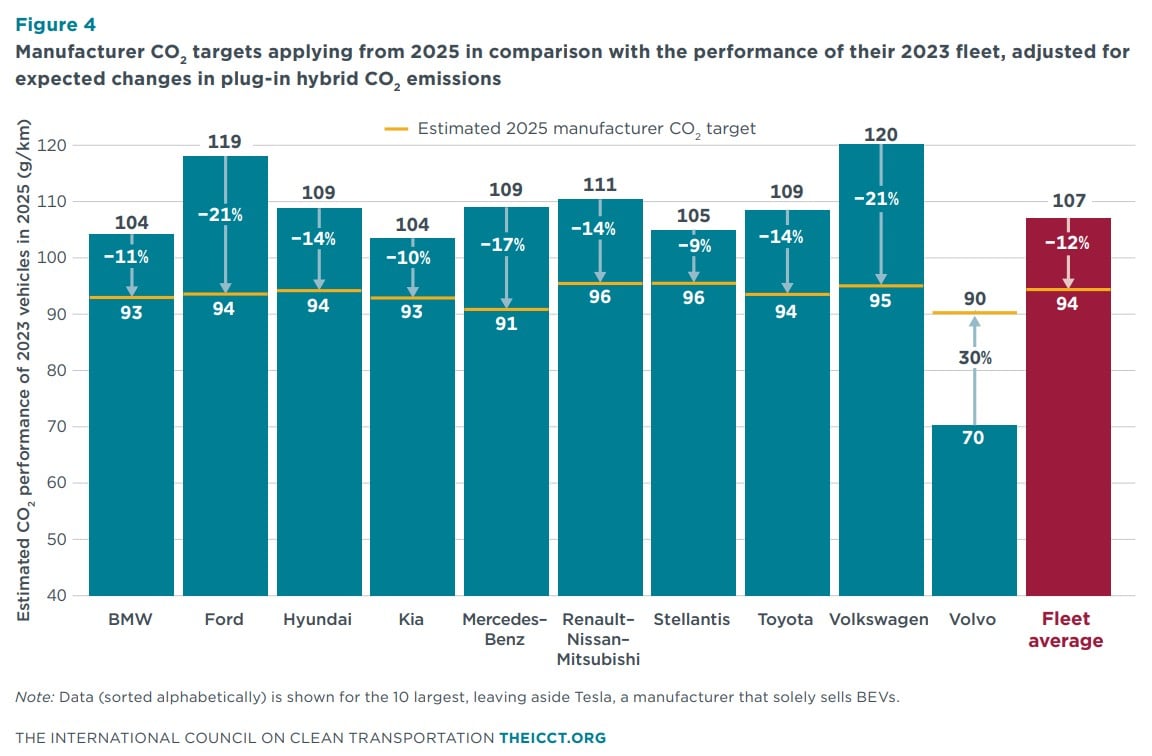

The company is also facing a long-term challenge. EU rules will tighten further. By 2030, automakers must cut CO₂ emissions by 55% versus 2021 levels, and by 2035 the reduction target rises to 90%.

Source: ICCT

Even with cheaper EV models coming, Volkswagen has admitted that electric vehicles still generate up to 30% lower profit margins than combustion engines. This makes the transition financially difficult in the short term.

BMW Hits 2 Million EVs as Production Accelerates

While Volkswagen faces penalties, BMW is scaling electric production quickly.

The BMW Group confirmed it has now produced its two millionth fully electric vehicle. The milestone vehicle was a BMW i5 M60 xDrive, built at Plant Dingolfing in Germany and delivered to a customer in Spain.

BMW’s EV ramp-up has accelerated sharply. It took the company nearly 11 years to reach its first one million EVs after the launch of the i3 in 2013. The second million took just about two years.

This reflects a major shift in production speed and demand alignment.

Plant Dingolfing is now BMW’s key EV hub. Since 2021, it has produced more than 320,000 electric vehicles, including models like the iX, i5, and i7. In 2025, more than 25% of production at the site was fully electric.

BMW is also using a flexible production system. It builds electric, hybrid, and combustion models on shared production lines. This allows the company to adjust faster to market demand. The luxury carmaker also aims for EVs to make up more than 50% of total annual sales by 2030.

Mixed Global EV Demand Shapes Industry Strategy

Despite production growth, EV demand remains uneven across regions for BMW. In 2025, BMW delivered 442,072 fully electric vehicles worldwide, showing moderate overall growth.

Europe remains the strongest market. EV sales there rose 28%, and now about one in five cars sold in the EU is fully electric. But performance is weaker in other regions.

U.S. EV sales fell 16.7% to 42,484 units

Fourth-quarter sales dropped 45.5%, after EV tax credits were removed

China sales also declined by double digits

At the same time, plug-in hybrid sales in the U.S. rose by more than 30%, showing that many buyers are shifting to partial electrification instead of full EV adoption.

This uneven demand is shaping automaker strategies. Companies are balancing full EV expansion with hybrid production to manage risk.

Two Auto Giants, Two Very Different ESG Paths

The contrast between BMW and Volkswagen also reflects different ESG outcomes.

Volkswagen is facing rising regulatory costs linked to Europe’s stricter emissions rules. At the same time, the company targets net-zero emissions across its value chain by 2050 and plans to become carbon neutral in Europe by 2040.

Source: Volkswagen

The automaker claims it cut production CO₂ emissions per vehicle by over 50% since 2018. This was achieved using renewable electricity, improving energy efficiency, and adopting lower-carbon manufacturing.

However, Volkswagen still faces pressure from slower EV profitability and the high cost of transitioning away from combustion-engine vehicles. The company has acknowledged that some EV models generate lower margins than traditional gasoline vehicles.

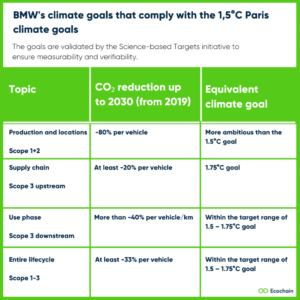

BMW, meanwhile, continues expanding EV production without facing similar emissions penalties. The company aims to cut lifecycle CO₂ emissions per vehicle by at least 40% by 2030 versus 2019 levels and targets climate neutrality across its value chain by 2050.

Source: BMW

The carmaker says it has already reduced operational CO₂ emissions by more than 70% since 2006 and now sources 100% renewable electricity for its global production network.

BMW is also increasing the use of recycled materials in batteries and vehicle production. The company says its Neue Klasse EV platform will reduce production emissions by up to 40% per vehicle compared with current models.

Both automakers remain under growing pressure to decarbonize further. By 2035, Europe plans to phase out most new combustion-engine vehicle sales entirely.

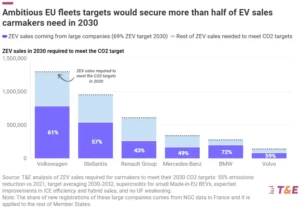

Transport & Environment (T&E) said the EU’s proposed 45% electrification target for new company cars is too low to fully boost EV demand. The group analyzed a higher 69% target that excludes plug-in hybrids and found it would significantly increase EV sales for major automakers. Under this scenario, BMW could secure 72% of its EV sales from corporate fleets, while Volkswagen Group could secure 61%, and Volvo Cars about 59%.

Source: T&E report

Industry Competition Intensifies as EV Transition Speeds Up

Competition across the global auto industry is increasing as EV adoption grows. Volkswagen recently reached its own milestone of 2 million EVs produced, just months after hitting its first million. This shows how quickly production is scaling across major automakers.

However, speed alone is not enough. Companies must also manage costs, margins, and regulatory compliance.

BMW’s approach focuses on gradual scaling with flexible production systems. Volkswagen’s approach is more aggressive but comes with higher financial pressure from emissions fines and restructuring costs.

Both companies now face a similar long-term challenge. EVs must become profitable while also meeting strict carbon reduction rules.

A Tale of Two EV Strategies

BMW and Volkswagen show two different paths through Europe’s EV transition. BMW is scaling production quickly and steadily increasing EV share across its plants and markets. It is avoiding major emissions penalties while gradually shifting its product mix.

Volkswagen is moving through a more difficult transition. It faces up to €1.5 billion in CO₂ fines, weaker profits, and rising restructuring costs as it adapts to EU climate rules.

Both companies are moving toward the same endpoint: lower emissions and higher EV adoption. But their financial and operational journeys are very different.

As EU regulations tighten further toward 2030 and 2035, the gap between compliance leaders and laggards may widen even more.

For the global auto industry, the message is clear. EV transition is no longer optional. It is now a regulated, high-cost transformation that is reshaping profitability, production, and long-term strategy.

Amazon is accelerating its push into carbon-free energy as artificial intelligence (AI) drives a massive new wave of electricity demand. The company announced plans to invest in 700 megawatts (MW) of clean energy projects in Nevada. This will help support future data center operations near Reno.

The portfolio includes 100 MW of geothermal energy from Zanskar and 600 MW of solar power paired with 600 MW of battery storage from Primergy.

The move comes as Amazon expands its AI and cloud infrastructure through Amazon Web Services (AWS). It shows a bigger trend in global energy markets. Major tech companies are racing to get reliable, carbon-free electricity they need to power their energy-hungry AI systems.

Amazon shares also moved higher after the company announced its new Nevada clean energy investments tied to future AI and cloud expansion. The next day, Amazon stock closed at $270 per share, extending its strong 2026 rally as investors continued backing major AI infrastructure companies.

The stock has gained sharply in recent months as Wall Street grows more optimistic about AWS, artificial intelligence demand, and the company’s long-term energy strategy.

At the same time, Amazon faces growing pressure to balance AI growth with its climate commitments. Rising demand for data centers is boosting electricity use. This makes energy sourcing one of the company’s biggest long-term challenges.

Geothermal Steps Into the Spotlight as “Always-On” Clean Power

Amazon said the Nevada projects will help power future AWS data centers while supporting grid reliability in the state.

The agreement with NV Energy marks the tech giant’s first data center energy deal involving geothermal power. Unlike solar and wind, geothermal energy can generate electricity continuously, regardless of weather conditions.

Amazon described geothermal as an important addition to its energy mix because it provides “firm” carbon-free power around the clock. The company said the battery storage will stabilize the electricity supply. It stores solar energy when production is high and releases it when demand increases.

Amazon said:

“Geothermal is a particularly exciting addition to Amazon’s carbon-free energy portfolio powering our data centers. Unlike other renewable sources that fluctuate with weather or time of day, geothermal harnesses the Earth’s constant internal heat to generate power around the clock.”

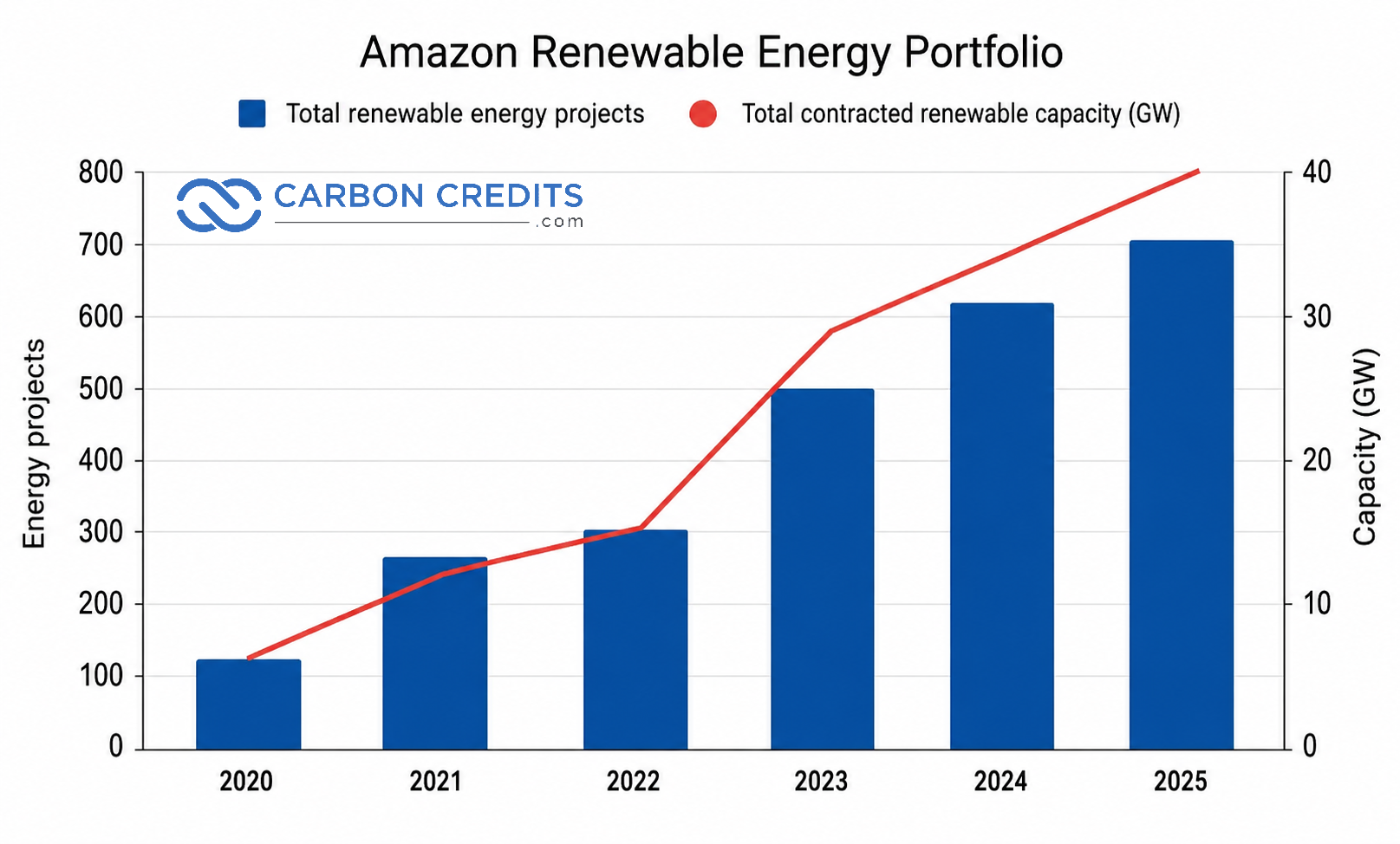

The projects are part of Amazon’s rapidly expanding clean energy portfolio. The tech giant has invested in over 700 renewable and carbon-free energy projects worldwide. This totals more than 40 gigawatts (GW) of generating capacity currently.

AI Is Driving a Massive New Wave of Electricity Demand

The Nevada announcement comes as Amazon aggressively expands its AI capabilities under CEO Andy Jassy. He said:

“I don’t think the world has ever seen a technology get this much adoption and grow this quickly… You can choose to howl at the wind, but AI is not going away.”

AWS remains one of the largest cloud computing platforms in the world. The company is investing a lot in generative AI systems, AI chips, and large data centers. This move is meant to compete with rivals like Microsoft, Google, and Meta Platforms.

That expansion is creating enormous new energy needs. The International Energy Agency estimates that global data centers consumed about 415 terawatt-hours (TWh) of electricity in 2024. The agency expects this figure to climb to nearly 945 TWh by 2030 as AI adoption accelerates.

Source: IEA

Amazon is already redesigning data centers to handle the next generation of AI hardware. AWS started an internal project named “Titus.” Its goal is to boost power density, enhance cooling systems, and improve energy efficiency for AI tasks. This uses advanced chips from NVIDIA.

The company is also working to reduce build times for new AI facilities while increasing electricity capacity per site. This reflects a broader shift happening across the tech sector.

AI infrastructure is no longer limited by computing hardware alone. Electricity supply and grid access are becoming major competitive factors.

Amazon’s Climate Goals Face Pressure From AI Expansion

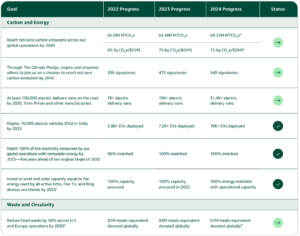

Amazon’s clean energy investments are also tied closely to its climate targets. The company co-founded “The Climate Pledge,” which commits it to reach net-zero carbon emissions by 2040. Below is the company’s progress on its carbon and energy targets:

Source: Amazon

The tech firm met its goal of using 100% renewable energy for its electricity seven years early. It reached this target in 2023 instead of 2030. However, emissions remain a major challenge.

Amazon’s operational carbon emissions have increased significantly in recent years as AWS and AI infrastructure have expanded. A recent United Nations report showed that Amazon’s indirect operational emissions increased by about 182% from 2020 to 2023. This was the largest rise among major AI-focused tech companies studied.

The company has acknowledged that AI growth is making emissions reductions more difficult.

Amazon is investing a lot in different energy technologies. This includes solar, wind, geothermal, battery storage, and nuclear energy. The tech giant says carbon-free electricity investments help stabilize grids, support local infrastructure, and reduce long-term exposure to fossil fuel volatility.

The company is now focusing more on energy-efficient data center designs. They are also working on advanced cooling systems and flexible power architectures. This aims to reduce electricity use for each computing workload.

Geothermal, Nuclear, and the Rise of Baseload Clean Energy

The Nevada projects also show how technology companies are shifting toward more stable energy sources. Solar and wind remain important, but many AI operators now need electricity that can run continuously 24 hours a day. That is increasing interest in geothermal and nuclear energy.

Amazon has already invested in several nuclear-related initiatives tied to small modular reactor (SMR) development and nuclear-powered data center infrastructure.

Geothermal energy is now attracting similar attention because it can provide steady baseload electricity with low emissions. This matters because AI systems consume far more electricity than traditional cloud workloads. Large AI models require dense clusters of GPUs operating continuously, which increases both power and cooling needs.

Industry analysts increasingly view firm carbon-free energy as one of the most valuable assets in the AI economy. As a result, technology companies are competing for more than just advanced chips. They also want access to a stable electricity infrastructure.

Orbital Data Centers Show How Far the AI Race Is Expanding

Amazon’s energy expansion comes as the broader AI industry explores even more ambitious infrastructure concepts. Reports recently revealed that Google has discussed orbital data center projects with SpaceX as companies search for long-term solutions to AI power constraints.

The concept involves placing solar-powered computing infrastructure in space to bypass terrestrial grid limitations. While orbital computing remains highly experimental, the discussions highlight how rapidly AI energy demand is growing.

Analysts estimate future AI infrastructure could require trillions of dollars in investment across:

data centers,

transmission systems,

cooling technologies,

battery storage, and

power generation.

Many experts now see electricity infrastructure as one of the defining investment themes of the AI era.

AI Is Now an Energy Infrastructure Race

Amazon’s Nevada projects highlight a major shift happening across both the technology and energy sectors. As AI systems become larger and more power-intensive, access to reliable carbon-free electricity is becoming critical for future growth.

The broader industry now faces a difficult balancing act. Technology companies want to scale AI infrastructure rapidly, but they must also secure enough clean electricity to avoid significantly increasing emissions.

For Amazon and the wider tech sector, energy strategy is quickly becoming just as important as computing strategy itself.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-05-19 11:14:582026-05-19 11:14:58Amazon (AMZN) Stock Rises as It Bets on Geothermal Power with AI Data Centers Triggering a New Energy Supercycle

Disseminated on behalf of Alaska Energy Metals Corporation.

The global energy narrative has shifted again. What began as a climate-driven transition is now increasingly shaped by geopolitics, supply chain risks, and national security concerns. In 2026, energy security and decarbonization have become the dominant drivers of policy and investment decisions.

According to the IEA, nearly 80% of energy experts ranked energy security as a top priority in 2025, ahead of emissions reduction and affordability. This shift is transforming how markets value critical minerals. Among them, nickel is emerging as a strategic asset, not just a commodity.

Source: IEA

The Return of Energy Security – and Why Nickel Is at the Center

Recent geopolitical shocks have exposed vulnerabilities in global energy systems. Disruptions in oil and gas flows and ongoing global tensions have pushed prices higher and accelerated demand for alternative energy systems. However, electrification brings its own dependencies, particularly on battery metals.

Nickel sits at the core of this transition because it plays a critical role in high-energy-density EV batteries, especially nickel-manganese-cobalt (NMC) chemistries.

It improves battery range, efficiency, and performance, making it essential for electric vehicles, grid storage, and industrial electrification.

Demand trends reflect this growing importance. Nickel demand for clean energy is expected to more than double by 2030, while battery-grade nickel demand continues to grow at a double-digit pace annually. At the same time, the global nickel market is expanding rapidly in value terms, highlighting strong long-term fundamentals.

Source: IEA

Yet supply remains fragile. A large portion of global nickel production and processing is concentrated in Indonesia and China. This concentration creates geopolitical exposure and environmental concerns. Even when supply is available, refining constraints and processing complexities can limit the availability of battery-grade material.

As a result, nickel is no longer priced purely on traditional supply-demand dynamics. Instead, it is increasingly valued based on security, reliability, and strategic access.

Quality Over Quantity: The Strategic Premium of Sulphide Nickel

The nickel market is no longer just about volume. It is now about quality. A key distinction has emerged between laterite nickel and sulphide nickel, and this difference is shaping investment decisions.

Laterite deposits are more abundant but require complex and energy-intensive processing methods. In contrast, sulphide deposits are easier to process into high-purity Class 1 nickel, which is required for EV batteries. This simpler processing route reduces costs, emissions, and technical risks.

Sulphide nickel also aligns better with environmental, social, and governance (ESG) goals. It produces fewer emissions and integrates more easily into clean energy supply chains. However, sulphide deposits are relatively rare, and most known high-quality resources have already been developed.

This scarcity is creating a premium for sulphide-based projects. Automakers and battery manufacturers are increasingly prioritizing high-purity, low-carbon, and geopolitically secure supply sources. The focus has shifted from simply securing more nickel to securing the right kind of nickel.

AEMC’s Nikolai Project: From Mining Asset to Strategic Infrastructure

Alaska Energy Metals Corp.’s Nikolai project stands out in this evolving landscape. It is not just a mining project but a strategic asset that aligns closely with the United States’ energy security priorities.

Proximity to U.S. Gigafactories

The United States is rapidly expanding its domestic battery manufacturing capacity. New gigafactories are being developed to support electric vehicle production and energy storage systems. As a result, the need for secure, local sources of critical minerals is increasing.

Nikolai’s location in Alaska provides a geographic advantage. It sits within reach of North American battery hubs, reducing reliance on long and vulnerable international supply chains. This proximity lowers transportation risks and supports the broader push toward supply chain localization.

Source: AEMC

Stable Jurisdiction and Permitting Advantage

The United States offers a strong regulatory framework, transparent permitting processes, and growing policy support for critical minerals. The nickel junior is advancing its Nikolai project with support from the U.S. government.

In its latest press release, AEMC said it is continuing to work with the U.S. Administration and key government agencies to advance its critical minerals strategy. The company is exploring strategic funding opportunities, partnerships, and policy programs designed to support domestic mineral production and build more resilient supply chains.

AEMC also said that, through the Department of Defense’s Defense Industrial Base Consortium (DIBC), it responded to a new call for projects eligible for Defense Production Act Title III funding. The company submitted a proposal for its Nikolai project, which received a “MET” rating. AEMC noted that requests for more detailed proposals under this funding program could begin as early as May 2026.

Thus, Nikolai is more than a nickel project. It is becoming a strategic U.S. asset. It supports both clean energy goals and defense supply chain security.

Low-CO₂ Sulphide Resource: Built for the Energy Transition

Nikolai’s sulphide-style mineralization is a key advantage. Compared to laterite operations, sulphide deposits require less energy-intensive processing, resulting in lower carbon emissions.

This is increasingly important as automakers face pressure to reduce emissions across their entire value chains. It is no longer enough to produce zero-emission vehicles. The materials used in those vehicles must also meet strict environmental standards.

A low-carbon nickel source with clear traceability and strong ESG credentials becomes highly attractive in this context. Nikolai fits well within this requirement, positioning it as a future-ready supply option.

Multi-Metal Exposure: A Full Energy Transition Package

The Nikolai project also offers exposure to multiple critical metals beyond nickel. These include copper, cobalt, and platinum group metals, all of which play essential roles in the energy transition.

These materials are used in electric vehicles, renewable energy systems, and emerging technologies such as hydrogen production. This multi-metal profile enhances the project’s strategic value and reduces reliance on a single commodity.

Source: AEMC

It positions Alaska Energy Metals Corp. as a broader participant in the clean energy supply chain rather than just a nickel-focused company.

The Bigger Shift: From Commodity Cycles to Strategic Positioning

The nickel market is undergoing a structural transformation. Historically, it was driven by stainless steel demand and cyclical economic trends. Today, it is increasingly shaped by energy policy, geopolitics, and technological change.

Buyers are securing long-term supply agreements to reduce risk and ensure stability. Companies are also willing to pay a premium for materials sourced from stable jurisdictions with strong environmental credentials. At the same time, vertical integration across the supply chain is accelerating.

This shift means that nickel assets are now evaluated on more than just cost and scale. Location, carbon footprint, processing efficiency, and alignment with national strategies are becoming equally important.

Conclusion: Nickel as Energy Infrastructure, Not Just a Metal

The return of energy security concerns has fundamentally reshaped the role of critical minerals in the global economy. Nickel has moved beyond its identity as a commodity and is now seen as a foundational element of clean energy systems.

Projects like AEMC’s Nikolai are positioned at the intersection of energy transition, industrial policy, and national security. With its proximity to U.S. gigafactories, stable jurisdiction, and low-carbon sulphide resource, it represents more than a mining opportunity.

It is part of a broader infrastructure layer that will support the next phase of global electrification. As geopolitical tensions persist and demand for clean energy accelerates, a secure and sustainable nickel supply will become increasingly valuable.

In this new landscape, success will depend not just on production volumes but on strategic positioning. And that is where projects like Nikolai are beginning to stand apart.

New Era Publishing Inc. and/or CarbonCredits.com (“We” or “Us”) are not securities dealers or brokers, investment advisers, or financial advisers, and you should not rely on the information herein as investment advice. Alaska Energy Metals. (“Company”) made a one-time payment of $75,000 to provide marketing services for a term of three months. None of the owners, members, directors, or employees of New Era Publishing Inc. and/or CarbonCredits.com currently hold, or have any beneficial ownership in, any shares, stocks, or options of the companies mentioned.

This article is informational only and is solely for use by prospective investors in determining whether to seek additional information. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Examples that we provide of share price increases pertaining to a particular issuer from one referenced date to another represent arbitrarily chosen time periods and are no indication whatsoever of future stock prices for that issuer and are of no predictive value.

Our stock profiles are intended to highlight certain companies for your further investigation; they are not stock recommendations or an offer or sale of the referenced securities. The securities issued by the companies we profile should be considered high-risk; if you do invest despite these warnings, you may lose your entire investment. Please do your own research before investing, including reviewing the companies’ SEDAR+ and SEC filings, press releases, and risk disclosures.

It is our policy that information contained in this profile was provided by the company, extracted from SEDAR+ and SEC filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee them.

CAUTIONARY STATEMENT AND FORWARD-LOOKING INFORMATION

Certain statements contained in this news release may constitute “forward-looking information” within the meaning of applicable securities laws. Forward-looking information generally can be identified by words such as “anticipate,” “expect,” “estimate,” “forecast,” “plan,” and similar expressions suggesting future outcomes or events. Forward-looking information is based on current expectations of management; however, it is subject to known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those anticipated.

These factors include, without limitation, statements relating to the Company’s exploration and development plans, the potential of its mineral projects, financing activities, regulatory approvals, market conditions, and future objectives. Forward-looking information involves numerous risks and uncertainties and actual results might differ materially from results suggested in any forward-looking information. These risks and uncertainties include, among other things, market volatility, the state of financial markets for the Company’s securities, fluctuations in commodity prices, operational challenges, and changes in business plans.

Forward-looking information is based on several key expectations and assumptions, including, without limitation, that the Company will continue with its stated business objectives and will be able to raise additional capital as required. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, or intended.

There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially. Accordingly, readers should not place undue reliance on forward-looking information. Additional information about risks and uncertainties is contained in the Company’s management’s discussion and analysis and annual information form for the year ended December 31, 2025, copies of which are available on SEDAR+ at www.sedarplus.ca.

The forward-looking information contained herein is expressly qualified in its entirety by this cautionary statement. Forward-looking information reflects management’s current beliefs and is based on information currently available to the Company. The forward-looking information is made as of the date of this news release, and the Company assumes no obligation to update or revise such information to reflect new events or circumstances except as may be required by applicable law.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-05-19 11:14:582026-05-19 11:14:58Energy Security Fears Are Back – And Nickel Is Now a Strategic Asset in the Clean Power Race

Ahead of its May 25 annual general meeting, Xpansiv released an investor update that shows where global environmental markets may be heading next.

The report highlights a major shift inside one of the world’s largest environmental commodities platforms. Carbon markets are still important, but electricity-linked infrastructure is now becoming a bigger part of the business. AI, battery storage, and cross-border clean energy trading are also reshaping demand.

The filing also shows that environmental markets are becoming more tied to financial systems. Registries, trading platforms, settlement systems, and market data tools are becoming more important. This is happening as governments and companies deal with more complex energy and climate rules.

Overall, the update points to a key shift. Carbon credits are no longer the only focus. Electricity certificates and digital energy systems are now central to future growth.

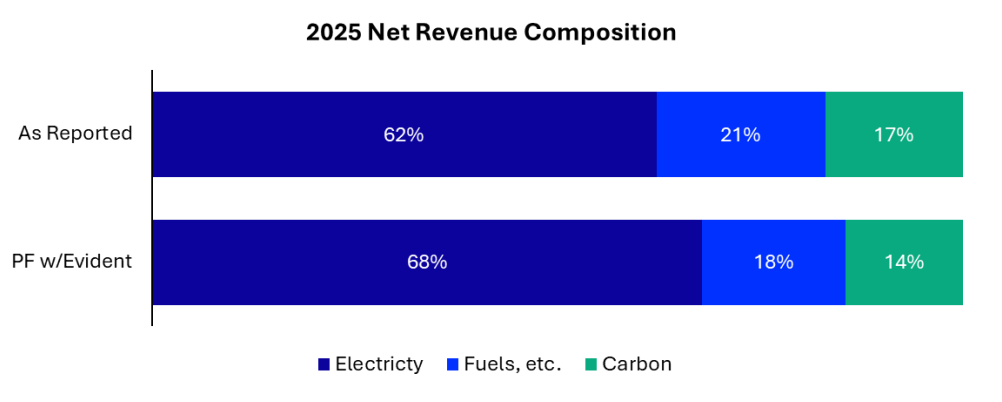

From Carbon Credits to Electricity: Xpansiv’s Market Pivot

The report shows a clear change in revenue mix. Electricity-linked products are now a major driver.

According to Xpansiv, electricity now makes up about 62% of net revenue. This is up from 57% in 2024. On a pro forma basis, including the Evident acquisition for a full year, electricity reaches about two-thirds of total revenue.

Source: Xpansiv

At the same time, carbon revenue fell from 21% to 17%. This reflects wider changes in energy markets.

Companies are buying more renewable electricity certificates (RECs) and clean energy attributes. They are doing this to meet climate targets and secure a stable power supply. Demand is also rising outside regulated markets.

Xpansiv’s system now tracks about 4% of global electricity generation and about 7% of global renewable electricity generation. The company serves customers in more than 90 countries.

The platform has also grown fast. After acquiring Evident, its renewable energy registry network now covers more than 300 gigawatts of capacity and over 4,000 companies.

These figures show that renewable electricity certification is becoming a large global system, not just a niche market. The report says:

“Across every major region, renewable penetration is rising while generation mixes are becoming more distributed and intermittent, which increases the importance of the market infrastructure layer between asset creation, energy attributes, trading workflows, and end-market demand. Electricity-linked products are expected to remain the primary driver of future growth.”

The report also highlights the growing impact of artificial intelligence on electricity demand. Xpansiv said a “step-change in electricity demand from AI compute and data-center build-out has fundamentally reshaped the demand curve of modern power markets.”

Source: Xpansiv

This matches wider trends in the energy sector. Big tech companies are building more AI systems and hyperscale data centers. These facilities use large amounts of electricity. They also need a stable, clean energy supply. Because of this, energy buying is becoming more complex.

Many large buyers now want electricity matched to real-time use. They no longer rely only on yearly offset systems. This is driving demand for hourly renewable energy certificates and 24/7 carbon-free energy tracking.

Xpansiv said it is expanding hourly RECs across its registries to meet this demand. It reported REC retirements of 239 million and 346 million issuances in 2025, both of which show increases from 2024.

Source: Xpansiv

It also said data-center-driven electricity demand is now a “tailwind” for its platform. This includes registries, trading systems, settlement tools, and market data services.

This trend may grow further. AI expansion is not only increasing tech demand. It is also boosting demand for renewable energy, storage systems, and energy tracking tools.

The Rise of Grid-Scale Environmental Market Infrastructure

The report shows that environmental markets are becoming more like financial infrastructure. Companies now need systems that can handle registration, tracking, verification, settlement, and cross-border transfers of environmental assets.

Xpansiv says users transfer about 1 billion environmental assets each year across its platform. The system connects more than 17 renewable energy, carbon, and environmental registries. This growing complexity is pushing governments and exchanges to work with specialized infrastructure providers.

In 2025, Xpansiv signed deals with Korea Exchange and NH Investment & Securities to support Korea’s carbon market. It also expanded work in Saudi Arabia and won a mandate from New York State for emissions reporting.

These moves show that environmental markets are becoming more institutional. Governments and companies now need central systems that can work across different regions and rules.

The company also said demand is growing for interoperability. Through its Xpansiv Connect platform, it aims to bring different systems into one workflow. This makes environmental markets look more like traditional financial markets, with shared systems for trading, clearing, and data.

Battery Storage and Nuclear Enter the Certificate Economy

The update also shows that clean energy markets are widening beyond solar and wind. Xpansiv said it now supports more than 30% of battery storage capacity in California and Texas. These are the two largest storage markets in the United States.

Overall, it supports more than 16 gigawatts of power resources across all seven U.S. independent system operators. Battery storage is becoming more important as renewable energy grows. It helps balance supply and demand on the grid.

Through a partnership with Constellation, Xpansiv launched Emission-Free Energy Certificates (EFECs) linked to nuclear power. It said 675,000 megawatt-hours were traded in the first week. This was its strongest REC-style launch so far.

The strong demand shows a shift toward reliable clean energy sources. AI growth and rising electricity demand are increasing interest in firm power like nuclear.

Carbon Markets Go Digital: Tokenization and AI Integration

The report also points to a more digital future for environmental markets.

Xpansiv said it plans to support tokenized environmental assets using blockchain systems. These could allow digital tracking, smart contracts, and fractional ownership in the future.

It also said it is using AI across its operations. The goal is to improve speed, reduce costs, and scale its systems. This suggests environmental assets may start to behave more like digital financial products.

The company also expects more consolidation in the sector. It plans to acquire new platforms to expand into new regions and reduce fragmentation in registry systems.

A Broader Shift Is Taking Shape

Xpansiv’s update shows that environmental markets are changing quickly.

Electricity-linked products are growing. AI is driving new demand for power. Battery storage and nuclear energy are expanding. Digital systems are becoming more important.

At the same time, environmental commodities are becoming more connected to financial and energy infrastructure. As climate rules tighten and companies face more complex energy needs, the systems that track and trade environmental assets may become as important as the assets themselves.

https://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.png00carbonfundhttps://globalcarbonfund.com/wp-content/uploads/2018/10/GCF_header_logo_340x156.pngcarbonfund2026-05-19 10:14:452026-05-19 10:14:45What Xpansiv’s Latest Investor Update Reveals About the Future of Carbon and Electricity Markets

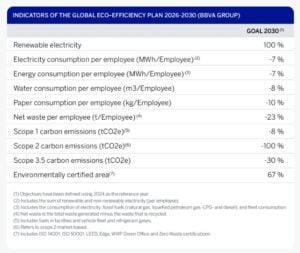

BBVA is strengthening its sustainability strategy with a new environmental roadmap for 2026-2030. The bank says it already achieved the goals from its earlier eco-efficiency plan two years ahead of schedule. Now it wants to move even faster by cutting emissions further, improving energy efficiency, and expanding the use of renewable electricity across its operations.

The latest figures show that BBVA has already made major progress. In 2025, renewable sources supplied 99% of the bank’s electricity use worldwide.

Furthermore, since 2019, the bank has reduced Scope 1 and Scope 2 carbon emissions by 83%. These emissions come from the company’s own operations and purchased energy.

The press release also revealed that the bank lowered electricity use per employee by 22%, total energy consumption by 19%, water use by 36%, paper consumption by 44%, and net waste by 33%. At the same time, environmentally certified office space reached 62%, far above the original 45% target.

Source: BBVA

New Eco-Efficiency Plan Raises the Bar

BBVA’s new 2026-2030 Global Eco-efficiency Plan focuses on reducing the environmental impact of the bank’s direct operations. The strategy builds on the strong results achieved under the 2021-2025 plan.

The bank now plans to source 100% of its electricity from renewable energy in the near future. It also wants to improve energy, paper, and water efficiency per employee while reducing indirect emissions linked to employee activities such as travel and transportation.

Another important target involves green buildings. BBVA aims to ensure that at least two-thirds of its facilities hold environmental certifications by the end of the decade.

The bank designed the new roadmap with input from local teams across all countries where it operates. This approach allows BBVA to maintain a global strategy while adapting solutions to local market conditions.

Alberto Agustín, Head of Premises and Services at BBVA, said:

“The new plan is a key lever to reduce the environmental impact of our direct activities. This approach reinforces our commitment to more efficient building management by relying on technology and increasingly stringent standards. We are building on a very strong foundation, with significant progress in all indicators. Now, we are taking it a step further and raising our sights to continue reducing consumption and emissions across our entire real estate network. Beyond the targets, this plan consolidates a culture of environmental efficiency and responsibility throughout the entire organization, where every building and every team contributes to a common aim,” he added.

The eco-efficiency plan centers on five main pillars.

Renewable Energy Expansion

BBVA plans to increase renewable electricity use through power purchase agreements, renewable energy certificates, and on-site renewable generation systems.

The bank already uses renewable energy contracts in Spain, Mexico, Türkiye, and Argentina. It also operates solar installations in several countries, including Spain, Mexico, Peru, Uruguay, Türkiye, and Argentina.

Energy Efficiency Improvements

The bank will continue upgrading office infrastructure to lower energy use. Planned improvements include modern lighting systems, smarter climate control technologies, and better building management systems.

These upgrades aim to reduce operational costs while lowering emissions.

Sustainable Mobility

BBVA is also working to reduce transportation-related emissions. The company plans to gradually replace its vehicle fleet with electric or low-emission vehicles.

In addition, it encourages employees to adopt greener commuting options. The bank already offers electric vehicle charging stations, shared transport services, and corporate shuttle systems in some regions.

Better Waste and Resource Management

The bank wants to reduce water use, cut paper consumption, and improve recycling and waste recovery systems across its operations.

These measures support BBVA’s broader goal of lowering the environmental footprint of its offices and facilities.

Operational Decarbonization

The final pillar focuses on reducing both direct and indirect emissions linked to the bank’s activities.

BBVA uses internal financial incentives to push business units toward lower emissions. In 2025, the bank retired 167,532 carbon credits and maintained an internal carbon price of €32 per ton.

This system charges departments according to their carbon footprint. For example, emissions from business travel are reflected in local budgets. The idea is to encourage teams and employees to consider the environmental cost of their decisions.

Source: BBVA

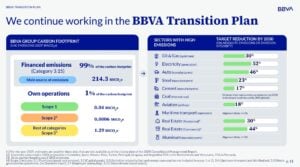

Scope 3 Emissions Remain the Biggest Challenge

Like many global banks, most of BBVA’s emissions do not come from office buildings or company vehicles. Instead, they come from financed emissions linked to loans and investments.

These indirect emissions, known as Scope 3 emissions, account for about 99% of the bank’s total carbon footprint.

To address this issue, BBVA has developed sector-specific transition plans and monitoring systems. The bank has also set intermediate emissions reduction targets for 2030 to align its financing portfolio with global decarbonization pathways.

This effort is especially important because banks play a major role in financing industries such as energy, transport, manufacturing, and infrastructure. Their lending decisions can strongly influence the pace of the global energy transition.

Sustainable Business Activity Continues to Grow

Alongside reducing its own emissions, BBVA is increasing financing for sustainable projects and businesses.

In the first quarter of 2026, the bank channeled €36 billion into sustainable business activities. This marked a 33% increase compared to the same period a year earlier.

Of this amount, €27 billion supported environmental initiatives linked to climate action and natural capital. The remaining €9 billion is focused on social projects and challenges.

Spain represented the largest share of sustainable business activity during the quarter at 35%. Türkiye followed with 17%, while Mexico contributed 16%. South America accounted for 9%, and other regions made up the remaining 23%.

Most of the financing came through traditional lending and transactional banking services, which represented 86% of the total. Capital markets activities accounted for 10%, while project finance contributed 4%.

The bank has now reached €170 billion toward its larger €700 billion sustainable business target for the 2025-2029 period.

The details are displayed in the image below:

BBVA Links Growth With Sustainability

BBVA’s latest strategy shows how major financial institutions are increasingly combining business growth with environmental goals.

The bank has already achieved sharp reductions in operational emissions and resource consumption. Now it is shifting attention toward harder challenges, such as financed emissions and sector-wide decarbonization.

Its growing sustainable finance business also highlights rising demand for funding tied to renewable energy, efficient resource use, and climate solutions.

Source: BBVA

As regulators, investors, and customers push companies toward lower emissions, banks like BBVA are expected to play a larger role in financing the global transition to a low-carbon economy.